Novo Nordisk: From Market Darling to Selloff Target — Should You Buy the Dip?

TradingKey - We've recently observed that,Novo Nordisk A/S, impacted by intensifying competition in weight-loss drugs (such as from U.S.Eli Lilly and Company) and weaker-than-expected earnings reports, has seen its stock price continually decline, falling over 70% from its peak of 143.54. Furthermore, Novo Nordisk recently announced the analysis results of its Phase III clinical trial for oral semaglutide in early symptomatic Alzheimer's disease. As it failed to meet its objectives, the stock plummeted over 5% in a single day.

Despite the various challenges currently confronting Novo Nordisk, we maintain thatits valuation is severely understated at this juncture, presenting a short-term opportunity for valuation correction.However, from a long-term perspective, given that its competitive moat has been breached by Eli Lilly, investors should continue to monitor whether the company's core competitiveness can be strengthened or enhanced. This will be pivotal in effectively mitigating investor apprehension.

What is Novo Nordisk?

Novo Nordisk (NVO), a global leading biopharmaceutical company headquartered in Copenhagen, Denmark, was founded in 1923. With over a century of focus on diabetes care and treatment, it is also involved in drug discovery, R&D, manufacturing, and marketing.

Novo Nordisk's primary identity is its long-standing dominance in the global insulin market, coupled with its absolute leadership in the highly popular GLP-1 class of drugs, which serve as dual powerhouses for weight loss and diabetes treatment. The company's most renowned product, semaglutide, has led to Ozempic for Type 2 diabetes and Wegovy for obesity. Combined sales for these two products exceeded $30 billion in 2024.

Novo Nordisk's key brands include NovoLog/NovoRapid, NovoLog Mix/NovoMix, Prandin/NovoNorm, NovoSeven, Norditropin, and Vagifem, among others. The company's pharmaceuticals are sold in over 180 countries. Its global commercial structure is comprised of two major regions: North America and International Operations, delivering therapies to patients through clinical research, manufacturing networks, and market channels.

Why Has Novo Nordisk's Stock Price Continuously Declined?

[NVO Historical Stock Price Trend, Source: TradingView]

Prior to 2024, examining the historical trajectory ofNovo Nordisk (NVO)stock reveals a near-uninterrupted upward trend. However, beginning in 2024, its share price experienced a sharp and historic reversal. We attribute this to the following factors:

I. Breakdown of a Dominant Industry Moat

Since 2024, Novo Nordisk has faced persistent market share pressure from competitors, with its core competitiveness gradually being matched and even surpassed.

Eli Lilly has achieved explosive sales growth with Mounjaro/Zepbound in the diabetes and weight management sectors. Crucially, clinical trials consistently demonstrate superior average weight loss compared to semaglutide (manufactured by NVO).

Investors now clearly recognize that Novo Nordisk's prior advantages—its monopolistic dominance and unshakeable first-mover status—have been completely reversed. Instead, a multi-competitor landscape has emerged, characterized by "Eli Lilly's comprehensive catch-up and significant market share erosion." Concerns regarding Novo Nordisk's future growth trajectory and sustainability have led to a substantial compression of its valuation premium, which represents the core driver of sustained stock price pressure since 2025.

II. High Valuation Correction and Commercialization Uncertainties

Between 2021 and 2024, Novo Nordisk achieved outperforming gains driven by its Ozempic/Wegovy pipeline, elevating its valuation into the high-growth stock range.

In December 2024,CagriSema's Phase III trial resultsshowed a 22.7% weight loss over 68 weeks, falling short of the market's consensus expectation of 25%. While seemingly small, this discrepancy delivered a significant blow to investors' elevated expectations for Novo Nordisk, causing the stock to plummet 17.83% that day and marking Novo Nordisk's largest single-day decline in history.

In March 2025, Novo Nordisk unveiled the results of its REDEFINE 2 clinical trial for its blockbuster weight-loss drug,CagriSema. The drug achieved an average weight reduction of 15.7% in obese patients. Although a significant achievement, this was still below the market's approximate 20% expectation. Following the announcement, the company's stock price briefly declined by 6.5%.

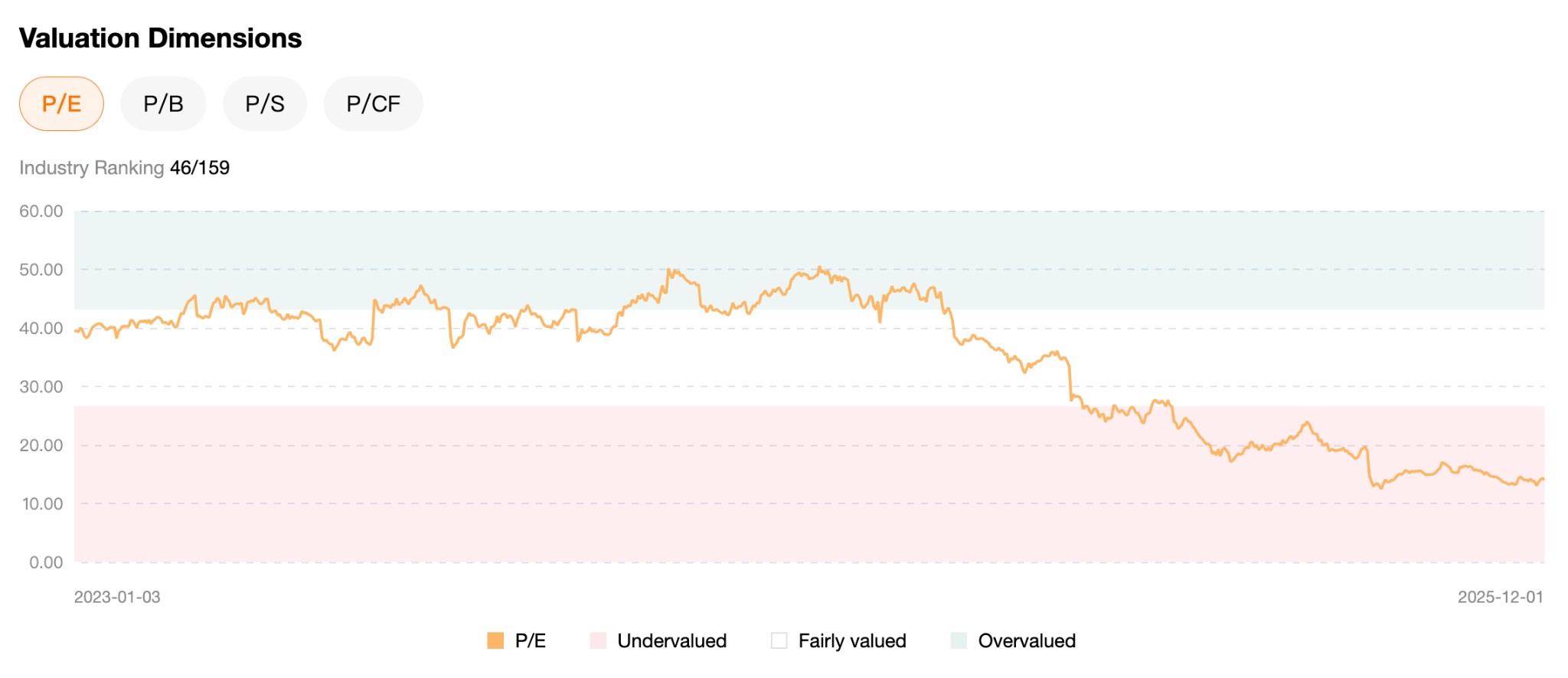

[Novo Nordisk Historical P/E Overview, Source: TradingKey]

From 2024 to 2025, as the market gradually returned to rationality from the perils of high valuations and some capital opted to realize gains, any negative or potentially negative news triggered an amplified pullback inNovo Nordisk's stock price.

III. Tightening Regulation and Medicare Negotiations Squeeze Profits

Since their market launch, Novo Nordisk's GLP-1 class drugs have been expensive and highly demanded. This supply-demand dynamic, coupled with periods of market shortage, has led to a proliferation of "unauthorized compounded/formulated" similar alternative products. This situation has drawn regulatory scrutiny and increased public relations and legal risks for the company. Consequently, the long-term price and supply predictability of Novo Nordisk's GLP-1 drugs face significant uncertainties.

Furthermore, in early 2025, the U.S. Department of Health and Human Services (HHS) announced its intention to include Novo Nordisk's high-priced prescription drugs, including Wegovy and Ozempic, in its Medicare price negotiation program. This development implies that these costly medications will be subject to mandatory price reductions.

This clearly constitutes a significant impact on the company's gross profit margins, particularly for pharmaceutical companies like Novo Nordisk with a single, dominant "moat." After the market swiftly absorbed this negative news, Novo Nordisk's stock price fell steadily. Morgan Stanley analysts commented that the progress of U.S. government drug price negotiations was unsurprising, and the inclusion of Novo Nordisk's Wegovy and Ozempic on the Medicare price reduction negotiation list was largely anticipated.

This was later corroborated in November 2025, when Novo Nordisk reached an agreement with the U.S. government that would substantially reduce the future selling prices of its GLP-1 drugs. While these price cuts might expand drug accessibility, they simultaneously pose a significant threat to pharmaceutical gross margins. This essentially trades profit for market share, a strategy we believe lacks strong sustainability.

What is the Market Sentiment on Novo Nordisk Stock?

Analyzing Novo Nordisk's stock trajectory, we believe the share price hasreached a nadir.

From a news flow perspective, although Novo Nordisk has recently faced multiple pressures from policy, competition, and R&D expectation shortfalls, from an allocation and valuation recovery standpoint, the company is currently nearing a "priced-in" or "all bad news out" state. Market scrutiny of Medicare negotiations, price pressures, short-term supply constraints, and next-generation product lines like CagriSema is largely complete, with the stock price already reflecting most discernible risks. In other words, the probability of new negative news causing systemic shocks to the share price is significantly decreasing.

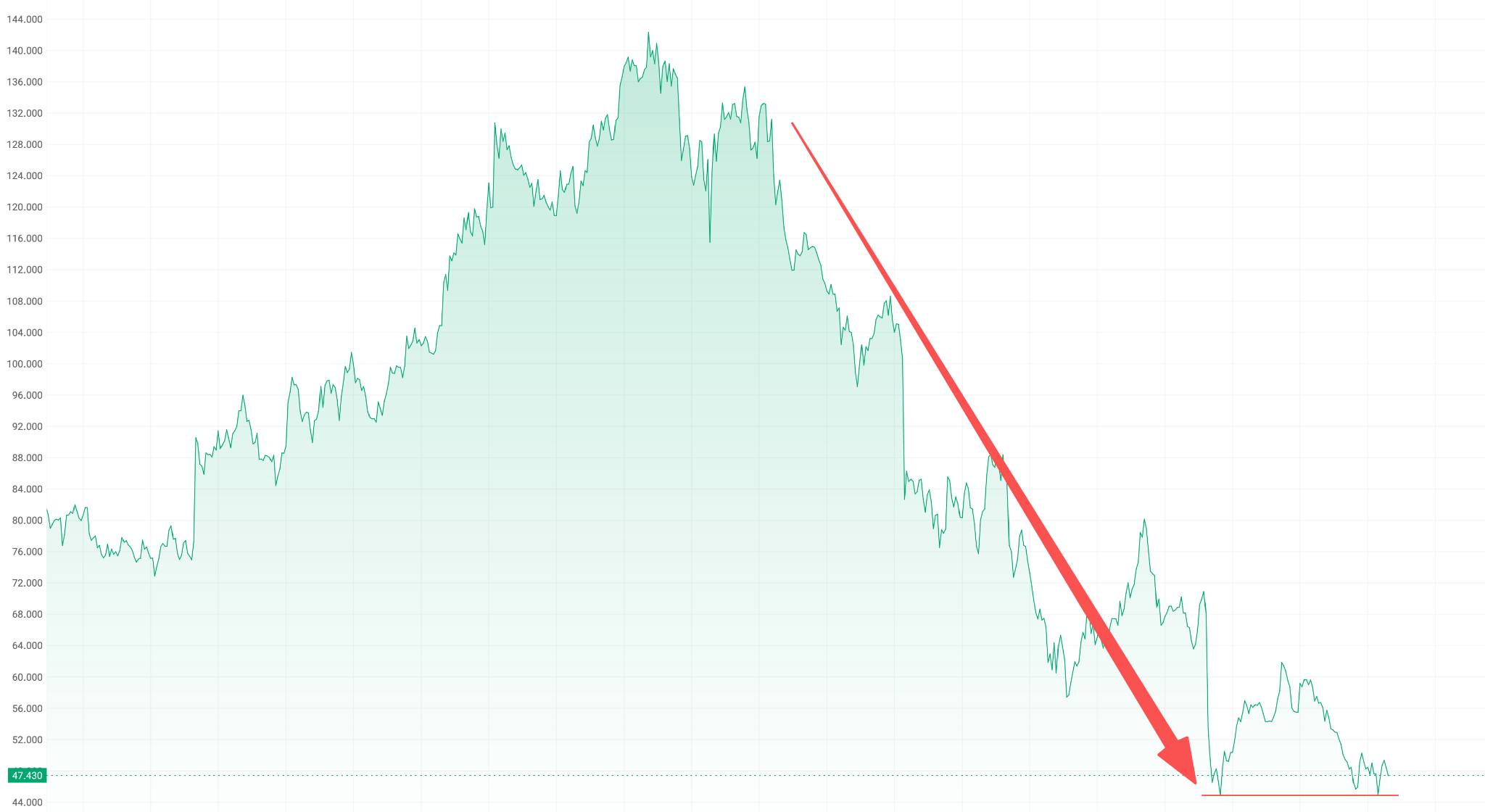

[NVO Stock PriceDaily Candlestick Chart, Source: TradingView]

Technically, after repeatedly touching new lows, the stock price has attempted to rebound and stabilize. We therefore largely conclude that the share price has found a floor to some extent. Even with the impact of downgraded guidance and weaker-than-expected earnings from Novo Nordisk, its stock has maintained relative stability.

Should You Buy Novo Nordisk Stock Now?

To reiterate, despite the various challenges currently confronting Novo Nordisk, we maintain thatits valuation is severely understated at this juncture, presenting a short-term opportunity for valuation correction.However, from a long-term perspective, given that its competitive moat has been breached by Eli Lilly, investors should continue to monitor whether the company's core competitiveness can be strengthened or enhanced. This will be pivotal in effectively mitigating investor apprehension.

Novo Nordisk Company Announcements and Press Release Quick Look

Recommended Articles