U.S. 10-Year Treasury Yields Stay High — Here Are Wall Street’s Investment Calls

TradingKey - Earlier this month, the U.S. 10-year Treasury yield shot up more than 70 basis points in just a few days, climbing toward 4.6%. Not long ago, it had briefly fallen below 4%. Notably, easing global trade tensions—fueled by optimism around U.S. tariff negotiations—helped spark a rebound in the bond market last week, with long-term Treasury yields falling more sharply. The 10-year yield briefly dropped more than 10 basis points, slipping below 4.3%.

However, Donald Trump’s repeated criticism of Federal Reserve Chair Jerome Powell this week renewed investor concerns and drove the 10-year Treasury yield back up to recent highs.

Investors Growing Uneasy About Fed Independence

Tensions between Donald Trump and Federal Reserve Chair Jerome Powell are once again raising questions about the future of Fed independence—and spooking bond investors in the process. Their back-and-forth has cast a long shadow over a U.S. Treasury market now worth $29 trillion.

Concerns over central bank independence are growing. In recent weeks, the President has stepped up his calls for interest rate cuts, even saying that Powell’s term “can’t end fast enough” — remarks that have fueled a sell-off in Treasuries. As a result, the yield on the 10-year Treasury climbed above 4.4% this week, approaching levels seen during market turbulence earlier this month.

What investors are worried about is that Trump might try to reshape U.S. monetary policy in order to ease inflation and achieve his goal of lowering interest rates. If the market senses such a policy shift, long-term bonds would be particularly vulnerable.

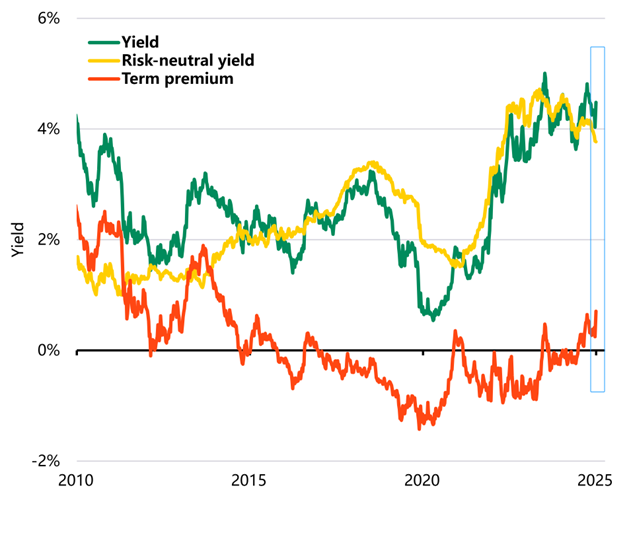

U.S. Treasuries Are Losing Their “Safe Haven” Status?

Although inflation expectations have been partly blamed for the recent yield spike—given that tariffs tend to push up prices and complicate the case for interest rate cuts—traders are now increasingly betting that the Fed will cut rates this year due to rising recession risks. That suggests interest rate policy is not the primary driver of higher yields.

Instead, technical factors may be accelerating the bond market’s volatility. Hedge funds caught on the wrong side of moves may have been forced to liquidate positions, while dealers have pulled back from volatility-smoothing practices. However, market anomalies extend beyond technicals.

"The behavior of Treasuries and the U.S. dollar has been unusual in recent weeks," noted analysts at Evercore ISI. “When the issue is a broader loss of confidence in the United States, even a much fuller retreat on trade might not work to bring yields down... We’re not sure any of the tools remaining in Trump’s toolkit will be sufficient to fully staunch the bleeding.”

.jpg)

Source:Nomura

In fact, since Trump took office, the U.S. credit default swap (CDS) spread—a barometer of perceived sovereign credit risk—has risen by 10 basis points, signaling increasing caution among global investors.

Trade Deficit Moves Stoke U.S. Bond Risk Premiums

The unusual divergence—forward-looking bond yields rising while the dollar trends lower—reflects investors’ growing demand for risk compensation. With soaring fiscal deficits and an uncertain outlook for trade policy, concerns over the sustainability of U.S. government borrowing are mounting.

Federal Reserve data shows the U.S. faces large deficits and heavy debt. A rapid push to cut the trade deficit could make debt financing harder—especially if tariff uncertainty shakes foreign investor confidence. That would mean higher yields and borrowing costs.

Global supply chains can realign over time, but abrupt reconstruction can create severe dislocations: tariff-driven inflation, disrupted access to key inputs, and potential production halts may slow growth materially or even trigger stagflation—handcuffing the Fed in the process.

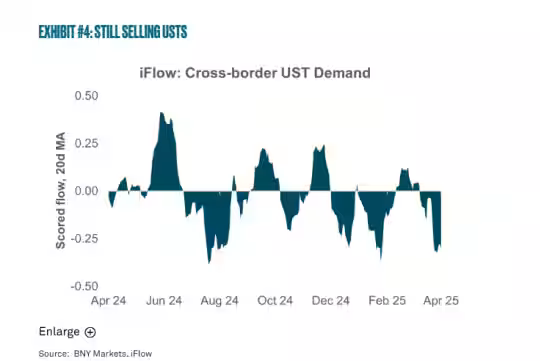

Japanese Selling Adds Pressure to U.S. Treasury Market

As of June 2024, foreign investors—particularly sovereign institutions—held approximately $7 trillion in the U.S. Treasuries, representing around one-third of total publicly held debt. Continued foreign participation is critical for rolling over existing bonds and absorbing new issuance.

However, recent data confirms a sharp foreign drawdown. According to John Velis, Americas Macro Strategist at BNY Mellon, “The perceived safe-haven status of Treasuries is facing increasing skepticism.” In a recent client note, Velis highlighted the largest weekly net outflow of foreign capital from Treasuries in years—with eight out of eleven sessions showing net foreign selling through April 11.

Source: BNY Mellon

Japanese data corroborates this. The Ministry of Finance said private institutions in Japan—including pension funds and banks—sold 17.5 billion long−duration U.S.debt in the week ended April 4, followed by another 3.6 billion the following week, marking the largest two-week offload since 2005.

Softening Demand for U.S. Treasuries

Investor appetite for U.S. debt showed further signs of strain at recent government auctions. On Tuesday, a $60 billion auction of 2-year Treasury notes cleared at a high yield of 3.795%—above the pre-auction yield, with a tail of 0.6 basis points, the widest since October. The tail indicates that investors demanded more yield to absorb the supply.

A $44 billion sale of 7-year notes on Thursday also tailed—at 4.121%, 0.2 basis points above the pre-auction level—reflecting a second consecutive undersubscribed auction. The indirect bidder participation rate (used as a proxy for foreign interest) fell to 59.3%, down from 61.2% in March, and its lowest level since December 2021.

These auction results raise fresh questions about how sustainable public debt issuance will be, and whether the Fed may ultimately have no choice but to restart quantitative easing and step in as a buyer of last resort.

Here Are Wall Street’s Top Treasury Picks

Despite short-term uncertainty, leading asset managers see opportunities in the current market. On April 23, Mohit Mittal, CIO of Core Strategies at PIMCO, argued that investors are overly focused on foreign positioning and underestimating the possibility of long-term weakness in the U.S. economy. In his view, current Treasury yields offer attractive value—especially in the 5- to 10-year segment.

Moreover, given the elevated volatility from uncertain Fed policy and tariffs, analysts expect a rotation away from riskier segments such as high-yield corporate bonds or private credit, toward safer short-term U.S. government bond funds.

“Every time new news emerges that raises the likelihood of large U.S. or foreign tariffs, recession risks increase—prompting renewed flows into the relative safety of short-duration Treasuries,” said Brian Huckstep, CIO at Advyzon Investment Management.

BlackRock offered a similar take: while the firm continues to push back on market expectations of multiple Fed cuts this year, it tactically favors short-term U.S. Treasuries as cash-like instruments. The firm also prefers mid-duration bonds, which are less affected by a higher term premium from investors.

For investors looking to access the U.S. bond market quickly and efficiently, Treasury ETFs offer a convenient solution. The ETFs listed below track the performance of U.S. Treasury bonds.

- TLT (iShares 20+ Year Treasury Bond ETF): Invests in long-term U.S. Treasury bonds with maturities greater than 20 years.

- IEF (iShares 7–10 Year Treasury Bond ETF): Focuses on medium-term U.S. Treasury bonds with maturities between 7 and 10 years.

- SHY (iShares 1–3 Year Treasury Bond ETF): Covers short-term U.S. Treasury bonds with maturities of 1 to 3 years.

- BIL (SPDR Bloomberg 1–3 Month T-Bill ETF): Invests in ultra-short-term U.S. Treasury bills with maturities of 1 to 3 months.

- VGSH (Vanguard Short-Term Treasury ETF): Targets U.S. Treasury securities with shorter remaining durations.

- GOVT (iShares U.S. Treasury Bond ETF): Provides broad exposure across multiple maturity segments of the U.S. Treasury market.

Recommended Articles