Arthur Hayes Warns Tether ‘Macro Hedge’ Risks Equity Wipeout in 30% Bitcoin Correction

BitMEX co-founder Arthur Hayes has warned that Tether risks balance-sheet insolvency if its Bitcoin and gold reserves suffer a 30% drawdown.

His November 30 post targets the structural vulnerabilities in Tether’s latest asset allocation. He suggests the firm has tied its solvency to the performance of volatile risk assets rather than relying solely on the stability of government debt.

Hayes Critique Tether’s Gold and Stablecoin Holdings

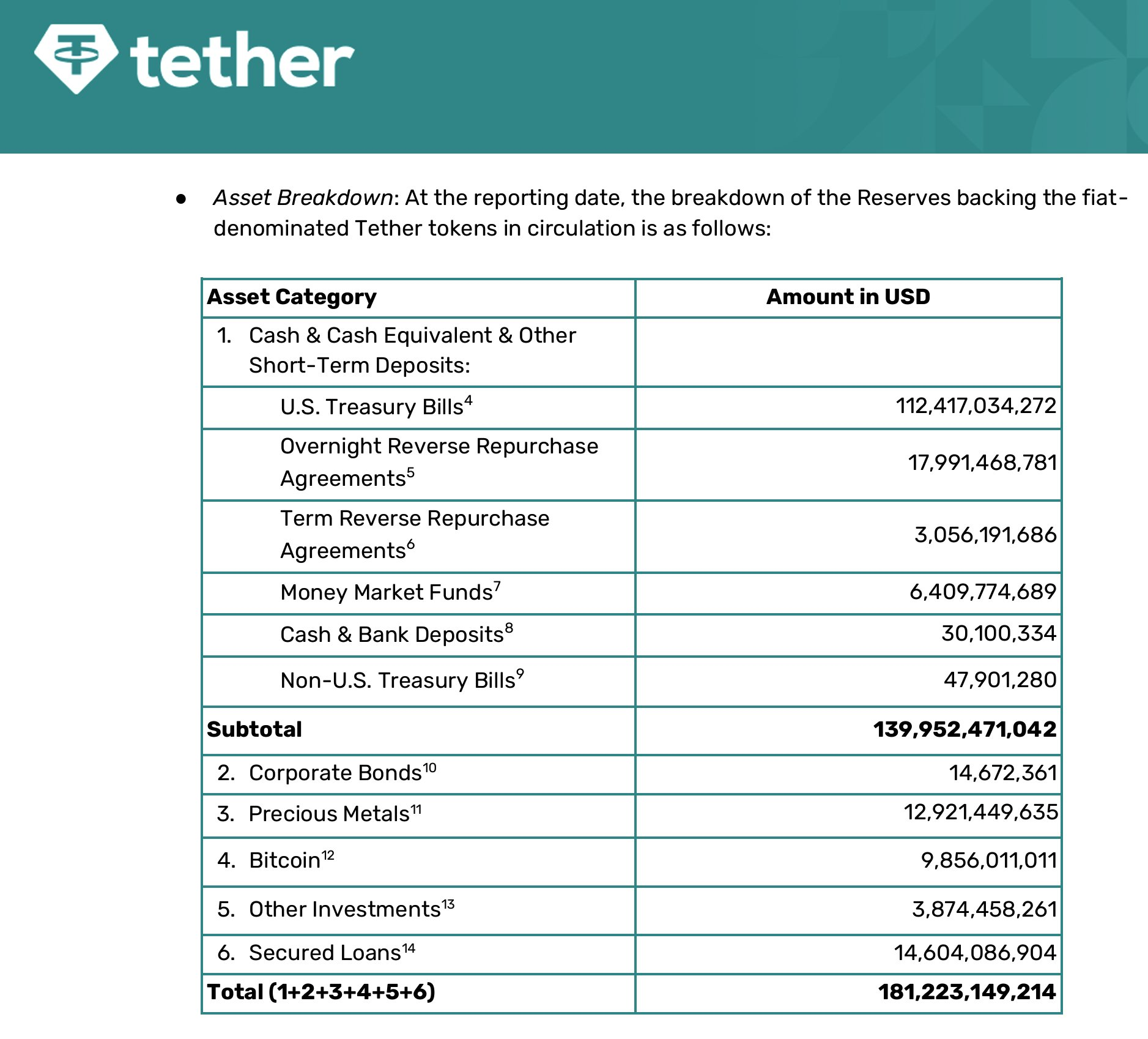

Hayes’ assessment draws on Tether’s third-quarter 2025 attestation, which reveals a significant rotation into non-fiat collateral. The report shows the issuer now holds $12.9 billion in precious metals and $9.9 billion in Bitcoin.

According to Hayes, this allocation represents a deliberate “interest rate trade.” His thesis posits that Tether is preparing for Federal Reserve rate cuts that would compress the yield on its massive portfolio of US Treasury bills.

“[Tether] thinks the Fed will cut rates, which crushes their interest income. In response, they are buying gold and BTC that should in theory moon as the price of money falls,” Hayes noted.

However, Hayes argues this strategy introduces asymmetric risk to the company’s thin layer of equity.

Hayes contends that this figure exceeds Tether’s surplus capital, rendering the firm theoretically insolvent even if it remains operationally liquid.

He warned that such a scenario would likely force large holders and exchanges to demand a real-time view of the balance sheet to assess the safety of the peg. Notably, this warning aligns with S&P Global’s decision to assign USDT a ‘5’ rating, the lowest on its scale.

Industry Stakeholders Defend Tether

Industry proponents maintain that the insolvency thesis conflates balance sheet accounting with actual liquidity risk.

Tran Hung, CEO of UQUID Card, dismissed the warning as fundamentally flawed.

He noted that the vast majority of Tether’s $181.2 billion balance sheet remains parked in highly liquid, low-risk instruments. Indeed, the attestation confirms Tether holds $112.4 billion in US Treasury Bills and nearly $21 billion in repo agreements.

Tether USDT Stablecoin Reserves. Source: Tether

Tether USDT Stablecoin Reserves. Source: Tether

Hung argues these “Cash and Cash Equivalents” provide a liquidity wall sufficient to cover the overwhelming majority of USDT in circulation.

Considering this, he argued that Tether would remain fully redeemable even if a market downturn eliminated its corporate equity buffer.

“Tether has consistently demonstrated strong redemption capacity, including $25 billion redeemed in just 20 days during the 2022 market crisis (FTX crisis), one of the largest liquidity ‘stress tests’ in financial history,” Hung noted.

Meanwhile, Cory Klippsten, CEO of Swan Bitcoin, pointed out that Tether’s leverage is more aggressive than that of traditional financial institutions.

Tether is running about 26x leverage with a 3.7% equity cushion. About three quarters of assets are short-term sovereign and repo; one quarter is a mix of BTC, gold, loans, and opaque investments,” Klippsten said.

According to him, a 4% portfolio loss would erase the common equity, while A 16% drop in the riskiest assets would have the same effect.

However, despite the structural leverage, he suggests the risk is mitigated by Tether’s sheer profitability. Indeed, the stablecoin issuer is on track to record a profit of more than $15 billion this year.

Moreover, Klippsten also noted that Tether’s owners recently withdrew a $12 billion dividend. Considering this, he argued they have the capacity to recapitalize the firm immediately if its buffer were ever breached.

Recommended Articles