Fed Cuts Rates by 50 Basis Points: Can We Expect Greenspan-like Results?

- Silver Price Forecast: Trump Signals Rapid Progress in US-Iran Negotiations, Bulls Target $90

- Gold declines below $4,500 as Iran tensions stoke inflation fears and bolster Fed hike bets

- Fed’s Powell says credibility lost if President can fire officials

- $1.5 Billion in Crypto Assets Liquidated, Bitcoin Falls Below $66,000 Mark. What Is the Reason?

- Bitcoin Suffers Year’s Strongest Waterfall-Style Decline. Will It Next Drop to the $60,000 Mark?

- WTI rises to near $93.00 as Iran launches missiles toward Kuwait, Bahrain

Insights - The Federal Reserve has kicked off a new easing cycle with a 50 basis point rate cut, yet the market rally did not last long. Concerns loom over whether the Fed can replicate the economic soft landing achieved by Alan Greenspan in 1995.

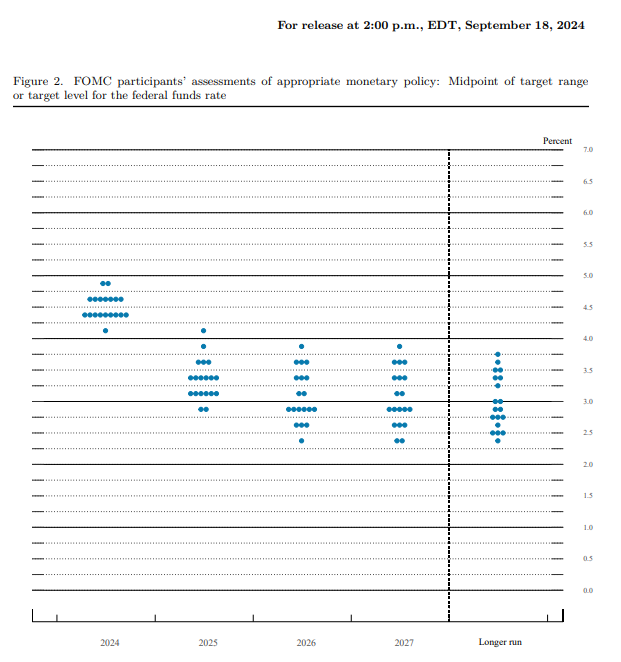

On September 18, U.S. Eastern Time, the Fed cut the federal funds rate from a range of 5.25%–5.50% to 4.75%–5.00%. The dot plot indicates that at least another 50 basis points will be cut this year, with an additional 100 basis points expected in 2025.

Source: Federal Reserve; Dot Plot

Powell's hawkish stance indicates that the Fed is not rushing to cut rates and warns against seeing large cuts as the new norm.

His comments dampened aggressive rate cut expectations and heightened concerns about future policy uncertainty. Various assets, including U.S. stocks, gold, and the dollar index, experienced significant reversals.

Among the six easing cycles since 1989, the Fed successfully avoided immediate economic downturns only twice—in 1995 and 1998. The current situation is most similar to the 1995 rate cut cycle, during which Greenspan led the Fed to achieve a rare economic soft landing.

How Does the Current Rate Cut Differ from Greenspan's Cuts?

In 1995, the U.S. experienced a slowdown in industrial production and job growth, with a rise in initial jobless claims. Although Greenspan did not believe these figures indicated an impending recession, he initiated rate cuts On July 6, 1995, lowering the interest rate from 6% to 5.25% over six months, a total reduction of 75 basis points. This move helped revitalize the manufacturing and job markets, allowing the U.S. economy to achieve a soft landing.

The context for the current rate cut is somewhat similar to that of 1995: unemployment rates are slightly rising, inflation is declining, and the U.S. economy is showing short-term weakness. However, the key difference is that the 1990s were marked by economic prosperity, whereas today, the global economy faces rising downward pressures, low potential growth rates in the U.S., and historically high debt levels.

Additionally, there are geopolitical changes and uncertainties surrounding the upcoming U.S. presidential election. Market confidence in the future is far less robust than it was in 1995.

Therefore, whether the Federal Reserve can replicate Greenspan's success from 1995 remains to be seen.

How Will Assets Respond After the 50 Basis Point Cut?

Unlike Greenspan's initial 25 basis point cut, the Fed has opened its easing cycle with a 50 basis point reduction.

According to Nomura, market reactions to a 50 basis point cut have been mixed historically. The S&P 500 faced significant losses in 2007, 2001, and 1974. However, in most cases, the S&P 500 showed little change three months after a 50 basis point cut.

In contrast, small-cap stocks averaged a 5.6% increase, technology stocks performed well, and value stocks outperformed growth stocks. Meanwhile, The dollar rose, metal prices surged, and the yield curve steepened.

Regardless of the magnitude of the cut, data from the six Fed easing cycles since 1989 shows that, on average, the S&P 500 rises by 13% in the six months following a rate cut (excluding the recession periods of 2001 and 2007).

In four of the past six easing cycles, gold delivered positive returns for investors, while the dollar and oil prices experienced fluctuations.

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.