- Gold Price Forecast: Gold Poised to Break $4,200 as Oil Price Slump Eases Inflation Fears

- Gold declines despite easing concerns over inflation, interest rate hikes

- Fed Decision Eve: 104 Economists Expect No Change; Why Is Citadel Securities Betting on a Surprise Hike?

- Gold Price Forecast: Can Gold Hold $4,020 as Fed Rate Hike Expectations Rise?

- Middle East War updates: US-Iran pause strikes as Trump weighs up diplomatic options

- WTI Oil flirts with the $80 level amid speculation about US-Iran peace talks

Market Review

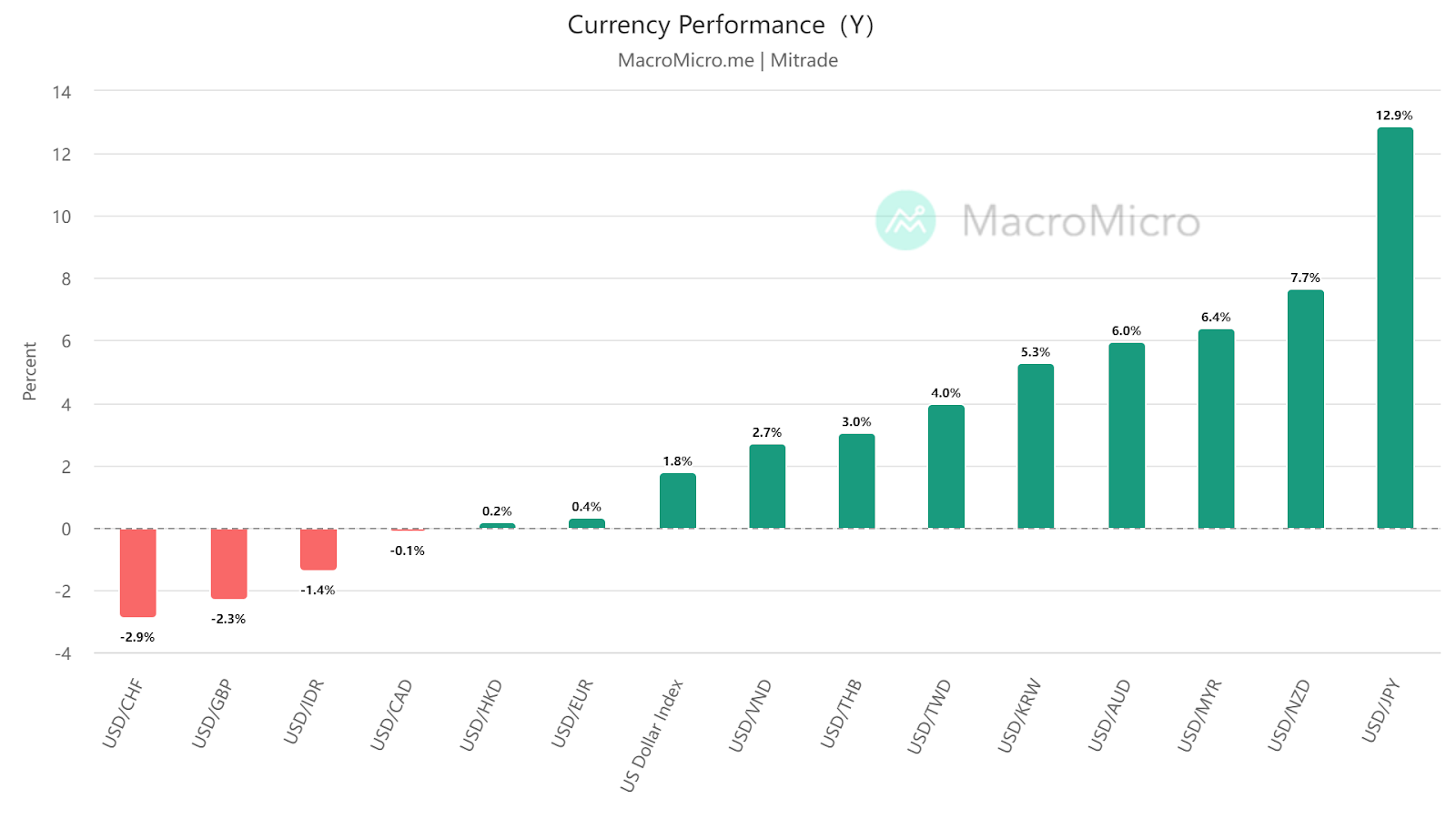

Last week (9/11-9/15), the US Dollar Index rose by 0.22%. Non-US currencies showed mixed performance, with the Japanese Yen slightly declining by 0.01%, the Euro falling by 0.40%, and the Australian Dollar rising by 0.9%.

【Source: MacroMicro;Date2023/9/11-2023/9/15】

【Source: MacroMicro;Date2023/1/1-2023/9/15】

1.ECB Dovish Hike: How will the Euro/Dollar trend in the future?

Last week, the euro declined by 0.4% against the US dollar, primarily due to dovish interest rate actions by the European Central Bank (ECB) and strong US economic data.

On September 14th, the ECB announced its latest interest rate decision, raising rates by another 25 basis points. However, in the monetary statement, the ECB indicated that key rates had reached a level that could be sustained for a considerable period of time, implying that this round of rate hikes may be ending.

Furthermore, the ECB revised down its economic forecasts for the next three years: it now expects GDP growth of 0.7% in 2023, previously projected at 0.9%; 1% in 2024, previously projected at 1.5%; and 1.5% in 2025, previously projected at 1.6%.

Additionally, inflation projections for this year and next were revised upward: the ECB now expects the European inflation rate to reach 3.2% in 2024, up from the previous forecast of 3.0% in June. It anticipates a 2.1% inflation rate in 2025, compared to the previous projection of 2.2% in June.

【Source:MacroMicro】

Concerns about the Eurozone economy entering stagflation have been rising, while at the same time, overall US economic data has been strong. Data indicates a significant increase in US retail sales of 0.6% in August, surpassing the expected 0.1%. Additionally, the Producer Price Index (PPI) for August showed a year-on-year growth of 1.6%, higher than the expected 1.3%.

The relative performance of the European and US economies has put further pressure on the euro against the US dollar, leading to a sharp decline of 0.8% in the EUR/USD exchange rate on September 14th.

Mitrade Analyst:

Against the backdrop of a deteriorating European economy, the relative strength of economic fundamentals has become the dominant factor in pricing the euro/dollar exchange rate. In the medium term, the gap between the recession in the Eurozone and strong US economic growth continues to widen, indicating further downward pressure on the euro/dollar. This week, the focus will be on the Federal Reserve interest rate meeting, and if the market interprets it dovishly, there may be a technical rebound for the euro/dollar in the short term.

From a technical perspective, the euro/dollar has broken below previous lows and remains in a downtrend. However, the RSI indicator is approaching oversold territory, suggesting that the euro may experience some rebound this week. Resistance is seen at 1.077, while support is seen at 1.060.

【Source:TradingView】

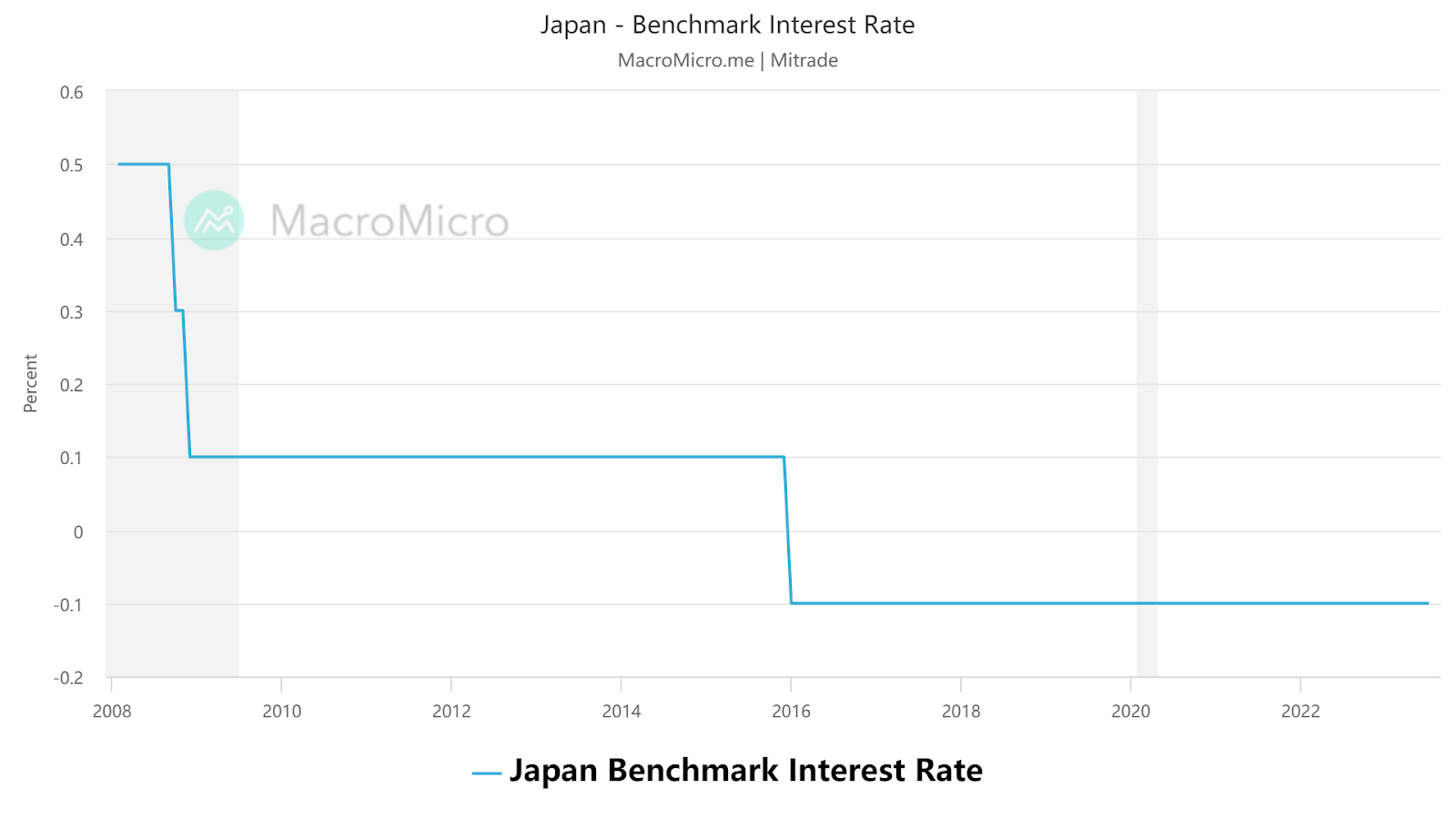

2.USD/JPY Remains Volatile, Focus on Meetings of the US and Japanese Central Banks

Last week, the USD/JPY initially declined and then rebounded, experiencing some downward pressure earlier due to hawkish comments from the Bank of Japan Governor Ueda Kazuo. However, it later returned to an upward trend.

According to sources familiar with the matter, Bank of Japan officials believe that Kazuo's remarks were not a policy signal but rather a reiteration of the need for policymakers to weigh upside and downside risks when deciding on policy adjustments. Nonetheless, the officials still acknowledge strong inflationary momentum, indicating a potential upward revision in the quarterly inflation outlook for October.

Kentaro Koyama, Chief Economist at Deutsche Securities, revised his forecast in the latest report, suggesting that the Bank of Japan may terminate Yield Curve Control (YCC) in October and could possibly end its negative interest rate policy in January next year.

【Source:MacroMicro】

The Bank of Japan will announce the outcome of the September monetary policy meeting this Friday. According to Bloomberg economists' predictions, the Bank of Japan is unlikely to change its interest rate policy.

Compared to last year, the urgency for Japanese government intervention in the yen exchange rate has decreased this year. Taking into account export trade, overseas revenue, and investment income, the Japanese economy and corporations can benefit from a weaker yen. Overall, maintaining a weak yen may have more advantages than disadvantages.

Therefore, it is likely that the Japanese Ministry of Finance and the central bank will continue to prefer verbal intervention to avoid the risks associated with rapid depreciation of the yen to the Japanese economy and capital flows.

Mitrade Analyst:

We believe the Bank of Japan will continue its accommodative stance in September, but there is a possibility of a hawkish tone from Governor Kazuo. Investors should take note of this and also pay attention to the Federal Reserve's interest rate meeting. If the USD/JPY quickly breaks through the key level of 148, Japanese authorities may resort to verbal intervention again.

From a technical perspective, the USD/JPY remains above the 21-day moving average, indicating strong bullish signals. However, the MACD indicator shows a balance between bullish and bearish forces with some signs of reversal. We expect the USD/JPY to rally and then pull back this week, continuing its volatile trend, with resistance at 148.5 and support at 146.5.

【Source:TradingView】

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.