3 Reasons It Might Be Time to Give Up on Lucid Stock

Key Points

A number of executives and VP-level talent have departed Lucid over the past two years.

Lucid's first quarter was a prime example of how severe its cash burn can be.

Shareholder dilution remains a primary concern, as the company will need more capital.

- 10 stocks we like better than Lucid Group ›

Lucid Group (NASDAQ: LCID) is accustomed to speed bumps in its business, and they came in the form of production snags, delays, and disappointing financial results early in its limited history.

Then Lucid seemingly got things turned around enough to achieve eight consecutive quarters of record deliveries, culminating in a full-year record of 15,841 vehicles in 2025. Production issues faded, and launching the Gravity SUV was set to bring in new demand and build scale for the automaker.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

That said, it's been another bumpy start in 2026. Here are three reasons it might be time to give up on Lucid becoming a worthy investment.

1. Talent jumping ship

If you want to put some public relations spin on this, you can, but the optics are bad at the very least, and at worst, it sure appears a lot of talent is fleeing Lucid. Let's start with the most notable, Marc Winterhoff, former interim CEO, who was supposed to stay on board as Lucid's COO under the newly appointed CEO. Plans changed rather quickly, and Lucid opted to eliminate the COO position entirely.

That's just one example. There have been roughly a dozen high-profile executive and VP-level exits over the past two years. The sweeping executive and other organizational changes have halved the number of positions reporting directly to the CEO. These moves also go hand in hand with Lucid cutting 18% of its workforce, targeting about $158 million in annual savings.

Lucid's Gravity SUV EV. Image source: Lucid.

You can try and spin this as streamlining the organization, but the truth is Lucid is gearing up for another mass-market vehicle, and you would think it should be building its employee base to support that, rather than cutting them.

2. Rough financials

It's easy to see Lucid's struggles in its quarterly financial numbers. Lucid has always been criticized for its high cash burn, but the first quarter of 2026 was staggering, with a free cash flow loss of $1.44 billion -- more than double the cash burn rate a year ago. Lucid also posted a large GAAP net loss of $1 billion for the quarter, driven by lower margins and unused factory production capacity.

It's also important for investors to grasp Lucid's liquidity situation. Lucid ended the first quarter with about $3.2 billion in liquidity. Add in the company's $1.05 billion capital raise in April, as well as an expansion of its credit line; Lucid's liquidity sits at about $4.7 billion. Even using a conservative $1 billion quarterly cash burn, you can see how the company could be in financial trouble without more capital by this time next year.

That's a perfect segue into the next reason investors should think twice or perhaps give up on Lucid: shareholder dilution.

3. Worse than rivals

Lucid has received several capital injections over the years, but it has consistently raised capital by issuing massive amounts of new shares, which shrinks the value of existing stakes for long-term shareholders. In theory, investors can stomach some shareholder dilution because the fresh capital should enable the company to pursue growth more aggressively. And while that's true for Lucid in some respects, it's also true that its massive cash burn simply needs additional incoming capital support.

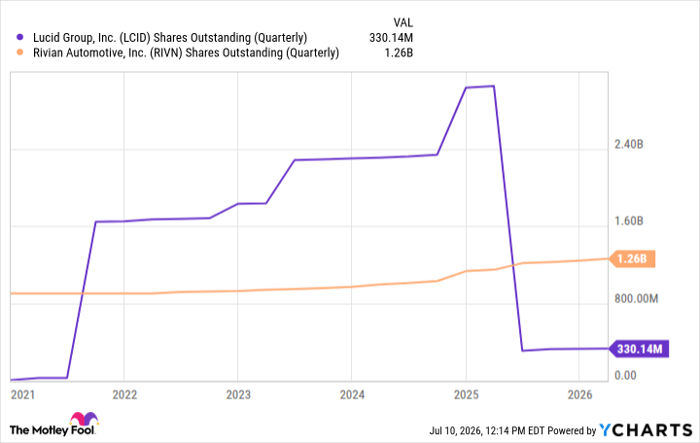

LCID Shares Outstanding (Quarterly) data by YCharts

As you can see in the chart above, Lucid has significantly increased its outstanding shares. That's especially true when compared to rival Rivian Automotive, which has been far more calculated in its fewer raises, and also boasts a Department of Energy loan for about $6.6 billion, as well as capital injections from its joint venture partner, Volkswagen.

You'll also notice the drastic decline in shares outstanding, which is because Lucid completed a 1-for-10 reverse stock split to artificially boost its trading price and avoid being delisted from the Nasdaq. It's not a matter of if, but when Lucid will need to raise more capital, and consistent shareholder dilution is something for all investors to consider.

What it all means

Lucid has always been an intriguing investment, as the company is widely lauded for its advanced electric vehicles (EVs) and compelling designs. That said, with the company's persistent supplier and production issues, recalls, and inability to improve unit economics, Lucid has driven into serious problems.

Given the sizable executive talent loss, its consistently high cash burn that requires fresh capital, and potential shareholder dilution, Lucid is not currently a viable long-term investment. If you've been holding shares, it might be time to consider other options.

Should you buy stock in Lucid Group right now?

Before you buy stock in Lucid Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lucid Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $396,542!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,299,961!*

Now, it’s worth noting Stock Advisor’s total average return is 931% — a market-crushing outperformance compared to 210% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 15, 2026.

Daniel Miller has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Recommended Articles