1 Mind-Boggling Metric That Proves Sandisk Stock Is Still Remarkably Cheap

Key Points

Wall Street expects Sandisk's revenue to double again in its next fiscal year.

The stock appears cheap relative to its peers.

- 10 stocks we like better than Sandisk ›

Sandisk (NASDAQ: SNDK) has been the top-performing S&P 500 stock so far this year. It's up by around 600%, easily outperforming the second-place performer, Dell, which is up by around 240%. So unless another stock emerges with a massive new tailwind or something catastrophic happens to Sandisk's business, I think it may have already locked up the title of 2026's best-performing stock. Moreover, I don't think it's done yet.

Despite a jaw-dropping run over the past year, the stock still looks pretty cheap. The question is, does it deserve to be?

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: The Motley Fool.

The memory chip market is cyclical

Sandisk makes NAND memory, which is non-volatile memory often used for storing information long term in solid-state drives (SSDs). AI data centers use a lot of SSDs, and the rapid infrastructure build-out has boosted Sandisk's business over the past year. However, demand for NAND memory is far greater than supply, which has caused prices to soar. This is also why storage for consumer devices has increased in price.

This combination has caused Sandisk's revenue and profits to skyrocket, and these conditions could continue for a while.

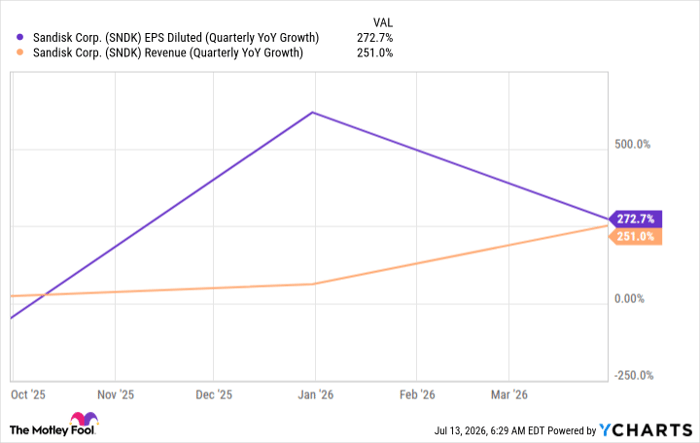

SNDK EPS Diluted (Quarterly YoY Growth) data by YCharts.

For the company's recently ended fiscal 2026 fourth quarter, Wall Street analysts expect it to report 337% revenue growth. For fiscal 2027, they expect 143% growth. Those are remarkable growth rates extended over a long time frame, and it would be understandable for investors to be excited about the future of the stock. But is it actually cheap?

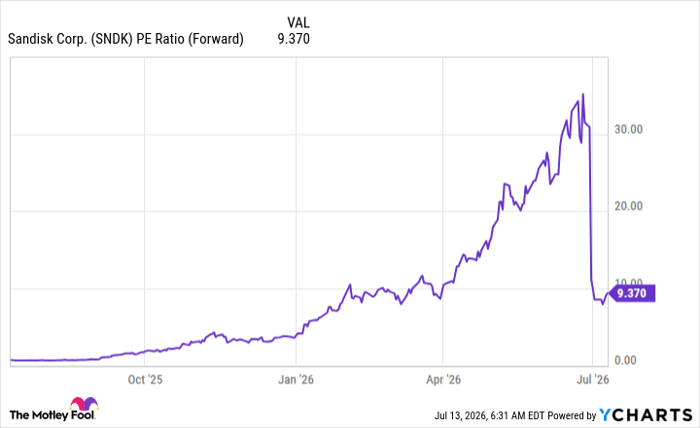

Today, Sandisk trades for a mere 9.4 times forward earnings.

SNDK PE Ratio (Forward) data by YCharts

Most stocks in the AI space trade for 20 to 30 times forward earnings, and some carry even greater premiums. If Sandisk rose to those levels, the stock would double or triple from here. However, there's a catch: The memory chip market is cyclical.

What will happen if demand decreases or if enough new production capacity comes online that supply and demand come back into balance? Or what if the shortage becomes a glut?

Today's astronomical memory chip prices would decline to normal levels. That would change the investment thesis behind Sandisk's business, and could cause the stock to plummet.

But when might something like that happen? After all, the AI build-out is expected to last for several years more, at a minimum. Most pundits and analysts point toward 2030 as the soonest it might end.

One memory chip maker, Micron (NASDAQ: MU), offered a projection a while back: It stated the memory chip market's growth could persist beyond 2027, which means that Samsung stock should have at least one more year of strong growth left, if not more.

I think that makes Sandisk stock a worthy investment, but shareholders will need to monitor memory chip market conditions to ensure that prices are staying elevated.

Should you buy stock in Sandisk right now?

Before you buy stock in Sandisk, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Sandisk wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $398,160!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,249,202!*

Now, it’s worth noting Stock Advisor’s total average return is 918% — a market-crushing outperformance compared to 209% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 14, 2026.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Micron Technology. The Motley Fool has a disclosure policy.

Recommended Articles