AST SpaceMobile Shares Plunge in Overnight Trading, What Happened? Will It Affect SpaceX?

TradingKey - In the early hours of April 19, AST SpaceMobile (ASTS.US) its seventh broadband communications satellite, BlueBird 7, launched from Cape Canaveral aboard Jeff Bezos' Blue Origin New Glenn rocket. Although the first stage was successfully recovered, the second stage delivered the satellite into an orbital altitude far lower than planned, rendering it unable to maintain operations and forcing it to deorbit and burn up.

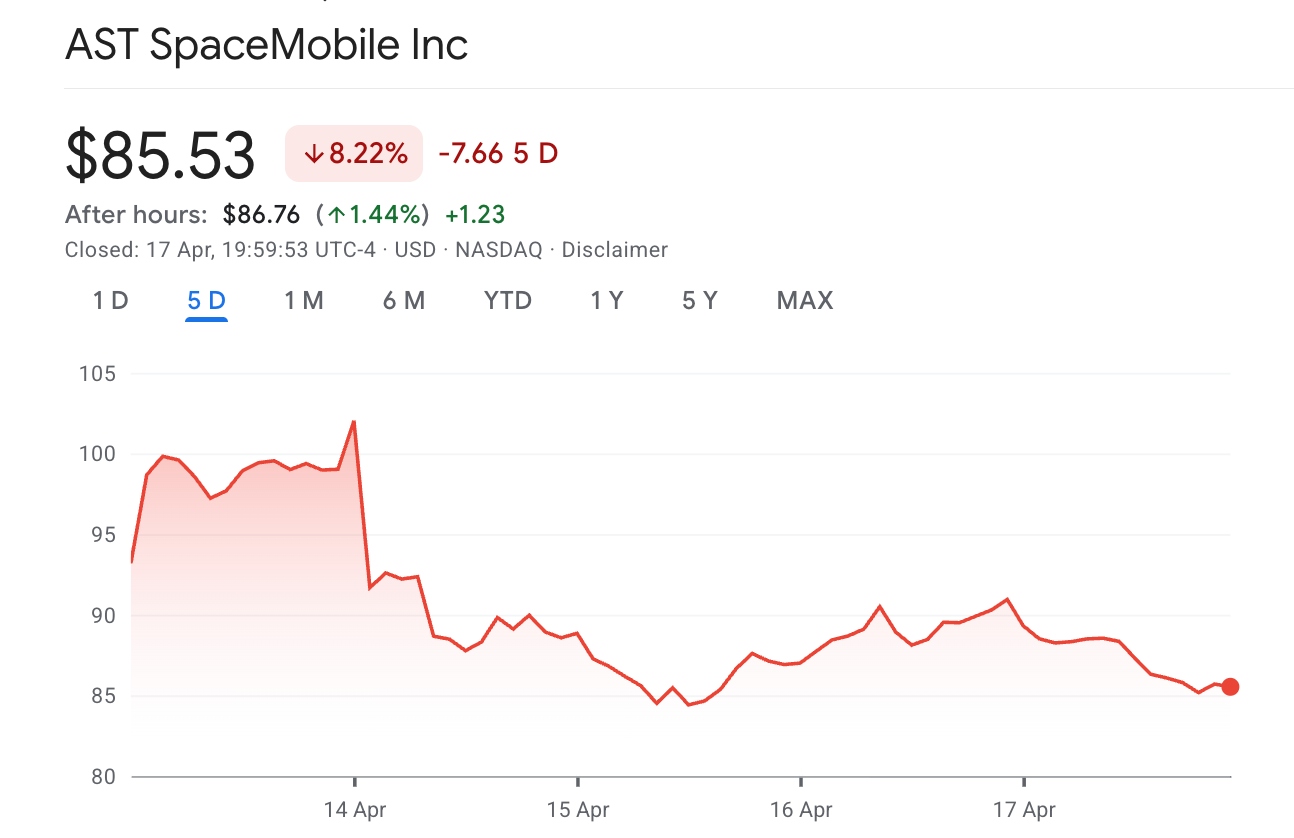

[ASTS stock price trend over the past week; Source: Google Finance]

Following the news, ASTS shares plunged more than 17% in overnight trading. Over the past week, ASTS has seen a cumulative decline of nearly 10%.

Reasons for AST SpaceMobile's decline over the past week?

AST SpaceMobile's recent decline has been driven by a confluence of negative sentiment.

On April 14 and 15, billionaire Rakuten Group founder Hiroshi Mikitani sold a total of 3.04 million shares of ASTS over two consecutive days, netting approximately $271 million. Simultaneously, insiders reduced their holdings in tandem; on April 17, reports surfaced that several executives and directors cashed out at price highs, causing the stock to drop another 5.9% to $84.91 that day.

Furthermore, on April 14, Eastern Time, Amazon (AMZN) announced it would acquire Globalstar for approximately $11.6 billion. Globalstar is a key partner for Apple's emergency satellite SOS feature on the iPhone and possesses valuable low-band spectrum resources. Amazon’s aggressive entry, backed by the financial strength of its e-commerce and cloud computing businesses, directly challenges the narrative logic of ASTS as an "independent direct-to-cell satellite operator."

Can AST SpaceMobile’s valuation premium persist?

Although ASTS stated that the satellite was insured and that the one-time financial loss would be covered, the consequences of this failure extend far beyond the loss of a single satellite.

ASTS originally planned to complete the deployment of 45 to 60 satellites by the end of 2026 to achieve its commercialization goals for the second half of that year. BlueBird 7 was the first satellite to be launched via a Blue Origin rocket and marked the debut of mass production for the Block 2 BlueBird satellites. This failure necessitates a rescheduling of the launch plan; combined with the rapid advancements of SpaceX and Amazon, ASTS's "window of opportunity" is being increasingly compressed.

ASTS's Q4 2025 revenue surged 2,731% year-over-year to $54.3 million, with 2026 revenue guidance of $150 million to $200 million and a 2027 target of nearly $1 billion. However, at a market capitalization of approximately $34 billion, ASTS's projected 2027 EV remains as high as 34x, while the market's 2027 EV expectation for SpaceX is roughly 27x to 34x.

Scotiabank analyst Andres Coello stated in an April 20 report: "ASTS's design is indeed impressive, but the intense competition, low ARPU, and high capital intensity do not justify the current valuation." He set a price target of $41.20, implying approximately 52% downside from current levels.

What Does AST SpaceMobile’s Launch Failure Mean for SpaceX?

ASTS's plunge and launch failure represent an "indirect positive" for SpaceX, though the magnitude of the impact should not be overestimated.

On the competitive front, SpaceX's lead is being systematically amplified. As of mid-April 2026, SpaceX had completed dozens of successful launches within the year, deploying over 1,000 new satellites, with its direct-to-cell constellation already exceeding 650 satellites.

On April 8, the FCC granted SpaceX conditional approval to provide direct-to-cell SMS services to U.S. users via its second-generation Starlink satellites; meanwhile, Starlink's fixed broadband subscribers have reached approximately 10 million.

From a valuation perspective, the discount on ASTS may highlight SpaceX's relative valuation attractiveness. Furthermore, SpaceX's Starlink enjoys a first-mover advantage and is significantly more mature than ASTS; consequently, SpaceX's valuation is expected to surpass that of ASTS.

In addition, market analysts believe that SpaceX's high retail allocation of 30%, its dual-class share structure control arrangement, and its institutional advantage of potential rapid inclusion in the Nasdaq 100 Index will further consolidate its position as the "preferred global satellite communications asset."

In terms of profitability, SpaceX demonstrates an insurmountable lead. SpaceX has entered an expansion phase of "diminishing marginal investment-to-output," while ASTS remains in an early stage of "high investment, high losses, and zero profit."

ASTS's full-year 2025 revenue was only about $70.9 million, with an operating margin of approximately -482% and capital expenditures reaching nearly $400 million; meanwhile, SpaceX's Starlink business saw 2025 revenue reach approximately $11.4 billion with an EBITDA margin of around 54%, achieving positive self-sustainability.

Just 18 months ago, ASTS was a pre-commercial company with zero revenue. Although it has since crossed the commercialization threshold, it still faces a long and uncertain path toward achieving large-scale deployment and profitability.

For SpaceX, Starlink already leads across scale, technology, capital efficiency, and regulatory progress. The crisis at ASTS has instead reinforced the "winner-takes-all" narrative for SpaceX in the satellite communications sector.

Recommended Articles