Applovin Corp Stock (APP) Moved Down by 3.33% on Jun 17: Key Drivers Unveiled

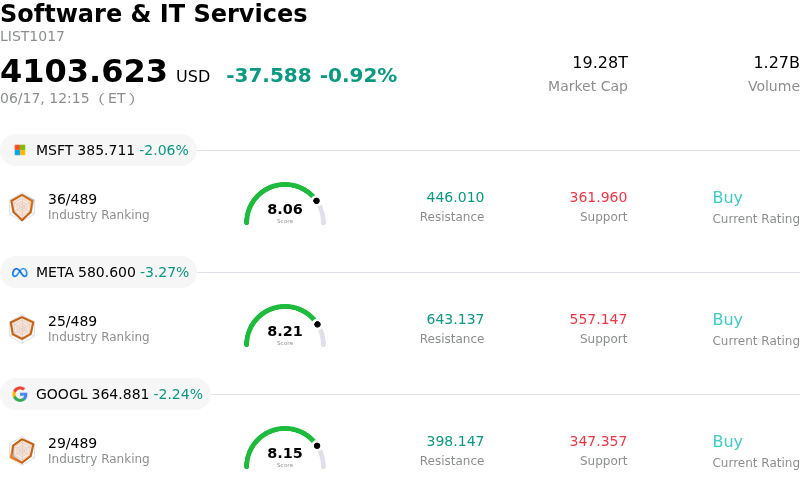

Applovin Corp (APP) moved down by 3.33%. The Software & IT Services sector is down by 0.92%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) down 2.06%; Meta Platforms Inc (META) down 3.32%; Alphabet Inc Class A (GOOGL) down 2.35%.

What is driving Applovin Corp (APP)’s stock price down today?

AppLovin Corporation is experiencing notable downward pressure and heightened intraday volatility, primarily driven by a convergence of sector-wide headwinds, accelerated insider selling, and execution anxiety surrounding its upcoming, highly anticipated platform transition.

The primary systemic headwind stems from persistent weakness within the broader technology and software-as-a-service sectors. In mid-2026, the software sector has faced a wave of multiple compression and capital reallocation. While AppLovin's underlying financial fundamentals remain strong—bolstered by robust first-quarter earnings and optimistic guidance—high-beta growth equities have borne the brunt of this risk-off sentiment. Investors are shifting capital away from highly valued software companies, which has exacerbated the stock's downward trajectory.

Adding to the negative market sentiment is a series of substantial insider liquidations. Recent regulatory filings revealed that high-level executives, including Chief Executive Officer Arash Foroughi, the chief financial officer, and other key board members, have collectively sold a massive volume of shares. Notably, the CEO liquidated over 74,000 Class A shares in mid-June, while other corporate officers also trimmed their holdings. Although scheduled insider selling is common, the concentration of these high-value executive sales has amplified market anxiety and raised questions regarding management's short-term confidence.

Furthermore, the market is highly divided over the imminent public launch of AppLovin's Axon advertising platform. The company is set to open its AI-driven ad engine to advertisers worldwide for the first time in fourteen years, shifting from a closed, referral-based system to a global, self-serve model. While bulls view this transition as a massive growth catalyst that could unlock billions in new advertising spend, bears and risk-averse analysts warn of severe execution and scaling risks. Onboarding a sudden influx of diverse global advertisers raises the potential for system friction, operational breakage, and performance dilution, leading to heightened pre-launch anxiety and price volatility.

In tandem with these operational worries, AppLovin is navigating escalating competitive and regulatory headwinds. The company's proprietary algorithms and competitive moat face pressure from alternative open-source solutions and competitive artificial intelligence model releases. At the same time, because of its heavy operational reliance on AI-driven tracking and consumer profiling, AppLovin is facing growing global compliance and data privacy regulatory scrutiny.

Finally, recent institutional disclosures have shown that prominent funds are trimming their exposures to the stock. Major institutional investors, such as Fred Alger Management and Russell Investments, reported reducing their respective stakes in AppLovin, adding to the structural sell-side pressure. Together, these compounding factors—macro sector rotation, executive selling, execution uncertainty, and rising regulatory risks—continue to drive the stock's recent decline and intraday turbulence.

Technical Analysis of Applovin Corp (APP)

Technically, Applovin Corp (APP) shows a MACD (12,26,9) value of -19.205, indicating a neutral signal. The RSI at 49.373 suggests neutral condition and the Williams %R at 71.200 suggests sell condition. Please monitor closely.

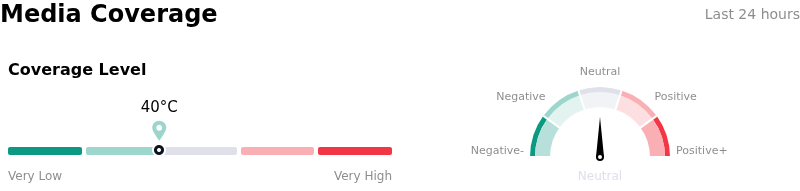

Media Coverage of Applovin Corp (APP)

In terms of media coverage, Applovin Corp (APP) shows a coverage score of 40, indicating a low level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Applovin Corp (APP)

Applovin Corp (APP) is in the Software & IT Services industry. Its latest annual revenue is $5.48B, ranking 56 in the industry. The net profit is $3.33B, ranking 18 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $652.05, a high of $860.00, and a low of $340.00.

More details about Applovin Corp (APP)

Company Specific Risks:

- Accelerated Insider Share Liquidations: Recent SEC Form 4 filings from mid-June 2026 disclose intensive insider selling, highlighted by CEO Arash Foroughi liquidating over 74,000 Class A shares (valued at more than $14.6 million) and Chief Administrative Officer Victoria Valenzuela selling 20,000 shares. This sustained executive exit has compromised market confidence and accelerated downward technical pressure.

- Systemic and Dilution Risks of the Global AXON Rollout: The transition of AppLovin’s proprietary AXON AI ad engine to a global, self-serve model in late June 2026 introduces severe execution risks. Analysts warn of potential system "breakage," operational friction during self-serve onboarding, and ecosystem dilution as the company opens its historically closed, referral-only gaming network to millions of unvetted web and consumer advertisers.

- Ongoing Federal Probe and Data Scrutiny: AppLovin remains under pressure from an active SEC investigation into its consumer data collection and tracking practices. Because the business relies heavily on AI-driven tracking and targeted consumer profiling, the regulatory overhang and potential compliance penalties create significant structural risk to its core algorithms.

- Erosion of Proprietary Moat from Rival AI Systems: The company's competitive advantage in mobile and gaming ad tech is increasingly challenged by emerging open-source technologies, such as the CloudX supply-side platform, and competitive AI gaming and software products like Google's Genie. Analysts caution that these rival technologies threaten to commoditize AppLovin's software and compress its elevated profit margins.

Recommended Articles