Prediction: This Will Be Sandisk's Stock Price by the End of 2027

Key Points

Since Western Digital spun the company off in early 2025, shares of Sandisk have been on a historic rally.

Strong demand for NAND flash storage and enterprise solid-state drives is bolstering Sandisk's revenue and profitability.

Sandisk has begun signing multiyear supply agreements with large customers, providing it with a high degree of visibility into its future finances.

- 10 stocks we like better than Sandisk ›

The memory and storage segment of the semiconductor sector is in the midst of a powerful boom, fueled by the artificial intelligence (AI) infrastructure build-out. With hyperscalers and others pouring hundreds of billions of dollars into new data centers, demand for high-capacity solid-state drives (SSDs) is far outpacing the world's capacity to manufacture them. As a leading producer of NAND flash storage and enterprise SSDs, Sandisk (NASDAQ: SNDK) has been one of the clearest beneficiaries of this movement.

So far this year, Sandisk stock has surged 873% -- making it the top-performer in the Nasdaq-100 by a wide margin. While such gains might suggest to some that Sandisk's rally has become overdone, a close look at the company's operational trends and valuation points to the potential for further upside.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Let's dig into what the next year could look like for Sandisk investors. Spoiler alert: The stock could still be a multibagger from here.

Breaking down the memory up cycle's tailwinds

The primary driver behind Sandisk's rise is big tech's insatiable demand for memory and storage solutions. AI training clusters require vast quantities of high-performance storage alongside accelerated compute systems, and data center operators are deploying those systems at a prodigious pace.

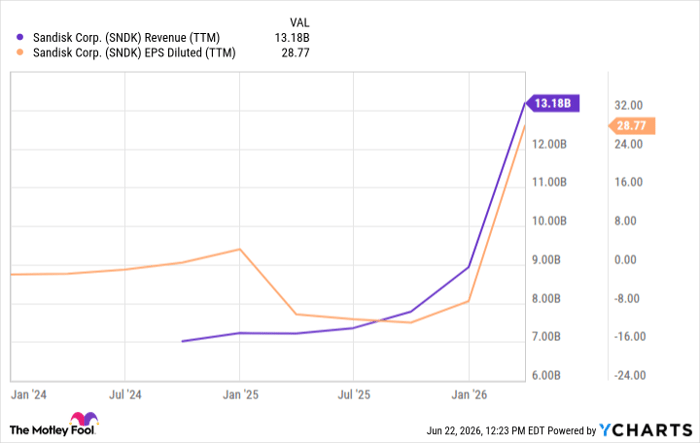

Also, large enterprises and cloud infrastructure providers are refreshing their aging servers by adding denser, faster SSDs; meanwhile, consumer demand for premium AI-enabled devices supports baseline volumes. The imbalance between supply and demand has allowed all of the memory makers to boost their average selling prices significantly. That has translated into noticeable profit margin expansion and top-line momentum for Sandisk.

SNDK Revenue (TTM) data by YCharts.

New contract structures give Sandisk strong earnings visibility

One of the bearish talking points surrounding an investment in Sandisk is the cyclical nature of the memory and storage chip market. While this argument has some validity, Sandisk has made an interesting move that suggests that the memory and storage solutions markets are becoming more secular in the context of the broader AI infrastructure narrative.

Sandisk's management recently highlighted its new business model, which features multiyear supply agreements that provide the company with exceptional visibility into its future sales and profits -- something it historically lacked. During Sandisk's fiscal third-quarter earnings call, management shared that the company has signed five multiyear supply agreements this year -- and just the three it inked in its most recent fiscal quarter carry a minimum total value of $42 billion.

The resulting backlog and contracted performance obligations extend Sandisk's runway well into 2028 and beyond -- materially reducing its cyclical risk. For this reason, the analysts' consensus points to earnings per share (EPS) of approximately $65 in fiscal 2026, followed by a step-up to roughly $183 next year as its volumes scale further and its margins continue to widen.

Image source: Getty Images.

Where will Sandisk stock be in one year?

Sandisk's forward price-to-earnings (P/E) multiple has expanded significantly throughout 2026. While rapid multiple expansion can sometimes signal froth, I think Sandisk's current valuation profile remains compelling given the duration and magnitude of the demand outlook.

Should Sandisk continue to meet or exceed its revenue and profitability targets, further upside could be in store even without further multiple expansion. For example, if Sandisk hits analysts' 2027 EPS target of $183 and maintains a forward earnings ratio of around 33, the stock would rocket to about $6,000. That would be 160% above current levels.

Taking this one step further, Sandisk stock could easily continue rising even if its multiples contract or normalize a bit. For instance, if the company generates earnings results consistent with Wall Street's outlook but its forward P/E dips to a level more in line with the average S&P 500 figure of 22, Sandisk stock would still surge to roughly $4,000 per share by the end of next year.

All told, the combination of strong secular tailwinds supported by contracted revenue visibility and compounding earnings creates a compelling setup for share price appreciation. If this memory up cycle persists and the company delivers on its expectations, the stock has a credible path to at least double -- if not gain even more -- by year-end 2027.

Should you buy stock in Sandisk right now?

Before you buy stock in Sandisk, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Sandisk wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $392,713!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,227,782!*

Now, it’s worth noting Stock Advisor’s total average return is 897% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 24, 2026.

Adam Spatacco has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Recommended Articles