June Fed Decision Delivered: Rates Held Unchanged but Dot Plot Significantly Raised, 9 Back Continued Rate Hikes in 2026.

TradingKey - On June 17, Eastern Time, the Federal Reserve's latest interest rate policy statement indicated that it chose to hold rates steady at this meeting, maintaining the federal funds rate in the range of 3.50% to 3.75%, while keeping the monetary policy framework of ample reserves in the banking system unchanged.

Despite disruptions from uncertainties arising from the Middle East conflict, the U.S. economy continued to expand at a solid pace, supported by strong productivity and corporate capital expenditures, a balanced labor market, and a generally stable unemployment rate.

Affected by supply shocks in sectors such as energy, inflation remains significantly above the 2% policy target. The Fed stated that it will hold its policy line and make every effort to restore price stability.

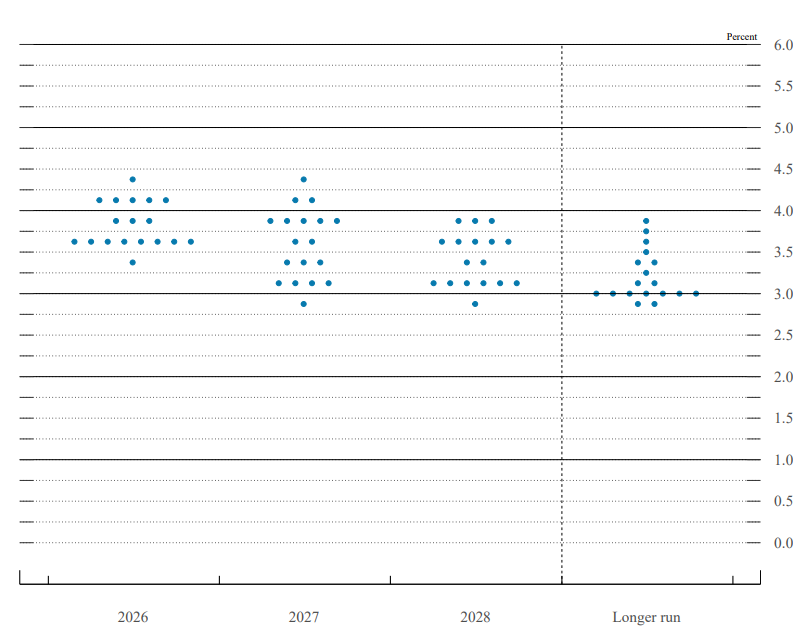

Changes in the dot plot

The dot plot released with this Federal Reserve interest rate decision sent a clear hawkish signal. The median rate on the dot plot was recorded at 3.8%, a sharp upward revision from the 3.4% projected in March.

The dot plot shows a wide distribution of members' projections, with the lowest forecast at around 3.5%, while the most hawkish member believes the appropriate rate for the full year needs to be maintained near 4.5%. The vast majority of members' rate expectations are concentrated in the 3.5%–4.2% range, with only a tiny minority projecting rate cuts below 3.5% this year.

Of the 19 officials, only 18 submitted dot plot projections. Among these 18 officials, one believed there should be a cumulative rate hike of 75 basis points over the remainder of 2026, five favored a cumulative hike of 50 basis points, three supported a cumulative hike of 25 basis points, eight believed rates should be kept unchanged, and one projected a cumulative rate cut of 25 basis points.

Overall, Fed officials now generally expect the number of rate cuts in 2026 to shrink significantly, with only a limited number of cuts initiated during the year. The federal funds rate will remain in high territory for a prolonged period, extending the high-interest-rate cycle.

[Source: Federal Reserve ]

For 2027, the divergence in Fed members' rate projections widens further, with the lowest forecast at around 3.0% and the highest still at 4.4%; the majority of members are concentrated in the 3.1%–3.9% range. This indicates that the Fed will continue on a gradual rate-cut path in 2027, but the overall downward pace of interest rates will be significantly slower than projected in March, as sticky inflation prevents officials from easing rapidly.

In summary, the policy communication framework at this rate meeting has undergone a clear adjustment, and market expectations pricing the future rate path may undergo a reassessment.

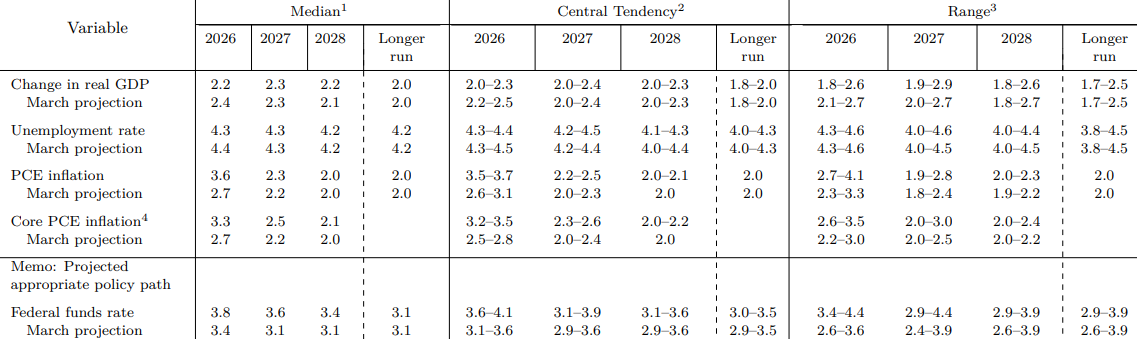

Summary of Economic Projections (SEP)

The Federal Reserve's latest Summary of Economic Projections (SEP) shows that policymakers have slightly upgraded their US economic growth forecasts.

[Source: Federal Reserve ]

In the latest projections, the median forecast for US real GDP growth in 2026 was revised to 2.2%, representing a downward adjustment from the 2.4% projected in March; real GDP growth for 2027 remains unchanged at 2.3%, while the 2028 growth forecast was slightly revised upward to 2.2% (compared to 2.1% in the March projection).

Over the longer term, Fed officials still maintain the US long-term potential economic growth rate at 2.0%, generally anticipating that the US economy will be able to sustain a steady expansion over the next few years.

Regarding the labor market, the Fed's overall unemployment rate projections saw only minor tweaks this time. Policymakers' latest median forecast for the US unemployment rate in 2026 is 4.3%, slightly down from the 4.4% projected in March; the unemployment rate for 2027 remains unchanged at 4.3%, and the projection for 2028 is 4.2%, which is in line with the Fed's long-term equilibrium unemployment rate estimate.

Overall, Fed officials judge that the US labor market will generally remain stable in the coming years without significant deterioration.

On inflation data, the Fed significantly raised its short-term inflation forecasts, indicating that the current pace of cooling prices is slower than the optimistic projections in March, and inflationary pressures remain high relative to the 2% policy target. For headline PCE inflation, officials raised the median forecast for year-on-year growth of the Personal Consumption Expenditures price index in 2026 to 3.6%, significantly higher than the 2.7% projected in March; PCE inflation is expected to fall to 2.3% in 2027, and further down to 2.0% in 2028, ultimately returning to the Fed's long-term inflation target. Core PCE inflation projections, which exclude volatile food and energy components, were also visibly revised upward, with the median core PCE inflation forecast for 2026 rising to 3.3%, far higher than the 2.7% projected in March.

This fully demonstrates that Fed policymakers have reached a consensus that the downward trajectory of inflation in this cycle will be slower than previously anticipated, with inflation stickiness significantly exceeding prior expectations.

Recommended Articles