This Memory Stock Has Doubled in 2026. Here's Why It Can Skyrocket Higher (Hint: It's Not Micron or Sandisk)

Key Points

Lam Research's stock has nearly doubled in 2026, driven by its critical role in the memory industry.

The semiconductor equipment supplier's addressable market is poised to grow rapidly, and that could help the stock soar higher.

- 10 stocks we like better than Lam Research ›

Micron Technology and Sandisk have delivered stunning gains to investors in 2026, driven by favorable memory market dynamics where demand is significantly outpacing supply.

Artificial intelligence (AI) data centers have been quickly cornering the available supply of memory chips, creating a substantial shortage for other applications such as smartphones, vehicles, personal computers, and gaming consoles. Moreover, supply constraints are unlikely to go away anytime soon, as demand for AI-focused high-bandwidth memory (HBM) is expected to increase at an annual rate of 30% through 2030.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

As HBM is manufactured by vertically stacking multiple memory dies into a single package, it requires thrice the wafer capacity needed to make conventional memory. As a result, the strong pricing environment powering Micron and Sandisk's rally seems sustainable. However, there's another memory-focused AI stock -- Lam Research (NASDAQ: LRCX) -- that's benefiting from booming memory demand.

Its shares have nearly doubled in 2026 already, and there is a solid chance that it will deliver more upside. Let's see why.

Image source: Getty Images.

Lam Research will benefit from the massive investments in memory infrastructure

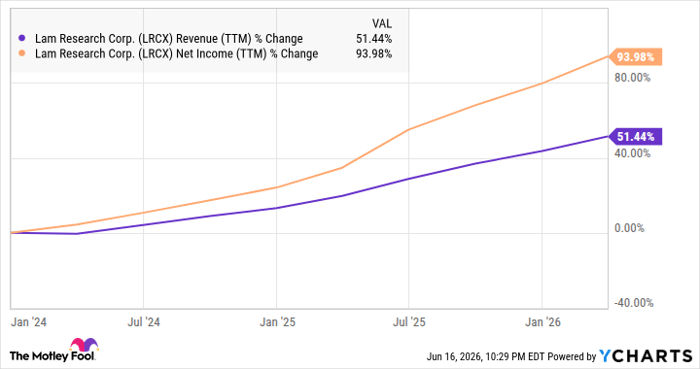

Lam Research is a semiconductor equipment supplier that derives a significant share of its revenue from the sale of memory manufacturing equipment. The company got 39% of its revenue from the memory segment in the third quarter of fiscal 2026 (which ended on March 29). This explains why Lam Research has been clocking healthy growth over the past two and a half years.

Data by YCharts

The ongoing memory shortage should ensure that Lam continues to grow at a solid pace. In fact, it won't be surprising to see its growth accelerating. After all, major memory manufacturers are going to significantly increase their investments to bring additional capacity online. SK Hynix, for instance, is planning to double its wafer capacity over the next five years. Meanwhile, Micron Technology is on track to spend $25 billion in capital expenditure this fiscal year, up significantly from $13.8 billion last year.

Not surprisingly, JPMorgan substantially increased its memory capex forecast for 2027 to $144 billion in March this year, compared to the earlier estimate of $83 billion issued in September 2025. Don't be surprised to see elevated levels of AI capital spending continuing beyond next year, as the memory shortage is expected to persist until 2030.

The market seems to be underestimating the company's growth potential

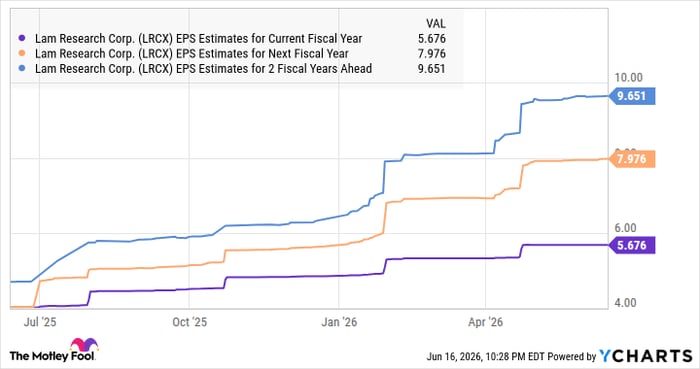

Lam's earnings are projected to grow by 37% in the current fiscal year to $5.68 per share, followed by a stronger 40% jump in the next one, according to consensus estimates sourced from Yahoo! Finance. However, the growth rate is expected to slow down after a couple of years.

Data by YCharts

But the massive memory demand and the resulting investments in machines needed to fill the supply gap suggest that Lam's growth could be much stronger than analysts anticipate. Of course, Lam stock's red-hot rally has made it expensive. Its forward earnings multiple of 49 is well above the tech-focused Nasdaq-100 index's forward earnings multiple of 26.6.

However, investors should look past the valuation, as the increasing outlay on memory equipment can help Lam consistently crush Wall Street's expectations in the coming years, paving the way for further upside in the stock price.

Should you buy stock in Lam Research right now?

Before you buy stock in Lam Research, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lam Research wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $424,531!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,273,016!*

Now, it’s worth noting Stock Advisor’s total average return is 940% — a market-crushing outperformance compared to 209% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 17, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Lam Research and Micron Technology. The Motley Fool has a disclosure policy.

Recommended Articles