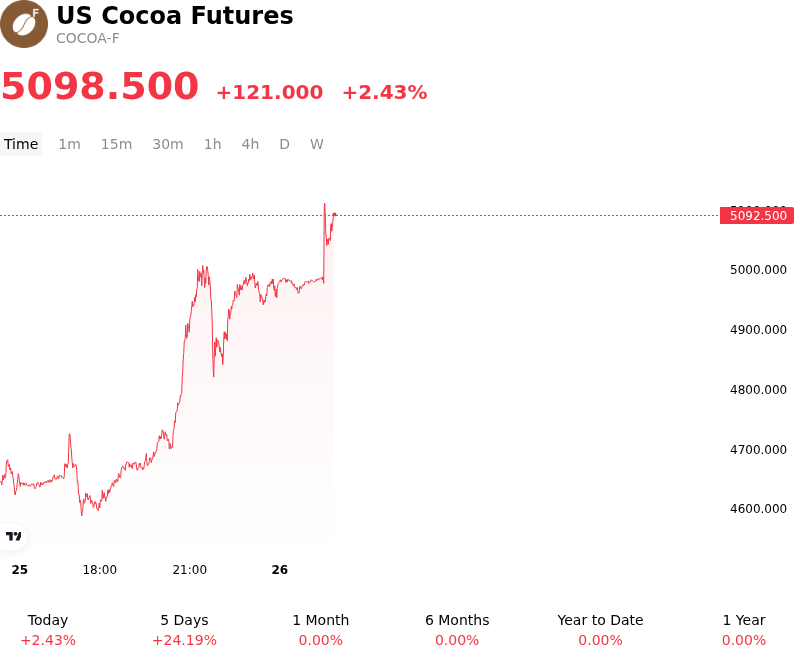

US Cocoa Futures (COCOA-F) Is up 2.43% on Jun 25: What Is Driving the Move?

US Cocoa Futures (COCOA-F) is up 2.43% at Jun 25 05:10(ET), now at $5098.5, with a 7-day up of 22.66%.

What is driving US Cocoa Futures (COCOA-F)’s stock price up today?

Cocoa futures moved higher, extending their multi-week rally and trading near five-month highs. This upward momentum was primarily driven by compounding supply-side disruptions in West Africa and heightened meteorological risks for the upcoming crop cycle, which triggered extensive short covering and technical buying from institutional investors.

The most immediate catalyst for the price advance is heavy, above-average rainfall across key producing regions in Côte d’Ivoire, the world's largest cocoa producer. While some moisture is necessary, the recent excessive rains have flooded critical transportation routes, restricting farmers' access to plantations and delaying the logistics of bringing the final mid-crop harvest to regional ports. Beyond immediate logistical bottlenecks, prolonged overcast conditions and persistent high humidity have significantly elevated the risk of fungal infections, specifically black pod disease. This disease damages pods, reduces usable yields, and compromises bean quality during the final ripening phase.

Adding to near-term physical constraints is the looming threat of an El Niño weather pattern. Meteorological agencies recently confirmed the formation of El Niño across the equatorial Pacific, with forecasting models pointing to a high probability of a severe event. In West Africa, El Niño typically translates to hotter, drier weather during the crucial developing months of the main crop. Early surveys of the 2026/27 West African crop are already indicating below-average cherelle formation, signaling that the main harvest starting in October could face a substantial supply deficit if soil moisture levels drop.

These climate challenges are compounded by structural and regional production headwinds. Regional export statistics show a notable contraction in cocoa outflows from Nigeria, another major producer, where annual production is forecast to slide. Furthermore, underinvestment in farm rehabilitation, aging cocoa trees, and the long-term impact of previous farmgate price cuts in Côte d'Ivoire and Ghana continue to strain the supply side. Because farmers receive fixed prices that lagged the global market recovery, many lack the capital to invest in fertilizers or disease prevention, leading some to abandon land or seek better returns elsewhere.

On the exchange side, near-term tightness has been reinforced by a steady drawdown in Intercontinental Exchange certified warehouse inventories at major import ports. The reduction in available spot supply has forced commercial hedgers and speculative accounts to cover short positions, providing strong technical support to the upward move. While elevated prices may eventually induce demand destruction in major consumer markets, the immediate focus remains squarely on supply vulnerability and the heightened risk of a deficit in the next crop year, keeping the commodity's path of least resistance tilted upward.

More details about US Cocoa Futures (COCOA-F)

Recent Events and Risks:

- Expanding Port Arrivals in Ivory Coast: Physical cocoa arrivals at Ivory Coast ports reached 1.883 million metric tons as of June 21, 2026, representing an 18% year-on-year increase. This robust pace of deliveries signals a significant recovery in West African supply, countering recent fears of long-term output deficits.

- Multi-Year High Exchange Inventories: ICE-certified cocoa inventories climbed to a 1.75-year high of 2,936,328 bags as of late June 2026. The continued accumulation of physical warehouse stocks points to rising near-term availability, limiting the upside potential of futures prices.

- Demand Destruction and Muted Chocolate Consumption: Global consumption remains heavily constrained by historically elevated retail prices. Top processor Barry Callebaut recently forecast subdued volume growth of just 1% to 3% over the next 12 to 18 months, while North American Q1 cocoa grindings declined by 3.8% year-on-year, highlighting ongoing demand destruction.

- Easing Logistical and Geopolitical Premiums: The reopening of the Strait of Hormuz has begun to ease global shipping rates, fuel surcharges, and insurance costs. The moderation of these logistics-related supply chain expenses is expected to lower overall importing costs for major processors and reduce the built-in risk premium in cocoa futures.

Recommended Articles