- US President Donald Trump says Iran talks to begin Monday after canceling attack

- Gold Price Forecast: Can Gold Hold $4,020 as Fed Rate Hike Expectations Rise?

- Bitcoin Falls Below $63,000; Can US-Iran Negotiations Reverse the Downtrend?

- WTI holds losses around $82.50 on renewed US-Iran diplomatic hopes

- WTI falls below $83.00 despite hostilities in the Middle East

- Amazon Shares Soar 10% After Earnings; Why Investors Are So Excited

Market Review

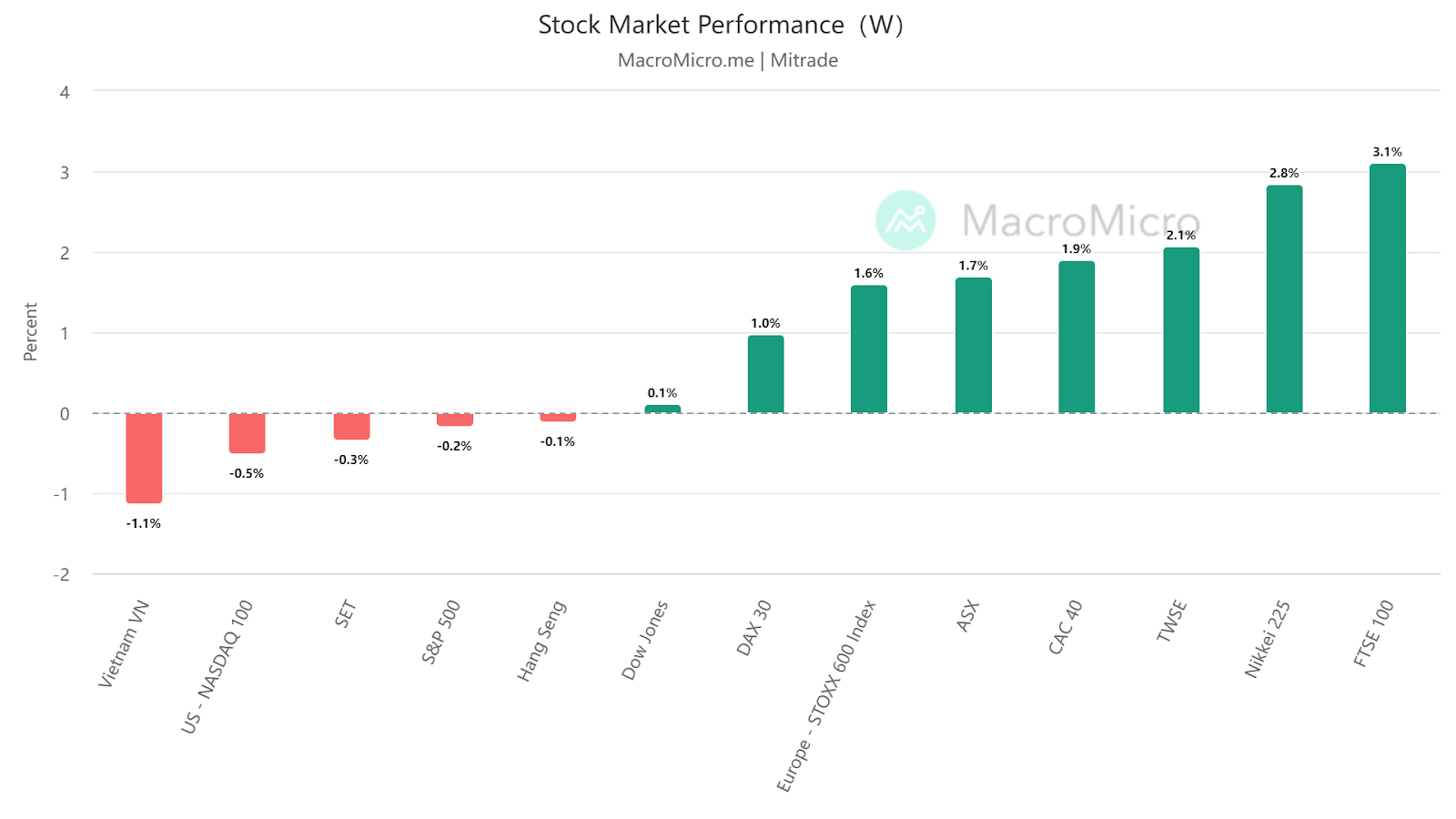

Last week (9/11-9/15), global stock markets showed mixed performance. In the US, the S&P 500 index fell by 0.16%, while the Dow Jones index rose by 0.12%, and the Nasdaq 100 index dropped by 0.51%. In Europe, the STOXX 600 index declined by 1.60%, with the UK's FTSE 100 index recording the highest increase at 3.12%.

【Source: MacroMicro;Date2023/9/11-2023/9/15】

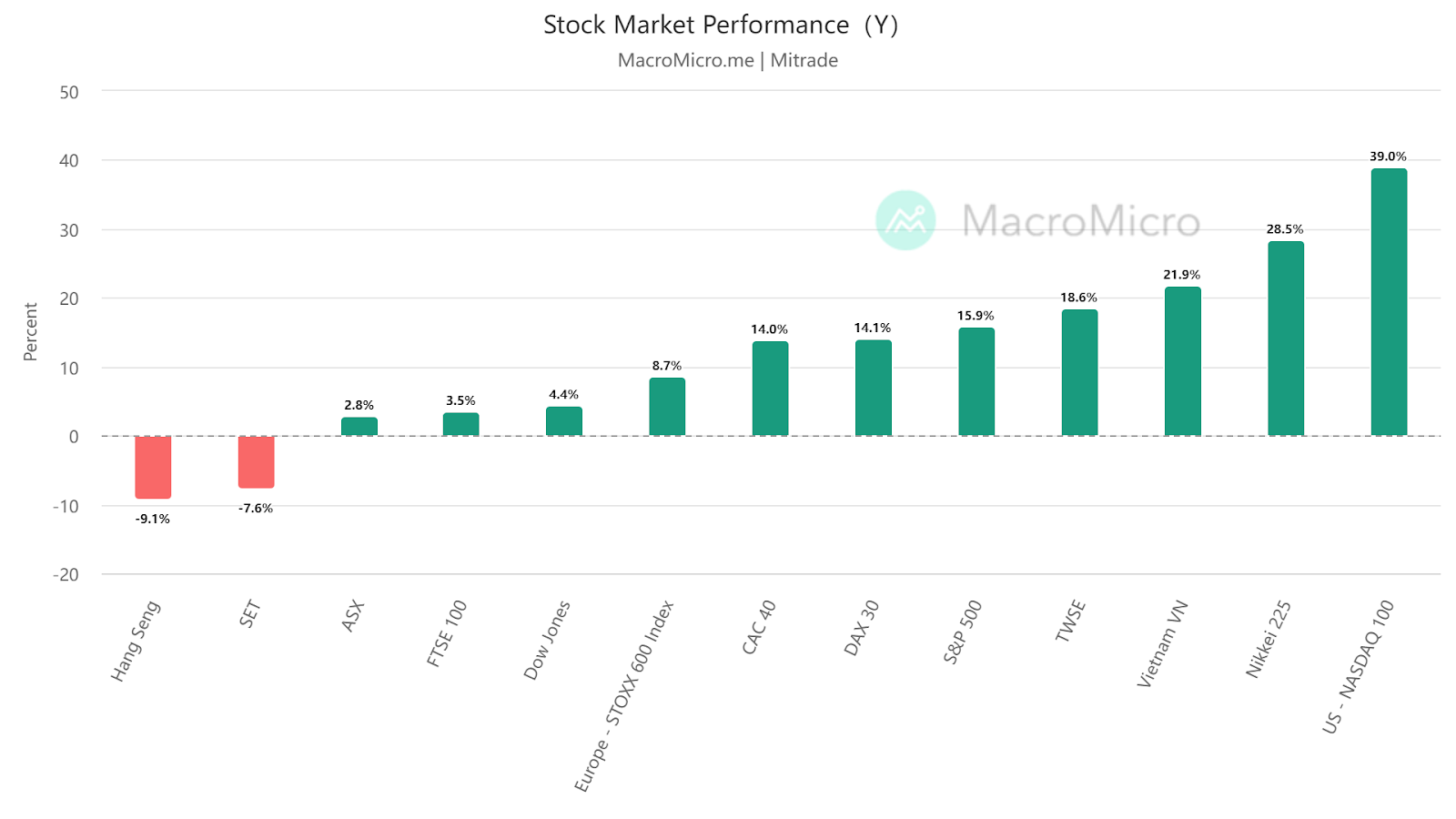

【Source: MacroMicro;Date2023/1/1-2023/9/15】

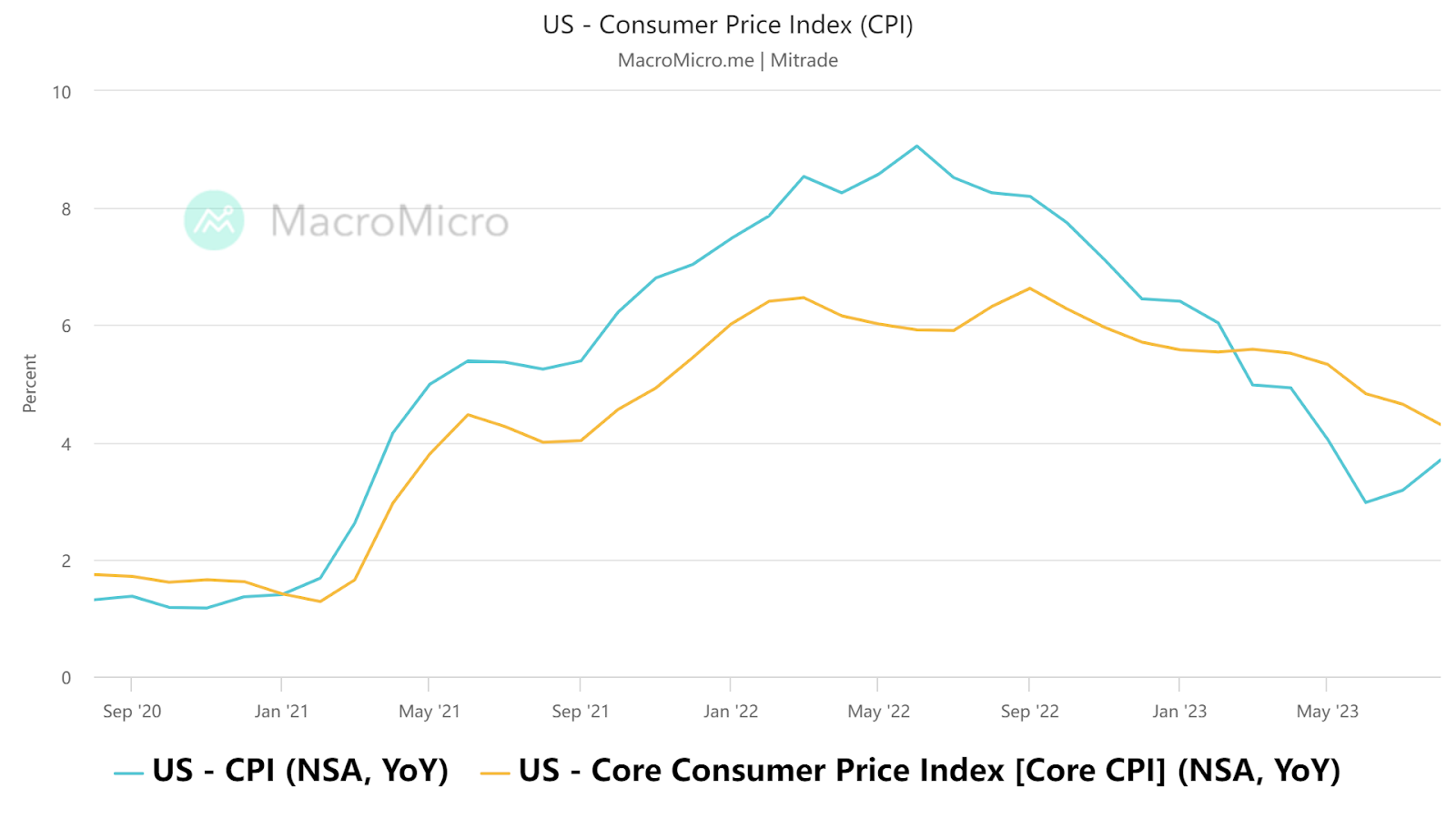

1.US August CPI Rebounds, Will the Federal Reserve Raise Interest Rates Again?

On September 13th, the US Bureau of Labor Statistics released data showing that the year-on-year CPI increase in the US for August rebounded from 3.2% in July to 3.7%, surpassing the expected 3.6%. The month-on-month CPI growth rate also accelerated from 0.2% in July to 0.6% in August.

The core CPI, which excludes energy and food prices, fell from 4.7% to 4.3% year-on-year, marking the smallest increase in nearly two years. However, the month-on-month core CPI increase slightly rose from 0.2% in the previous month to 0.3%, exceeding the expected 0.2%.

【Source:MacroMicro 】

Rising oil prices were the main driving force behind the CPI rebound. Since July, WTI crude oil has risen from $70 to $90, an increase of about 30%. Most analysts expect oil prices to remain high due to tight supply, putting pressure on inflation.

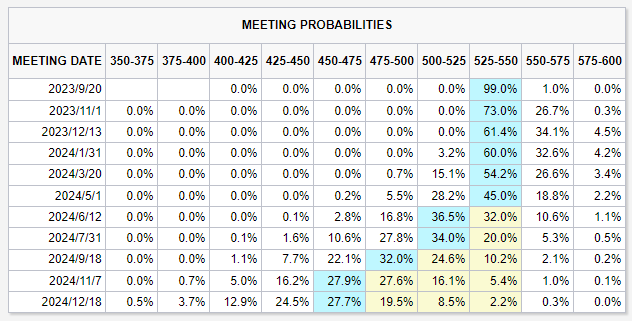

Following the release of the CPI data, market expectations for a Fed interest rate hike increased, with the probability of a rate hike in November reaching 40% at one point. However, as the market digested the data, dovish sentiment resurfaced. Currently, the CME Group's FedWatch tool shows market expectations of a 99% probability of no change in September, 73% probability of no change in November, and 61.4% probability of no change in December. The majority of market participants believe that the rate hikes have reached their endpoint.

【Source:CME】

Mitrade Analyst:

The year-on-year growth rate of core CPI in August retreated, indicating that inflation is still cooling down, although the absolute level remains high, and there was a rebound in the month-on-month core CPI. If the duration of oil price increases is prolonged, the future increase in core CPI could exceed expectations. Therefore, the Federal Reserve may still face pressure to continue raising interest rates within this year.

We anticipate that the Federal Reserve's monetary policy will be "higher for longer," and the current market expectations for Fed rate hikes may be overly optimistic.

2.Economic Data Improving, Will the Shadow of Recession in the United States Dissipate?

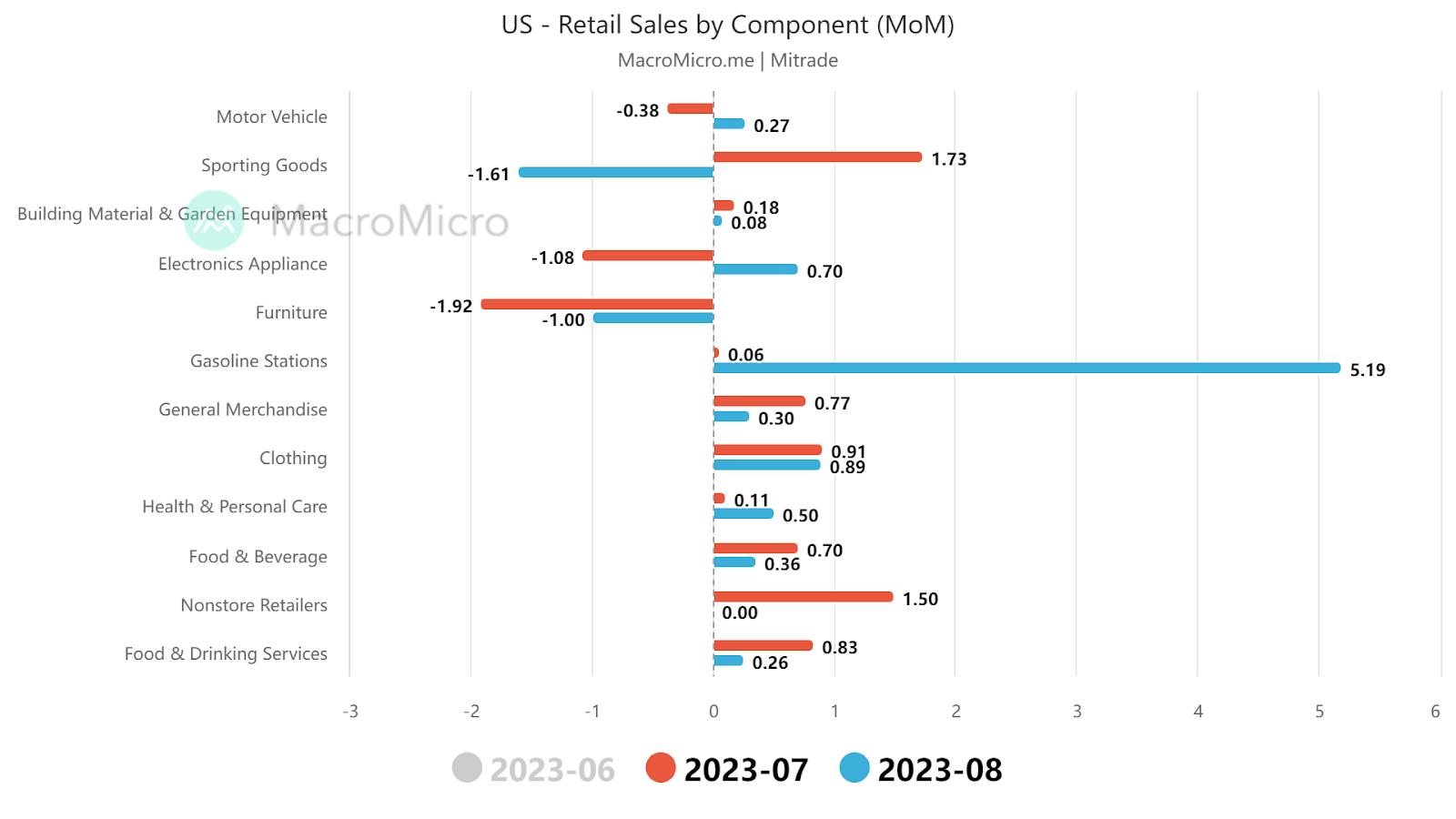

Data on September 14th showed that boosted by strong gasoline prices, U.S. retail sales in August increased by 0.6% compared to the previous month, surpassing the revised value of 0.5% and significantly exceeding market expectations of 0.1%. This marks the fifth consecutive month of growth.

Excluding automobiles and gasoline, core retail sales also exceeded expectations with a month-over-month increase of 0.2%.

【Source:MacroMicro;Gas stations are a key driver of retail growth】

The better-than-expected performance of retail sales, particularly core retail sales, in August indicates that U.S. consumer spending still possesses some resilience, suggesting that GDP growth in the third quarter is expected to remain positive.

Does this imply that the U.S. will avoid a recession in the future? Analysts have varying opinions on this matter.

Some analysts believe that the strong performance of third-quarter GDP does not indicate an increased possibility of a soft landing; in fact, it raises the possibility of negative growth in fourth-quarter GDP. As the fourth quarter lacks the driving forces seen in the third quarter, factors such as the resumption of student loan payments after a three-year pandemic-induced hiatus, rising delinquency rates for consumer loans, and a weak labor market could dampen consumer spending in the fourth quarter.

Morgan Stanley strategist Michael Wilson also believes that U.S. economic growth this year will be weaker than expected, leading to disappointment among U.S. stock investors.

However, the majority of analysts have started to anticipate that the Federal Reserve will revise its outlook for U.S. economic growth to 1.8% or 2% during the release of the economic projections and dot plot of future interest rate paths on September 20th. This would be a doubling of the 1% growth forecasted back in June.

Mitrade Analyst:

After the depletion of excess savings, the labor market will determine whether retail sales can continue to sustain resilience. Currently, the unemployment rate has rebounded, and the labor market is cooling down. Whether it is possible to achieve a "soft landing" in terms of inflation without significantly increasing the unemployment rate remains uncertain.

3.Nasdaq Index Volatile, Focus on This Week's Fed Interest Rate Decision

Last week, the NASDAQ 100 index declined by 0.51% due to the drag from chip stocks. On the news front, Taiwan Semiconductor Manufacturing Company (TSMC) requested its major suppliers to postpone the delivery of high-end chip manufacturing equipment, citing weak economic conditions and soft demand in the end-market.

Currently, chips used in smartphones, computers, and other devices are experiencing a slump, and the demand for AI chips is not strong enough to offset the impact in other sectors. The chip sector is expected to further differentiate in the future, and investors should be mindful of related risks.

Meanwhile, AI-related stocks have recently experienced a correction, primarily due to unclear prospects for monetizing applications and high interest rate pressures.

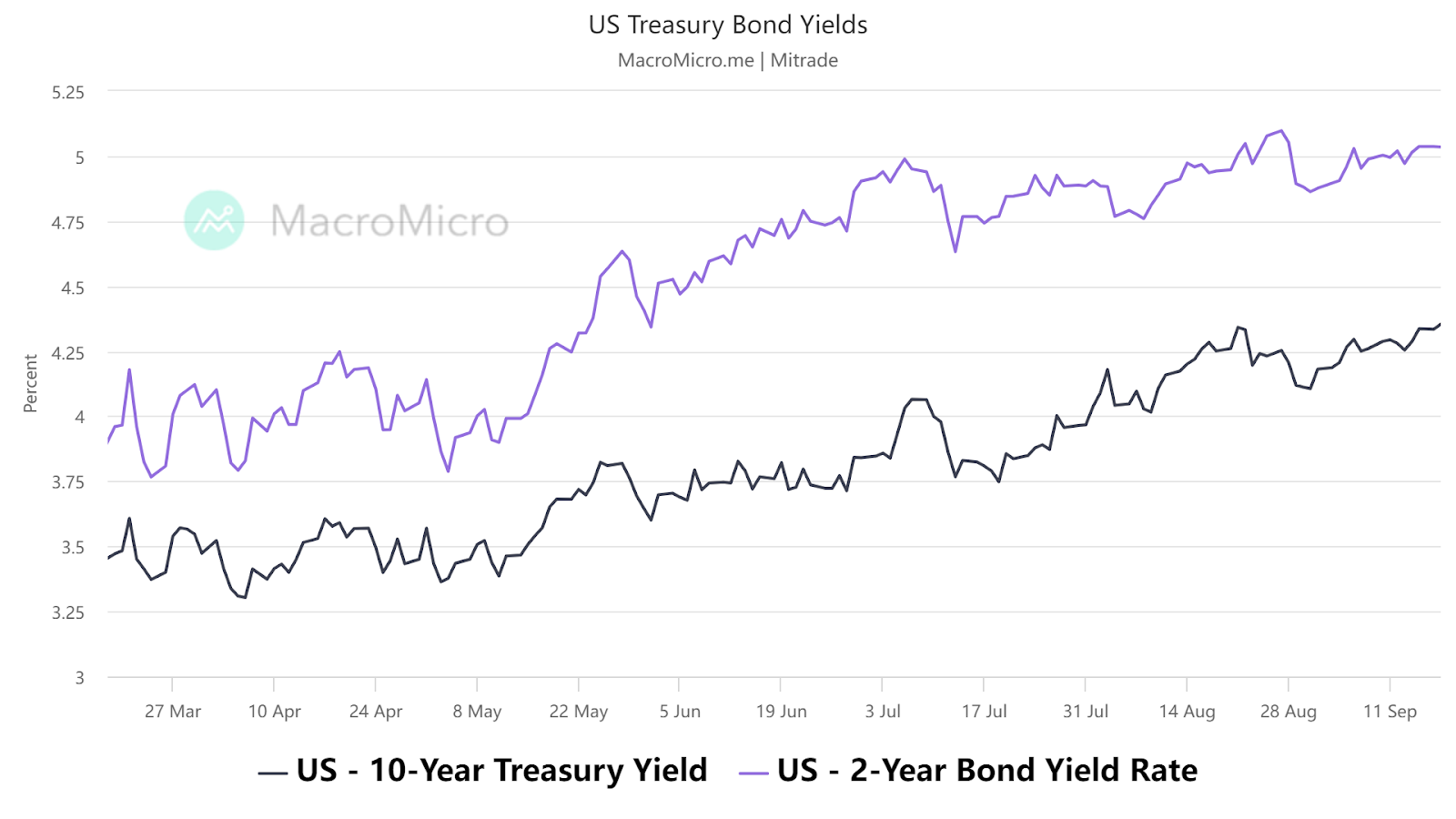

Last week, the yield on the 10-year U.S. Treasury bond approached a three-week high, while the 2-year yield rose above 5.0% for three consecutive days, marking a two-week continuous increase.

【Source:MacroMicro 】

Mitrade Analyst:

The current US Treasury bond yield implies an expectation of a prolonged period of high interest rate policy by the Federal Reserve. Attention is focused on this week's Fed interest rate decision and Powell's speech. If the signals are more hawkish than expected, it will further impact the US stock market. On the other hand, if the information is in line with expectations, it will be beneficial for the stock market.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.