- US President Donald Trump says Iran talks to begin Monday after canceling attack

- Gold rallies to two-week high as USD softens on Iran deal hopes, receding Fed hike bets

- Australian Dollar remains calm following Trade Balance data

- WTI trades with positive bias below mid-$79.00s on Iran uncertainty, supply concerns

- Bitcoin Falls Below $63,000; Can US-Iran Negotiations Reverse the Downtrend?

- WTI holds losses around $82.50 on renewed US-Iran diplomatic hopes

By Jason Tang, Petar Petrov, Viga Liu

Looking ahead to 2025, in the context of robust economic growth, we are bullish on global stock markets, particularly US and Japanese equities.

US Stocks

Although the US stock market has experienced a correction since December 2024, Trump's tax cuts and interest rate cuts remain supportive of the market. We are bullish on the US stock market in 2025.

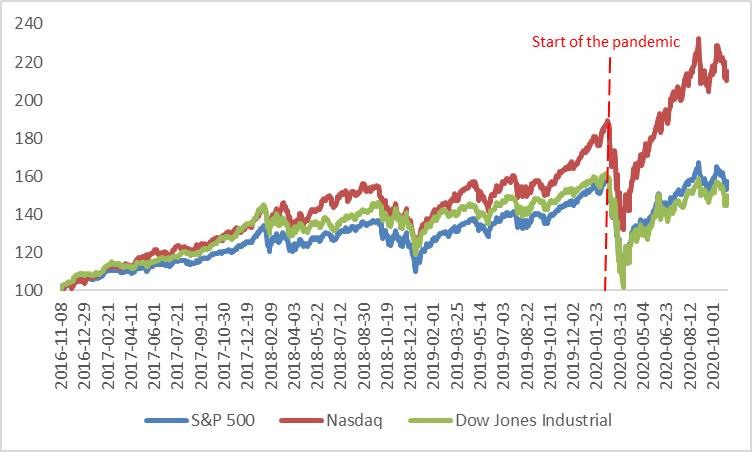

During his first term (from his election on 8 November 2016 to his defeat on 3 November 2020), despite being in a period of the Fed's interest rate hike cycle and the challenges posed by the pandemic, Trump's policies contributed to significant market gains. The S&P 500, Nasdaq and Dow Jones Industrial Average rose by 57.5%, 114.9% and 49.9%, respectively—outperforming the historical averages (Figure 3.1.1). In 2025, Trump's continued push for tax cuts is expected to further benefit the stock market.

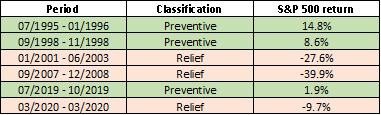

Interest rate cut cycles can be categorized into two types: Relief and Preventive. Of the six interest rate cut cycles in history, three were relief cuts, triggered by economic recessions. During these periods, the negative impacts of the recession outweighed the positive effects of rate cuts, resulting in a stock market decline. The remaining three were preventive rate cuts, implemented in response to economic slowdowns rather than recessions. In these cases, the positive effects of rate cuts were larger than the negative impacts of slower growth, leading to an upward market trend (Figure 3.1.2).

Looking ahead to 2025, the US economy is expected to remain resilient, with a soft landing being a high-probability scenario. As such, this interest rate cut cycle is likely to be preventive, with a net positive effect on the stock market.

However, risks to the US stock market remain. High valuations, the potential for re-inflation and growing public debt could trigger a periodic market decline.

Figure 3.1.1: US stock performance during Trump’s first term

Source: Refinitiv, Tradingkey.com

Note: Re-based 8 November 2016 = 100

Figure 3.1.2: S&P 500 return during rate cut cycles

Source: Refinitiv, Tradingkey.com

Eurozone Stocks

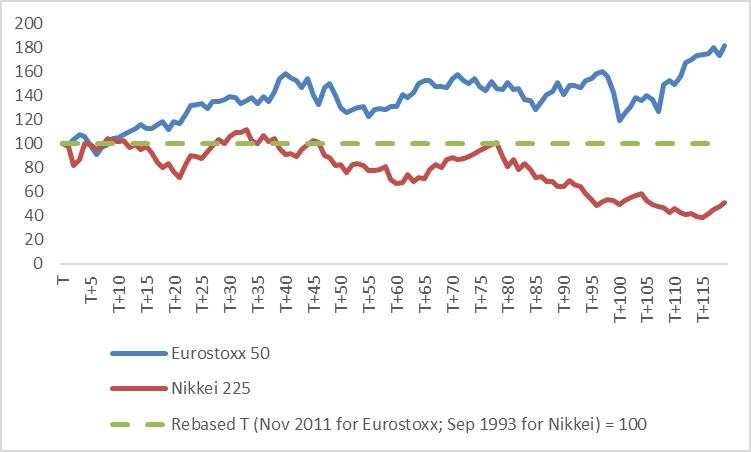

The eurozone is expected to enter a period of low interest rates in 2025. Looking at history, the eurozone began its low-interest rate era in November 2011, one year after the European debt crisis. In the following decade, the eurozone stock market performed relatively well. In contrast, Japan entered its low-interest rate period in September 1993, three years after its asset bubble burst. Over the next decade, Japan's stock market experienced a prolonged bear market (Figure 3.2).

As the eurozone enters this new low-interest rate era, the question arises: Will its stock market follow the path of prosperity seen in the past, or will it mirror the Japanese-style long bear market? To answer this, we need to analyse the underlying factors that influenced the stock markets in both regions during their respective low-interest rate periods.

One key similarity between the two markets is that both attracted foreign capital inflows during their low interest rate periods. However, the Japanese stock market benefited from strong government intervention, while the European stock market saw increased stock investment from the private sector, in contrast to the Japanese private sector, which reduced its stock investment.

That said, in developed markets, private sector investment has been the decisive factor in stock market performance. Therefore, the future performance of the eurozone stock market in 2025 will largely depend on the effectiveness of the eurozone's fiscal and monetary policies. If these policies successfully encourage the private sector to increase stock investments, the eurozone stock market could regain its former strength; otherwise, it may struggle.

Given the uncertainty surrounding the outlook, we assign a neutral rating to eurozone stocks. However, we do caution about potential downside risks, particularly due to Trump’s tariff policies.

Figure 3.2: Eurozone vs. Japanese stock performance during low-interest rate periods (monthly data)

Source: Refinitiv, Tradingkey.com

Japan Stocks

After the economic bubble burst in 1990, the Japanese stock market entered the "Lost Decades" (1990–2010). During this period, while the overall trend was downward, there were three periodic bull markets. Since May 2012, however, Japanese stocks have experienced a sustained and significant bull market (Figure 3.3). The driving forces behind these four bull markets—three short and one long—were shifts in domestic and international policies, as well as improvements in economic expectations both at home and abroad.

Looking ahead to 2025, domestic and international factors suggest a positive outlook for the Japanese stock market. Domestically, while the effects of expansionary fiscal policy may be tempered by contractionary monetary policy, Japan's economic growth in 2025 is projected to significantly surpass that of 2024.

Internationally, major central banks have entered a cycle of interest rate cuts, gradually improving the global financial environment. Meanwhile, the US economy continues to demonstrate resilience and China's economy is recovering, driven by a series of stabilization measures. These global dynamics, combined with domestic improvements, create a favourable environment for the Japanese stock market in 2025.

Figure 3.3: Nikkei 225

Source: Refinitiv, Tradingkey.com

Other stock markets

In addition to major economies, we are optimistic about the stock markets of Australia, Hungary, Indonesia and Taiwan in 2025 for the following reasons:

Australia: Domestic demand is expected to increase and economic growth is projected to accelerate, driven by expansionary fiscal policies. Additionally, China's stimulus measures are likely to boost export demand for Australian products, further supporting economic and stock market performance.

Hungary: After entering a technical recession in mid-2024, the Hungarian government implemented a series of measures to stabilize the economy, creating a favourable environment for the stock market. The Hungarian central bank (Magyar Nemzeti Bank, MNB) has recently adopted a more hawkish stance, which is beneficial to the financial sector—the largest component of the Hungarian stock index. Moreover, two-thirds of the revenue of Hungarian-listed companies comes from overseas markets. These firms are expected to benefit from the continued global economic recovery in 2025.

Indonesia: The Indonesian government has shown greater tolerance for debt, making it more likely to stimulate economic growth through increased financing. A favourable economic outlook is expected to drive earnings growth for listed companies. Indonesian stock valuations are currently well below their 10-year average, making the market attractive for investors.

Taiwan: Taiwan's previously weak consumption has shown signs of recovery and investment activity has rebounded. The semiconductor industry, a cornerstone of Taiwan’s economy, has entered a new inventory replenishment cycle, which is expected to drive investment growth. Technology stocks, including TSMC, have a significant weight in Taiwan's stock index. This high-tech focus makes its stock market trend closely aligned with that of the Nasdaq index. Given our bullish outlook on US stocks, we are similarly optimistic about the Taiwan stock market.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.