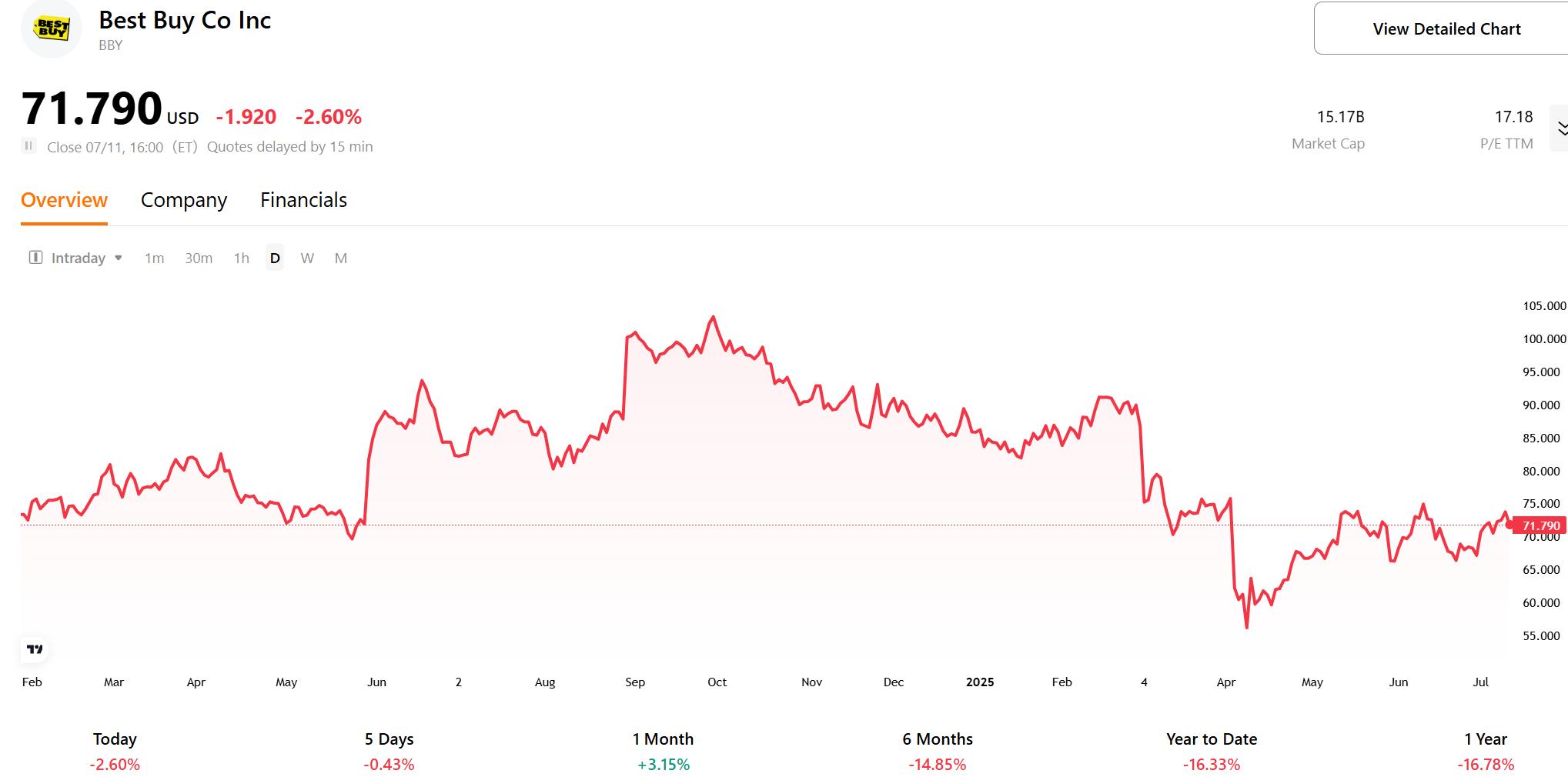

Best Buy: From Retail to Digital Health: Can Diversification Deliver Surprises?

Investment Thesis

TradingKey - Best Buy, a leader in consumer electronics retail, boasts a strong brand and extensive store network. Despite tariff and competitive pressures, its diversified revenue and new strategic initiatives like Best Buy Marketplace, advertising, and health tech investments are expected to drive 2-5% revenue growth in FY26. DCF valuation suggests a target price range of $92.11-$114.14, indicating undervaluation. With robust omnichannel strategies and cost efficiencies, Best Buy presents a compelling investment opportunity.

Source: TradingKey

Source: Best Buy, TradingKey

Company Overview

Best Buy is an American retail company founded in 1966, specializing in the sale of electronics, appliances, and related services. The company operates over 1,000 stores in the United States and Canada, offering a product range that includes computers, smartphones, televisions, audio equipment, and more. Renowned for its professional product knowledge, high-quality customer service, and technical support, Best Buy is a key destination for consumers purchasing electronics. Through innovative retail experiences and diverse services, Best Buy maintains a leading position in the electronics retail market.

Competitor Analysis

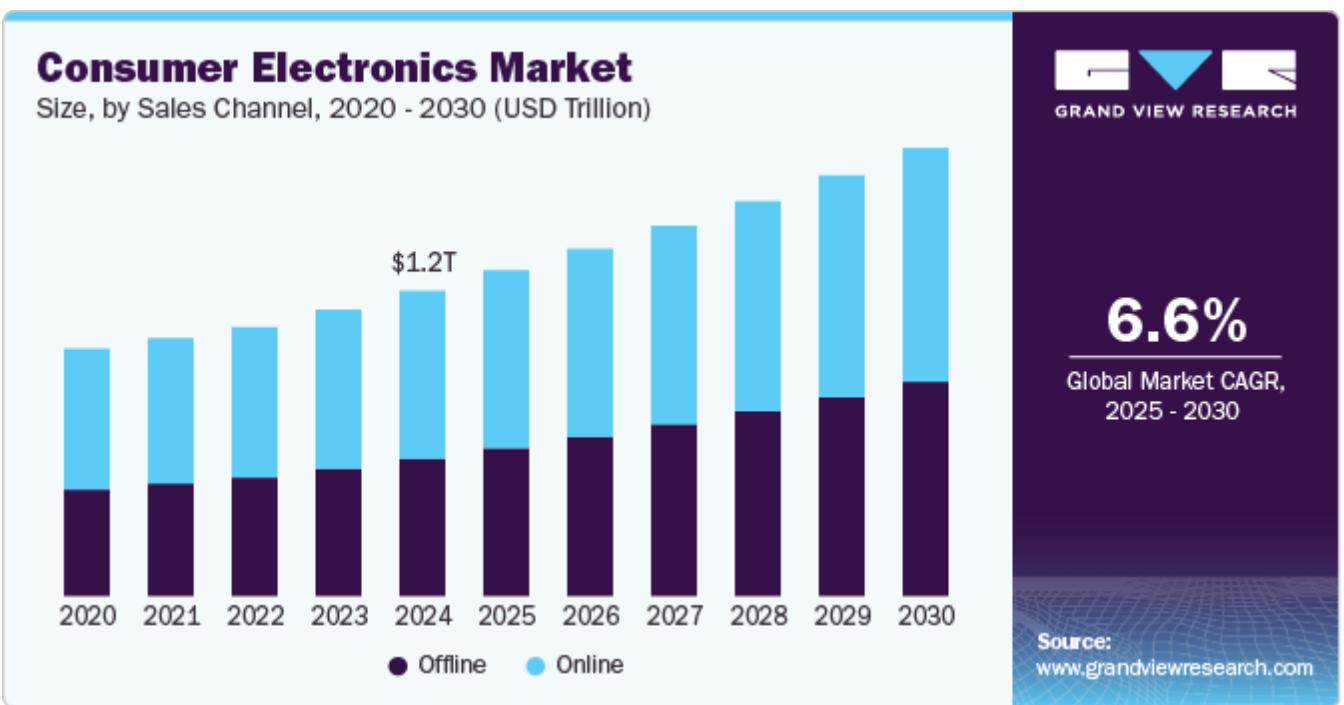

In 2024, the global consumer electronics market was valued at $1,214.11 billion, projected to grow to $1,782.6 billion by 2030, with a compound annual growth rate (CAGR) of 6.6% from 2025 to 2030. Industry growth is driven by rapid technological advancements, rising disposable incomes, and increasing consumer demand for convenience and connectivity.

Source: grandviewresearch

Competitive Landscape: Best Buy operates in a highly competitive consumer electronics retail industry, facing intense challenges from both online and offline retailers such as Amazon, Walmart, Target, and Apple Stores. According to Numerator data, Best Buy and Amazon dominate the market, capturing 30% and 28% of total sales in specific consumer electronics categories over the past year, respectively, making their rivalry particularly fierce. Amazon holds an edge in the online space with its extensive product selection, competitive pricing, and fast delivery. Walmart and Target pose threats with low-price strategies and broad product ranges, while Apple Stores attract a dedicated customer base through premium experiences with Apple products. Amid this competitive landscape, Best Buy maintains its edge through unique strategies and market positioning.

Competitive Advantages: With over 50 years of operational history, Best Buy has built strong brand recognition, establishing itself as a trusted name in consumer electronics. Its network of nearly 1,000 physical stores provides extensive coverage, particularly in rural areas where it outshines competitors, offering customers hands-on product experiences. Best Buy seamlessly integrates its physical stores with its mobile app, creating a smooth shopping experience, and counters price competition with a price-match policy. Exclusive partnerships with brands like Apple, Samsung, and Sony enhance its supply chain and pricing advantages, enabling unique product and service offerings. According to PitchBook data, Best Buy holds approximately 8% of the North American consumer electronics market and commands about 33% of the brick-and-mortar retail segment, underscoring its strong position in physical retail.

Source: numerator

Revenue Breakdown

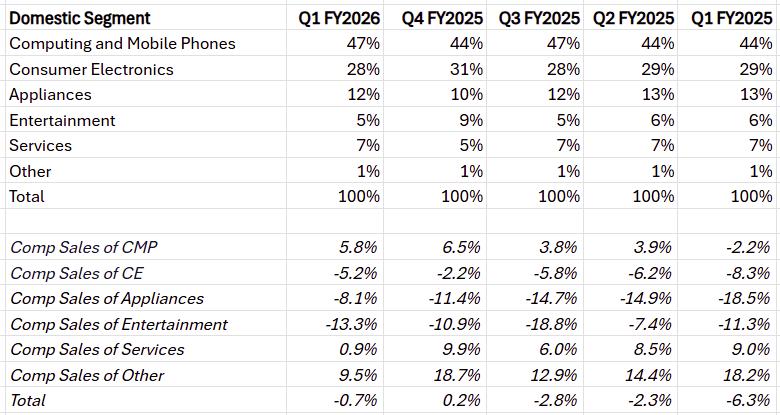

Best Buy’s revenue is heavily reliant on the U.S. market, which accounts for approximately 93% of total revenue, while international markets (primarily Canada) contribute about 7%, underscoring the company’s strategic focus on the U.S. The revenue distribution across product categories is diverse, with Computing and Mobile Phones (including laptops, desktops, tablets, and smartphones) leading at approximately 47%, followed by Consumer Electronics (such as TVs, audio equipment, cameras) at about 28%, Appliances (including refrigerators, washers, dryers, and small appliances) at around 12%, Entertainment (including video games, movies, and music) at about 5%, and Services (such as Geek Squad technical support, installation, and repair services) at roughly 7%. This diversified product mix enables Best Buy to adapt flexibly to changing consumer behaviors and market trends.

Computing and Mobile Phones: Over the past five quarters, the Computing and Mobile Phones category has seen a gradual increase in revenue share, with comparable sales returning to positive growth. This performance is primarily driven by new product launches (e.g., new laptops and smartphones), sustained demand from remote work and online education, and Best Buy’s effective promotional campaigns and omnichannel strategies (e.g., the “Drops” strategy). This category has become a key pillar of the company’s revenue growth.

Consumer Electronics: The revenue share of the Consumer Electronics category has remained relatively stable over recent quarters, though comparable sales have shown slight improvement but remain in negative growth. Market saturation, slower innovation, intense competition from online retailers, and shifting consumer preferences toward other categories have collectively contributed to this category’s lackluster performance, making a strong recovery in the short term unlikely.

Appliances: The Appliances category has experienced persistent declines in comparable sales, though the rate of decline has slowed. Economic factors, such as cautious consumer spending on big-ticket items, combined with supply chain challenges, are the primary drivers of this trend. While market conditions may gradually improve, this category continues to face significant challenges.

Entertainment: The Entertainment category has seen a significant decline in comparable sales, reflecting a long-term shift from physical media (e.g., DVDs and game discs) to digital streaming services. This structural change has diminished the category’s revenue contribution, further marginalizing its role in the overall revenue structure.

Services: The Services category has maintained relatively stable revenue performance, highlighting its importance as a recurring revenue source. This stability is largely driven by the continued growth of the My Best Buy Total membership program, which provides Best Buy with reliable cash flow and enhanced customer loyalty.

Source: Best Buy, TradingKey

Growth Potential

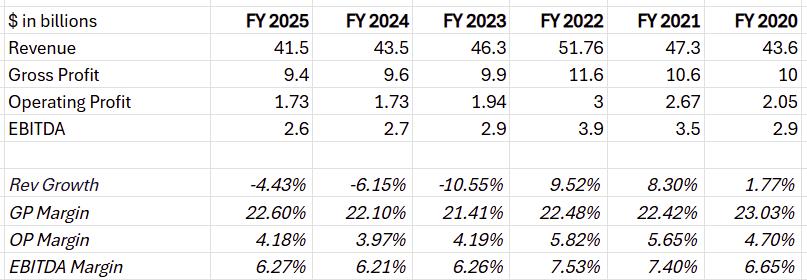

Despite challenges in the consumer electronics market, including a slowdown, rising costs due to tariffs, increased consumer price sensitivity, and adjustments in import sourcing, Best Buy has had to lower its full-year sales and profit forecasts, leading to lackluster stock performance and flat earnings results. However, the company has demonstrated resilience through flexible strategic adjustments, striving to maintain its competitive edge and unlock new growth potential.

· Marketplace Expansion: Best Buy plans to launch the Best Buy Marketplace in the summer of 2025, drawing on its successful experience in Canada, allowing third-party sellers to offer products on its platform. This initiative aims to expand product variety, introduce non-electronic categories, and generate additional revenue through commissions. Currently, online sales account for 32% of domestic revenue (Q1 FY26), and a successful Marketplace rollout is expected to significantly boost online sales performance, driving revenue growth for fiscal year 2026.

· Advertising Business Growth: Best Buy’s management has identified Best Buy Ads as a strategic priority for fiscal year 2026 (FY26), aiming to monetize platform traffic to enhance gross margins. Since its launch, Best Buy Ads has shown strong growth potential through innovative offerings like Social+ and My Ads, as well as partnerships with Meta, CNET, and others. This business not only generates additional revenue but is also seen as a key driver of future profit growth.

· Investment in Health Technology: Best Buy is actively investing in remote patient monitoring and health technology, entering the digital health market, which is projected to grow at a 20% CAGR from 2025 to 2030 (Grand View Research). Successful penetration of this high-growth sector could diversify Best Buy’s revenue streams, potentially contributing $0.5–1 billion in revenue after 2027, further strengthening its financial stability.

· Operational Efficiency and Cost Management: Best Buy continues to reduce operating costs by optimizing its store footprint (planning to close 10–15 underperforming stores) and improving supply chain efficiency. In Q1 FY26, the adjusted operating income margin reached 3.4%, and sustained progress in cost control is expected to directly support profitability growth.

Overall, Best Buy’s performance is poised to stabilize and achieve modest growth in the future, particularly if its new strategies are successfully implemented. The rapid scaling of Best Buy Marketplace and Best Buy Ads could drive 2–5% revenue growth in FY26, with earnings per share (EPS) potentially exceeding $6.30. Leveraging its strengths in customer service, omnichannel integration, and brand recognition, Best Buy is well-positioned to capitalize on evolving opportunities in the consumer electronics market while diversifying revenue through new sectors like health technology. The current valuation may underestimate its long-term potential, presenting a potential growth opportunity for investors.

Source: Best Buy, TradingKey

Valuation

Based on a three-year Discounted Cash Flow (DCF) model, Best Buy’s enterprise value (EV) is estimated to range from $19.471 billion to $24.13 billion, comprising a present value (PV) of $2.307 billion to $2.878 billion and a terminal value (TV) of $16.532 billion to $20.62 billion. The model assumes a revenue growth rate of 0.38% to 0.39%, an operating margin of 2.09% to 2.6%, and a discount rate based on U.S. Treasury yields of 3.84% to 4.20% plus a 2% premium. After subtracting net debt from the EV and dividing by 211.4 million outstanding shares, the target stock price range is $92.11 to $114.14. This valuation reflects Best Buy’s strong position in the consumer electronics retail market and its growth potential driven by marketplace expansion (e.g., Best Buy Marketplace), advertising business, and health technology investments, despite challenges from tariffs and economic uncertainty.

Risk

· Tariff Impact: Potential tariff increases could raise import costs, squeezing gross margins.

· Economic Uncertainty: An economic downturn or reduced consumer spending could lower demand for big-ticket items.

· Competitive Pressure: Low prices and online advantages from retailers like Amazon and Walmart threaten market share.

· Strategic Execution Risk: Failure of Best Buy Marketplace and advertising business to meet expectations could hinder revenue growth.

· Supply Chain Disruptions: Global supply chain issues could impact inventory availability and delivery efficiency.

Get Started

Recommended Articles