AppLovin's Algorithmic Rise: A Lean AI Flywheel with Potential to Scale

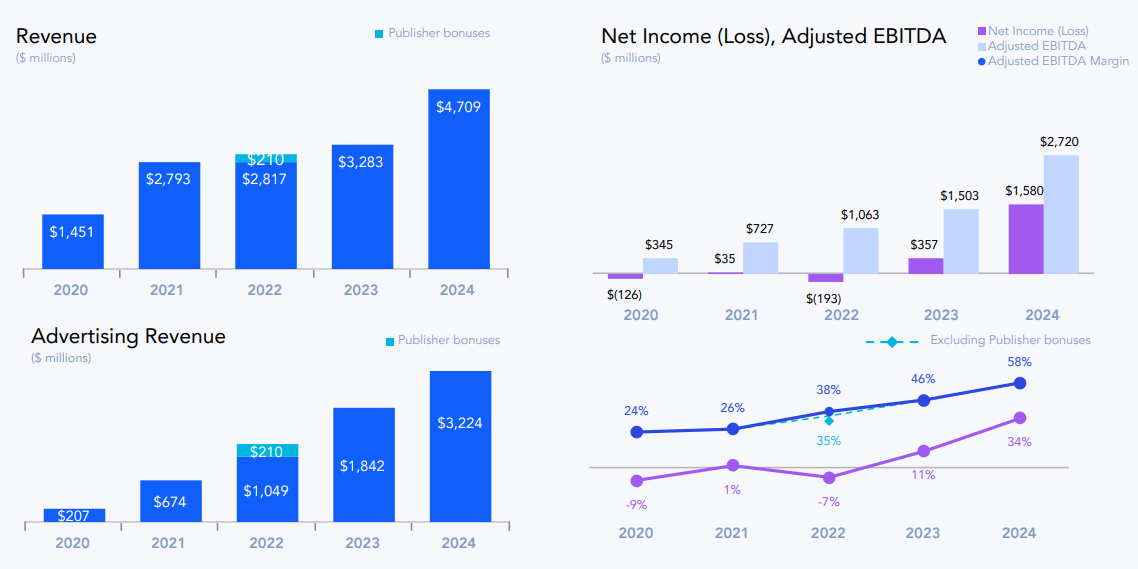

- FY24 net income surged 343% YoY to $1.58 billion, driven by AI-led monetization efficiency and disciplined cost structure across verticals.

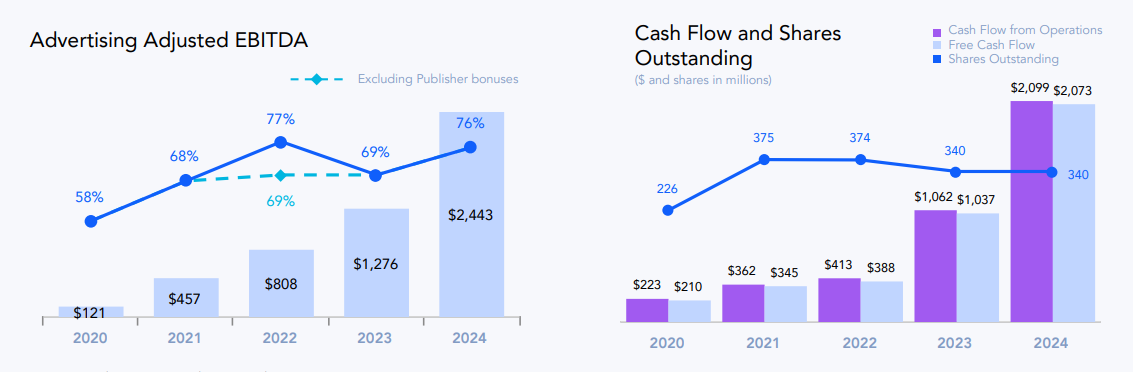

- Axon 2.0 algorithm managed $3.2B in ad revenue, boosting ad segment EBITDA margins to 76%, up from 69% YoY, by automating optimization loops.

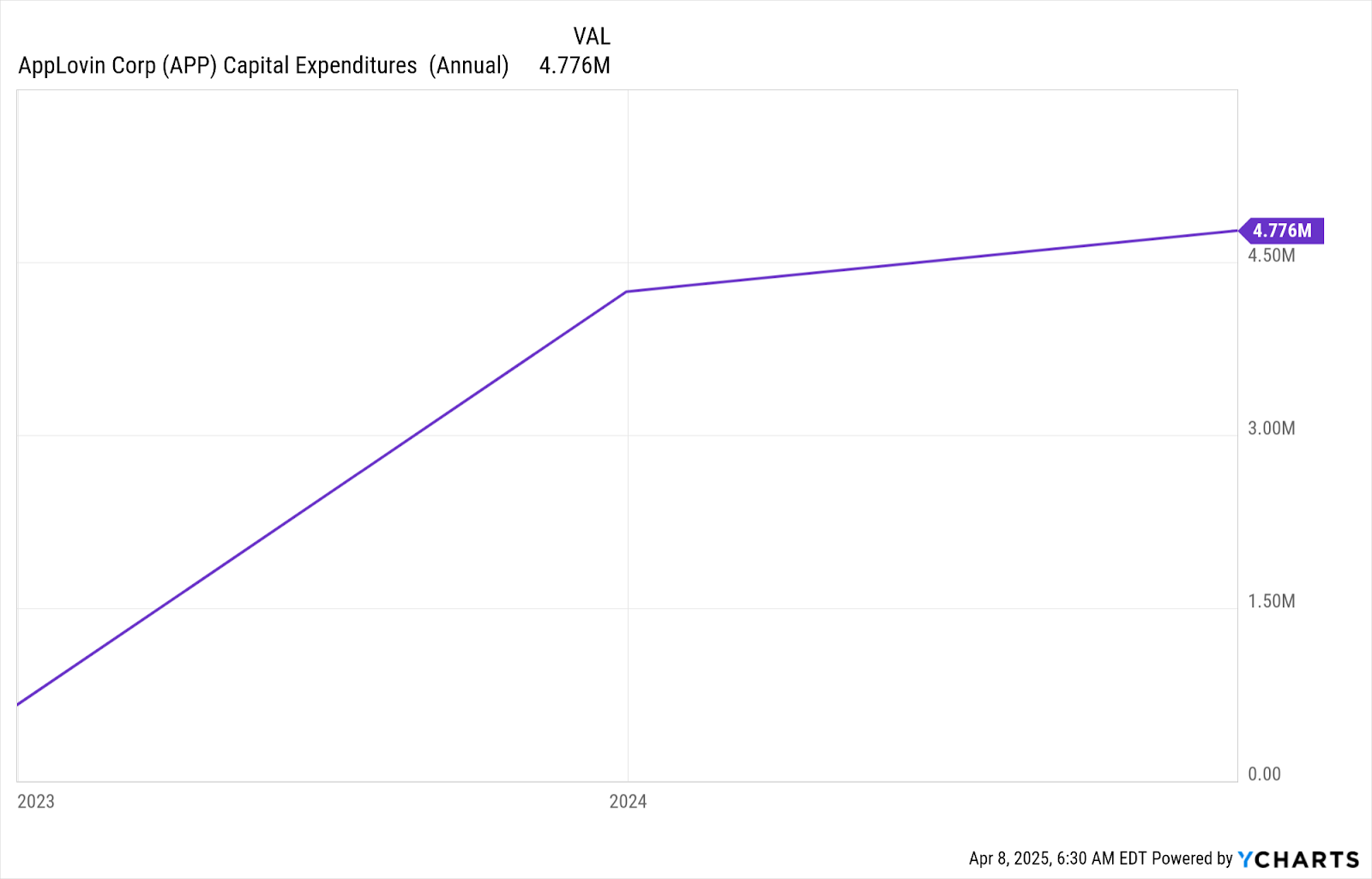

- Generated $2.07B in free cash flow with only $4.8M CapEx in FY24, signaling robust scalability and lean operations with minimal reinvestment needs.

- Executed $2.1B in buybacks while refinancing $4.6B debt at lower rates, maintaining interest expense near $318M with strong coverage.

TradingKey - Whereas most of the market is fixated on user-facing AI platforms or model providers, AppLovin (APP) is a sneakier, but no less effective, beneficiary of the generative AI revolution. Miscategorized as an adtech commodity, AppLovin has become a structural beneficiary in stealth mode through its in-house Axon engine, today fueled by one of the industry's most lucrative advertising AI flywheels. The market has finally taken notice, with the stock up manyfold in the last year, but the valuation still contains skepticism regarding the sustainability of its growth. This is an asymmetric setup: AppLovin marries hyper-profitable AI-driven ad economics with a practically-frictionless scaling model and increasing optionality into Connected TV (CTV) and enterprise self-serve.

With a YoY net income boost of 343% and a YoY growth in adjusted EBITDA of 81% in FY24, AppLovin is not merely surfing macro recovery tides, it's executing a highly choreographed plan around algorithmic monetization and automated scaling. However, even with these strengths, residual risks around customer concentrations, indebtedness, and the commoditization hazard of open source advertising tools keep investors cautious. This article explores the operating mechanics of AppLovin's business model, financial structure, and competitive moat, giving a balanced institutional view of where it positions itself in the AI adtech battleground.

Source: 4Q24 AppLovin Financial Update

Algorithm in the Core: How AppLovin Monetizes Automation

AppLovin's business model has evolutionarily shifted from a platform business and hybrid app portfolio business to a vertically integrated AI ad engine. Its Axon 2.0 algorithm is central to this, directing more than $3.2 billion in advertising revenue in FY24, a 75% YoY increase. By design, Axon eliminates human frictions from the ad optimisation loop, supporting small teams in running large-scale campaigns with granular control and performance consistency. What emerges is not scale, but hyper-efficiency: Advertising segment adjusted EBITDA margins reach 76% in 2024, up from 69% a year ago.

What sets AppLovin apart from more general DSPs or programmatic competitors is its direct alignment between model optimization and performance-driven advertiser return on investment. In a world where traditional attribution is rapidly being held back by privacy rules, AppLovin avoids this tension by controlling the algorithm plus the routing infrastructure of the media. Its offerings guarantee measurable profitability per dollar, giving advertisers a deterministic loop of return unavailable from many brand-focused DSPs. This has made the platform highly sticky with performance verticals like gaming, direct-to-consumer e-commerce, and mobile-first apps.

The firm's internal culture carries through to its architecture: “Automate before hiring.” This culture of lean engineering is expressed in the way the firm's finances are structured, with R&D expenditure merely 14% of revenue while operating leverage keeps increasing. AppLovin's CapEx in FY24 was a paltry $4.8 million, signaling a low-capex business model capable of accretive free cash flow even through growth spikes.

Source: Ycharts

How to Weather the Ad Tech Bloodbath: Maintaining a Competitive Edge

The adtech universe has been unforgiving for the last three years. Amidst privacy headwinds, signal decay, and declining valuations for mobile ad networks and traditional DSPs, several peers have fought tooth and nail just to stay profitable or alive. AppLovin has prospered instead by not chasing scale through user acquisition but rather by optimizing with a ruthlessness for monetization per user. Unlike The Trade Desk's top-down emphasis on brand advertisers or Google's platform lockin, AppLovin's AI-native engine is tailored for mid-funnel conversion, making it a unique bet on scalable, post-IDFA performance advertising.

Vertical integration is one of AppLovin's most important competitive strengths. Whereas competitors like Unity, ironSource (now a part of Unity), and Digital Turbine use segmented stacks built from outside partners, AppLovin's ad system is a closed loop. Axon serves as the real-time bid, campaign, and user-scoring platform, while the business's in-house app inventory, in addition to partner integrations, keeps feedback data in its environment. This close feedback loop maximizes model training, as well as the efficiency of its campaigns, enabling AppLovin to negotiate better prices and win rates in contested auctions.

Another advantage is platform versatility. Whereas legacy ad networks often falter when expanding beyond mobile games, AppLovin has begun successfully penetrating broader verticals. In FY24, the company launched dynamic creative tools powered by AI to deliver hyper-personalized ads, a critical differentiator in a world shifting toward generative media. Moreover, its upcoming self-serve dashboard, powered by AI agents, could democratize campaign management for non-technical advertisers, expanding its TAM while reducing customer support costs.

Although its peers such as Meta and Google enjoy wider reach, AppLovin's strength in performance accuracy as well as operational efficiency is its strong niche. Its higher EBITDA margins of 58% consolidated in 2024 leave it comfortably ahead of peers such as Unity (20% range) or The Trade Desk (adjusted EBITDA margin ~40%), implying AppLovin is running one of the most efficient monetization engines in contemporary adtech.

Financial Efficiency and Strategic Flexibility FY24 was a break-out year for AppLovin not only in revenue, but also in operating discipline as well as balance sheet management. Overall revenue was up 43% YoY to $4.71 billion, with advertising driving the lion's share. The Apps segment, relatively stable, nonetheless contributed $1.5 billion in revenue and $277 million in adjusted EBITDA, providing a solid cash base while the AI engine takes the Advertising side higher

The company’s gross margin profile, with cost of revenue at just ~$1.17 billion on $4.71 billion revenue, implies a gross margin of over 75%, a sign of significant model scalability. SG&A expenses grew moderately, and R&D investments, while up slightly, remain efficiently deployed. This cost discipline helped deliver $2.7 billion in adjusted EBITDA, up 81% YoY, while free cash flow doubled to $2.07 billion.

Most importantly, AppLovin undertook a $2.1 billion share repurchase in FY24, decreasing share count substantively in a vote of confidence in intrinsic value. At the same time, the firm financed its balance sheet with new debt, issuing $4.6 billion at low rates to replace $4.2 billion in higher-cost debt. Leverage is moderate, but interest expense is no more than $318 million a year, while net income grew by a stunning 343% to $1.58 billion, suggesting a comfortable interest coverage ratio

Looking ahead, the firm guided for first quarter 2025 adjusted EBITDA of $855–$885 million on revenue of $1.355–$1.385 billion, implying sustained momentum in ad monetization. CapEx continues to be minimal, while operating cash flows are strong. With the net debt remaining under control, as well as ongoing buybacks, AppLovin is entering into 2025 with strategic responsiveness and financial strength.

Source: 4Q24 AppLovin Financial Update

Valuation: A Margin-Moated Compounder in Plain Sight

AppLovin shares trade at elevated valuation levels, reflecting strong profitability and investor optimism about sustained monetization via its Axon engine. With a forward EV/EBITDA of 20.05x (vs. sector median of 11.68x) and a forward P/E of 33.25x, the stock isn’t cheap relative to peers. It trades significantly above the sector average in nearly every valuation metric, particularly on a P/S (FWD) basis of 13.07x and a staggering P/B (TTM) of 68.45x, 2,382% above the median. However, the company’s ability to generate consistent cash flow, with a forward price-to-cash flow of 26.41x, provides a cushion to justify premium pricing. These multiples imply that the market expects sustained growth and high-margin scalability across verticals.

Importantly, APP’s valuation incorporates upside from new monetization verticals like CTV and AI tools. As AppLovin’s Axon expands into broader sectors beyond gaming, margin durability and addressable market could rise. While the high multiples raise questions about sustainability, early signs of cross-vertical adoption and AppLovin’s infrastructure-light model suggest long-term potential. If Axon’s success generalizes, a valuation re-rating toward 14–16x forward EBITDA, more aligned with high-margin platforms, could be warranted, especially if current earnings quality holds firm amid macro volatility.

Risks: Concentration of Customers and the AI Commoditization Pinch

Even with strong execution, AppLovin has a number of key risks. First, its customer base is concentrated in mobile app developers and game publishers in the US. Any decline in mobile advertising budgets or alterations in app store policies would materially affect growth. Second, further commoditization of AI advertising models, particularly with more open-source options emerging as well as self-hosted DSPs, can potentially erode Axon’s relative performance advantage in the future.

Furthermore, while debt is manageable at present, the long-term obligation of $3.5 billion exposes credit conditions. A macro slowdown, or a persistent decline in ad spend, may tighten cash flows and limit AppLovin's agility. Lastly, execution risk surrounding new projects, most notably CTV and the AI dashboard, is elevated, since these involve product-market fit in more competitive, less algorithmic environments.

Building a Scalable AI Engine with Institutional-Grade Economics AppLovin isn’t merely a story of adtech rebound, it’s a compounder powered by AI that has built a structural monetization advantage through lean execution, vertical integration, and disciplined automation.

Conclusion

Though market perception remains tied to its historical app portfolio and adtech segmentation, the driving engine of performance today is a smart, self-optimizing algorithm that translates ad dollars into high-margin cash flows with low overhead. For investors looking for exposure to real-world monetization and operational leverage from applied AI, AppLovin presents asymmetric upside, particularly as optionalities in self-serve, CTV, and generative creative continue growing in scale in 2025 and beyond.

Recommended Articles