When Light Replaces Copper: Lumentum (LITE) — The Optical Heart of the AI Era

If GPUs were the protagonists of the last AI bull market, this time the spotlight has quietly shifted to optics. The real question is no longer whether to keep buying Nvidia, but: along the entire optical interconnect chain behind NVLink and GPUs, who is the next pure-play beneficiary?

Over the past two weeks, Jensen Huang himself has pointed to an answer: Lumentum.

On March 2, Nvidia put up 4 billion dollars, investing 2 billion each in Lumentum and Coherent, and signed multi‑year large‑scale purchase agreements with priority access to capacity. This is not a simple financial investment, but effectively locking up the most critical scarce resource in AI factories — InP lasers that provide light sources for CPO and future NVLink optical interconnects — in the hands of a few suppliers. Lumentum is the purest play among them: it owns upstream InP wafer fabs, makes EML and CW/ELS lasers in the middle, and also has OCS and cloud optical modules downstream.

The timing is also unusually delicate. Next week, on one side you have Nvidia’s GTC 2026 in San Jose, where they need to clarify the next‑generation architecture, how NVLink continues to scale out, and when CPO will truly reach volume production. On the other side, you have OFC, the most important global conference in optical communications, where every vendor in optical modules, CPO, and OCS will lay their roadmaps on the table in the same week. The CPU conference of compute and the CES of optical interconnect are colliding this closely for the first time, and Lumentum stands right at the crossroads of these two main storylines: one hand holding a 2‑billion‑dollar cooperation and long‑term orders from Nvidia, the other hand controlling key links such as CPO light sources and OCS, making it one of the most representative companies along this optical interconnect chain in the eyes of many institutions. Among all the players, why is it precisely Lumentum that has ended up in the most central position on this track?

Copper’s Physical Limits: AI Data Centers Hitting an Invisible Wall

In recent years, whenever people talk about AI, the conversation starts with how many GPUs and how much compute. But there is a more easily overlooked premise: no matter how fast you compute, if data cannot move, it is all for nothing. GPUs will sit idle in the rack, power will still be burned, and capex will fail to turn into effective compute output.

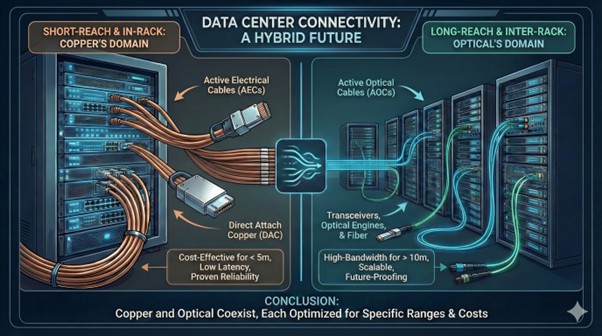

Today’s mainstream data center interconnect roughly divides labor as follows:

- Inside a rack and within a few meters for short‑reach links, DAC/AEC copper cables dominate because they are cheap and easy to deploy.

- Once you cross racks or rows, especially at aggregation and backbone layers, it is essentially an all‑optical world of fiber plus optical modules. In large new‑build data centers around 2025, more than 80% of backbone and long‑reach interconnects have already gone directly to fiber solutions.

In the tiny segment where compute density is the highest — inside the rack, between boards — most AI clusters today are still riding on copper. Precisely because of that, once bandwidth moves from 400G and 800G up to 1.6T, the first thing to break is this short stretch of copper hitting its physical limits.

1. The higher the frequency, the harder copper has to work — skin effect is unavoidable.

At 100G/200G‑class high frequencies, current no longer fills the entire copper cross‑section uniformly; it gets squeezed into a ring near the surface of the conductor, which is the classic skin effect. You pay for a thick copper wire, but the part that actually carries high‑frequency signals is only the thin layer on the surface, so the effective cross‑section keeps shrinking.

To keep running at 112G or 224G PAM4 per lane, designers can only make cables thicker, use more expensive dielectrics, and reserve more routing and bending space on the board. The consequences are cables that are stiffer, heavier, and bulkier, with rack space, airflow, and cooling pressure all rising in lockstep.

2. As soon as distance goes up, high‑speed copper gives out.

Every time you double the data rate, the reach of a traditional copper link gets slashed. At the 400G stage, a 100G/lane passive copper cable (DAC) can typically run 3–5 meters in a reasonably robust way — signal integrity and BER are still engineerable without adding chips at both ends for amplification and equalization. At 800G and 112G/lane, many vendors recommend that passive DACs should ideally stay under 2 meters; beyond that, eye diagrams collapse badly and it is hard to keep BER within acceptable engineering limits.

Pushing further to 1.6T and 224G/lane, if you do not add any chips and rely solely on a passive copper cable, in practice you can only design for around 1 meter of usable length. If you insist on going longer, you have to add small chips at both ends to amplify, equalize, and retime the signal, turning the cable into an active electrical cable (AEC), which stretches distance to around 3–7 meters, but with visibly higher cost, power, and system complexity per cable.

The real problem is that the links where AI clusters most desire high bandwidth and low latency are often exactly cross‑rack or cross‑row, where tens of meters are common. In other words, the network scale that workloads ideally want has already grown far beyond the physical comfort zone of copper at 1.6T. That is why we say AI data centers are literally running into copper’s physical ceiling.

3. Power consumption can differ by an order of magnitude.

The traditional approach can be summarized as: long copper dragging short optics. The GPU or switch ASIC first runs along a long stretch of high‑speed copper traces inside the chassis to the front panel, then hands off to pluggable optical modules — loaded with heavy‑duty DSPs, FEC, and equalization circuitry — for electrical‑to‑optical conversion. This is the typical form of most 800G/1.6T pluggable optical modules today, with 1.6T modules usually landing in the 20–25 W range, essentially burning power to brute‑force through copper channel losses.

Source: Microelectronics

CPO (Co‑Packaged Optics) flips this path around, and can also be summed up as: light runs next to compute. CPO places the optical engines right next to the switch ASIC or XPU, so high‑speed electrical signals only travel a few millimeters to centimeters on the package and substrate before converting to light, after which the rest of the path is all fiber. The long, power‑hungry high‑speed copper segment is replaced by optics. Data from vendors such as Nubis already show that under CPO/NPO architectures, putting a full 1.6T optical engine into roughly a 5–8 W envelope is realistic, saving on the order of tens of watts per port. That may not sound dramatic at a single board level, but in an AI “factory” with thousands of high‑bandwidth ports, you are talking about power differences on the order of tens or even hundreds of kilowatts.

Source: Astera Labs

So across these three dimensions, fiber almost completely dominates copper: in bandwidth density, a single fiber can stack many wavelengths as multi‑lane highways without making the physical cable thicker; in reach, tens to hundreds of meters are normal operating ranges for single‑mode fiber, with loss and ISI far friendlier than copper at similar frequencies; in power, optical signals propagating through glass do not suffer from skin effect or constant charging and discharging of large capacitances, making them inherently more energy‑efficient.

At this point, it is no longer a question of “copper vs. optics” as a pure technical debate, but rather at what speeds and at which interconnect layers the industry flips entirely to optics. From 800G to 1.6T, this migration timetable is being pushed forward step by step by AI data centers.

Three Evolution Paths of Optical Interconnect

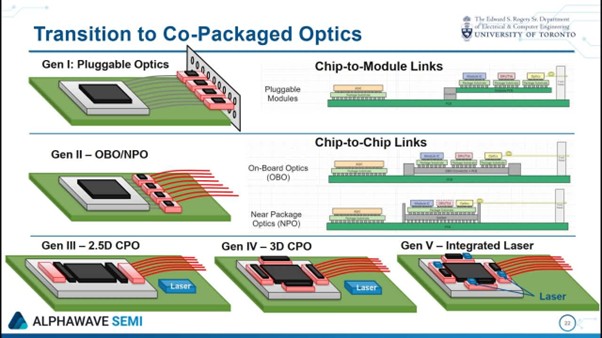

Optical interconnect is not a single solution, but a layered technology stack rolling out in stages. Broadly, it follows three paths: first deploy pluggable optics, then move optics closer to the chip, and finally change the switching architecture altogether. Once you understand these three paths, you essentially grasp who benefits and who gets squeezed over the next few years.

Pluggable Optical Modules — today’s workhorse

This is the most mature form of optical interconnect in data centers today. Modules sit on the front panels of switches for easy hot‑swap and maintenance. From 400G to 800G to 1.6T, pluggable solutions are still ramping quickly. Lumentum’s EML laser chips are the key light sources in these modules; its 100G EML shipments are at record highs, and 200G EML is ramping fast.

CPO/NPO — integrated solutions for the future

CPO integrates the optical engines directly into the switch package, fundamentally shortening the electrical‑to‑optical conversion path and sharply reducing power and latency. At GTC 2025, Nvidia first showcased Spectrum‑X and Quantum‑X switches based on silicon photonics, with 1.6 Tbps per‑port bandwidth. NPO (Near‑Packaged Optics) is a transitional form of CPO, placing optical engines a few centimeters away on the PCB, balancing power efficiency with maintainability.

According to Bernstein, large‑scale CPO/NPO shipments in scale‑out scenarios are likely to start around late 2026 to 2027, while in more reliability‑sensitive scale‑up scenarios, volume production is unlikely before the second half of 2028.

OCS — redefining the switching fabric

The first two paths focus on keeping existing Ethernet/InfiniBand logic while swapping copper for optics and moving optics to better locations. OCS (Optical Circuit Switch) is more radical: it bypasses the electronic switching layer in the middle altogether. OCS uses MEMS micromirror arrays to steer light directly between fibers, never converting to electrical signals in between, completely sidestepping the multiple O‑E‑O conversions in traditional switches. Google has been a pioneer in deploying this technology at scale in its data center networks. Lumentum’s R300 is a representative product on this path, offering 300×300 ports in a single box as an optical main distribution frame for hyperscale cloud providers.

Technology path | Power (1.6T) | Reach | Commercial stage | Representative vendors |

Pluggable optical module | 20–30 W | Tens–hundreds m | Mass production | Innolight, LITE, Coherent |

NPO | ~9 W | Tens–hundreds m | Trial production in 2026 | Nvidia, Broadcom |

CPO | 5–8 W | Tens–hundreds m | Mass production in 2026-2027 | Nvidia + TSMC + LITE |

OCS | Very low | Tens–hundreds m | Deployed by top cloud | Google, LITE |

Lumentum: Why Is This Company the Prime Beneficiary?

From spin‑off to integration: a decade of grinding the blade

Lumentum (LITE) was spun off from legacy optical player JDSU and listed independently in 2015. On paper it started as a mid‑sized optical components company, but three acquisitions over the following decade gradually rewrote its positioning:

- 2018 acquisition of Oclaro (around 1.8 billion dollars): gained a full set of InP laser design and manufacturing capabilities, the core material system for high‑speed datacom lasers.

- 2022 acquisition of NeoPhotonics: strengthened its long‑haul coherent optics portfolio.

- 2023 acquisition of Cloud Light (around 750 million dollars): entered the high‑speed cloud optical module market and began competing head‑to‑head with major Asian module makers.

By 2026, ten years on, Lumentum has evolved from a laser chip and component supplier into a vertically integrated platform covering laser chips, optical modules, and optical switching systems.

An IDM in Photonics: Why This Matters

In semiconductors, IDM (Integrated Device Manufacturer) means end‑to‑end control from design to manufacturing. Lumentum’s role in photonics closely mirrors this model:

Its own InP fabs: it runs InP photonic wafer and laser production lines in places including Sagamihara and Takao in Japan and Caswell in the UK. In a world of tight InP supply, such captive capacity is extremely scarce.

Full‑chain coverage: from making laser chips on InP wafers, to assembling optical modules in the Navanakorn industrial area near Bangkok, Thailand, to delivering OCS systems, it has footprints across the front, middle, and back ends of the value chain.

Continuous capacity expansion: a more than 40% InP capacity expansion plan launched in late 2024 is already over halfway complete, and the company is considering new fabs or M&A to further boost output.

In a supply‑constrained cycle, this kind of vertical integration becomes more valuable: while others queue for chips, Lumentum can build its own.

Four product lines, four growth engines

Engine 1: EML laser chips

EML (electro‑absorption modulated lasers) are the core light sources in 800G and 1.6T modules. Lumentum’s 100G EMLs keep setting shipment records, and 200G EMLs already contribute around 10% of datacom laser revenue in the quarter ending December 2025, with management expecting that share to reach 25% by the end of 2026. 200G devices command higher prices than 100G, lifting both ASP and gross margin. The company has also showcased 448 Gbps next‑gen EML tech to pre‑position for 400G‑per‑lane 3.2T modules.

Engine 2: CW lasers and ELS modules — the heart of CPO

In CPO architectures, modulation moves onto silicon photonics PICs, so modules no longer need their own integrated lasers; instead, they rely on external continuous‑wave (CW) lasers as light sources. These CW lasers must deliver hundreds of milliwatts of stable optical power in high‑temperature environments, demanding very high InP device and packaging prowess — exactly where Lumentum has been selected by major customers like Nvidia.

In its latest earnings call, management disclosed multiple hundreds of millions of dollars orders for ultra‑high‑power lasers, with deliveries planned to begin in the first half of 2027. More importantly, the company is extending from supplying bare laser chips to providing full ELS (external laser source) modules, whose revenue per unit is roughly 2 to 2.5 times that of a single chip, significantly expanding its addressable market.

Engine 3: OCS optical circuit switching systems

Lumentum’s R300 OCS, based on 3D‑MEMS micromirrors, now has more than 400 million dollars in backlog from three major hyperscale cloud customers. In its Q2 FY26 earnings, management noted that OCS shipment pace has exceeded internal expectations, with quarterly revenue already surpassing the 10‑million‑dollar mark earlier than planned. Most of the backlog is expected to ship in the second half of 2026.

Mizuho estimates that by 2029, the data center OCS TAM will be around 1.9 billion dollars (roughly a 44% CAGR), and Lumentum could capture 30–40% market share.

Engine 4: Cloud optical modules

The high‑speed transceiver business acquired via Cloud Light is now expanding rapidly. In Q2 FY26, systems revenue reached 221.8 million dollars (up 60% year‑on‑year), with cloud optical modules as the largest growth driver. Management emphasizes that 1.6T modules carry significantly better margins than 800G products, so as 1.6T ramps, profitability in this segment should continue to improve.

Financial Inflection Point: Let the Numbers Speak

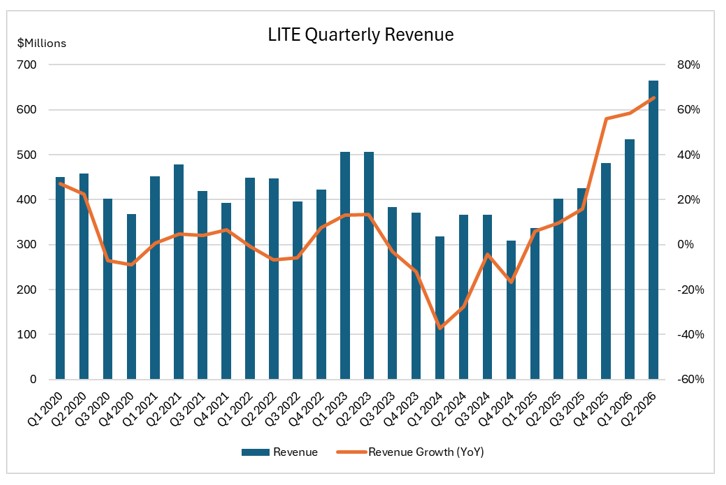

From the hard numbers, Lumentum’s inflection point is already visible to the naked eye. In Q2 FY26, the company delivered 665.5 million dollars in revenue, up 65.5% year‑on‑year and nearly 25% quarter‑on‑quarter, marking the highest quarterly revenue since listing.

Source: LITE Quarterly Reports, TradingKey

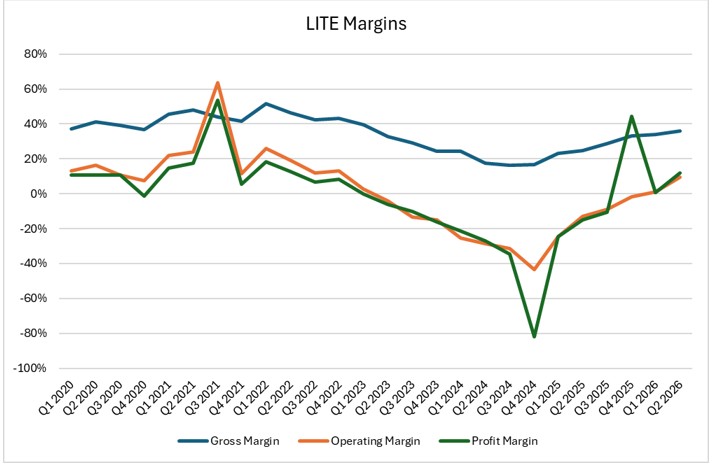

Gross margin rose from around 25% a year earlier to 36%, operating margin improved from roughly −12.8% to +9.7%, and GAAP EPS swung from −0.88 dollars in Q2 FY25 to +0.89 dollars in Q2 FY26. This set of changes shows that while revenue is growing fast, profitability is not being diluted; instead, the company is stepping up from losses to sustainable profitability.

Source: LITE Quarterly Reports, TradingKey

From the second half of FY25 through FY26, the slope clearly steepens: revenue accelerates, margins climb in steps — a classic volume‑plus‑pricing inflection rather than a one‑off rebound.

More importantly, the improvement is not just a one‑quarter story. For Q3 FY26, management is guiding to 780–830 million dollars in revenue, almost doubling year‑on‑year.

Risks & Debates

Valuation is not cheap

Based on consensus FY2027 EPS of about 11 dollars, the current share price around 670 dollars implies roughly 60× forward P/E. Some more optimistic institutions project 17–24 dollars of EPS in FY2027, under which valuation would compress to around 30×. Either way, today’s price already bakes in strong growth expectations. The core debate is whether Lumentum is still a cyclical optical component company, or has truly stepped onto a structural AI optical‑interconnect platform track.

Technology path uncertainties

There is uncertainty between CPO pilot runs and true large‑scale deployment. CPO in scale‑up scenarios still needs longer‑term reliability validation in real environments. Alternative options such as co‑packaged copper (CPC) are also vying for short‑reach interconnect needs in scale‑up use cases.

Customer concentration

OCS orders currently come mainly from three hyperscale customers. If OCS fails to expand beyond these leading cloud players into a broader market, the growth ceiling could fall short of expectations.

Rising competition

In lasers, Coherent is upgrading its InP lines from 4‑inch to 6‑inch wafers, potentially quadrupling per‑wafer output. In optical modules, Chinese vendors (such as Innolight and others) are moving upstream into laser chips. Whether Lumentum can maintain its current technology and capacity edge will depend on sustaining its R&D pace.

Conclusion

Lumentum’s growth logic can be boiled down to a clear causal chain: AI clusters keep scaling up → GPU‑to‑GPU bandwidth demand grows exponentially → copper hits its physical limits → optical interconnect becomes the only way out → lasers sit at the very start of the optical chain → the number of companies capable of making high‑end AI‑grade lasers is tiny → through IDM‑style integration and a decade of M&A, Lumentum has built the broadest footprint in this choke‑point position.

It is simultaneously riding three growth curves: the ramp of 800G/1.6T pluggable modules, the commercialization of CPO/NPO from zero to one, and the spread of OCS across multiple hyperscale clouds. Having these three curves rise together in 2026–2027 is extremely rare in the history of optical communications.

Of course, at 670 dollars, the stock already embeds very high expectations. The key proof points are just ahead: next week’s GTC and OFC will deliver critical signals on CPO’s ramp schedule, OCS customer diversification, and the role of optical interconnect in Nvidia’s next‑generation architectures.

Disclaimer: This article is for industry analysis and information sharing only and does not constitute any investment advice or recommendation. Investing involves risks. Any investment decision should be based on your own independent judgment and consultation with professional advisors.

Recommended Articles