JPMorgan’s Q3 Rally Fizzles as Dimon Warns of “Cockroaches” Ahead

TradingKey - JPMorgan Chase, the largest U.S. bank, reported its Q3 2025 earnings on October 14, delivering record-breaking revenue and profit that surpassed analyst expectations — the strongest quarter in its history.

Yet, despite the stellar results, JPMorgan’s stock fell as much as 4% intraday, closing down 1.91%. The disconnect between performance and price reflects a market already priced for perfection, rising valuation concerns, and CEO Jamie Dimon’s stark warning about hidden credit risks — his now-infamous “cockroach talk.”

J.P. Morgan Chase reported third-quarter revenue of $47.12 billion, surpassing expectations of $45.48 billion, with net income reaching $14.4 billion compared to an estimated $13.7 billion. The Wall Street giant not only achieved a record high in trading revenue during the quarter but also posted double-digit percentage growth in investment banking. With an 8.7% share of global investment banking fees, the firm maintained its lead over peers.

Yet, investors responded with caution — not celebration. Shares of J.P. Morgan closed down 1.91% on Tuesday. Year to date, the stock has gained about 26%, outperforming the S&P 500’s 13% rise over the same period.

High Expectations Already Priced In

Despite beating forecasts, the reaction underscores a classic “sell the news” dynamic. Bullish sentiment was fueled by Fed rate cuts, AI-driven trading volumes and the Trump administration’s deregulatory stance.

Keith Horowitz, Citi analyst, said that this was a solid quarter — but the stock already reflected that strength.

Glenn Schorr, Evercore ISI analyst, added that big banks delivered, but it was fully expected. Much of the good news is already baked into valuations — and those valuations are high.

Rich Valuation Raises Red Flags

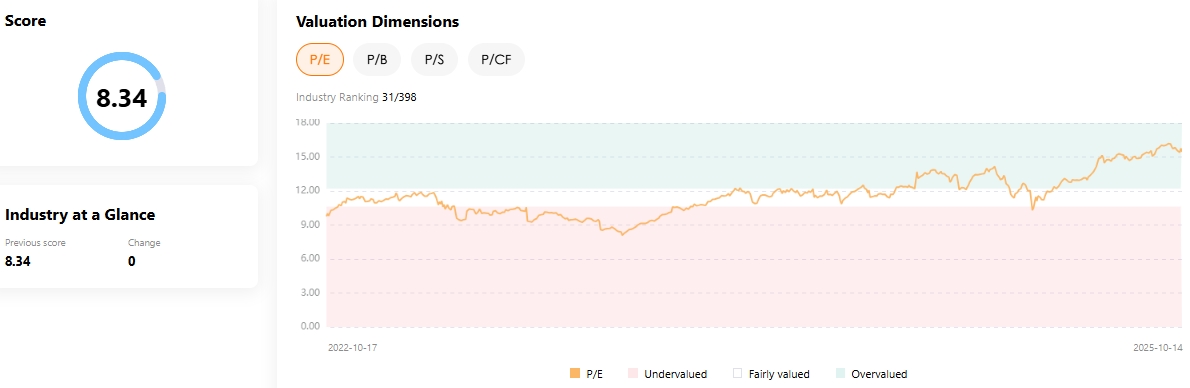

After months of gains since April, JPMorgan’s valuation has stretched. According to TradingKey’s stock score tool, JPMorgan trades at a P/E ratio above 15x — near historical highs.

JPMorgan Stock Valuation Level, Source: TradingKey

Morningstar analysts plan to modestly raise their fair value estimate for JPMorgan (currently $235 per share) due to strong profitability. But they stress that even after adjustments, the stock remains overvalued relative to risk.

They note:

“The bank has an enviable competitive position and should continue to grow its market share. Having said this, we remind investors that banking is a cyclical business and profitability is currently near cyclical highs.”

Dimon’s “Cockroach Talk”: A Warning Sign

While declaring that “all businesses performed well,” CEO Jamie Dimon also issued a sobering outlook on future risks, citing:

- Complex geopolitical tensions

- Trade and tariff uncertainty

- Asset price inflation

- Sticky inflation risks

When asked about the September bankruptcy of subprime auto lender Tricolor, which cost JPMorgan $170 million in losses this quarter, Dimon said that this was not "our finest moment".

He added that the firm is reviewing all risk and control frameworks. But his most quoted remark came next:

“When you see one cockroach, there are probably more.”

Dimon warned that Tricolor’s collapse — followed by the bankruptcy of auto parts supplier First Brands Group — is unlikely to be isolated.

Recommended Articles