Institutional rush for Bitcoin CME futures cools as premium drops

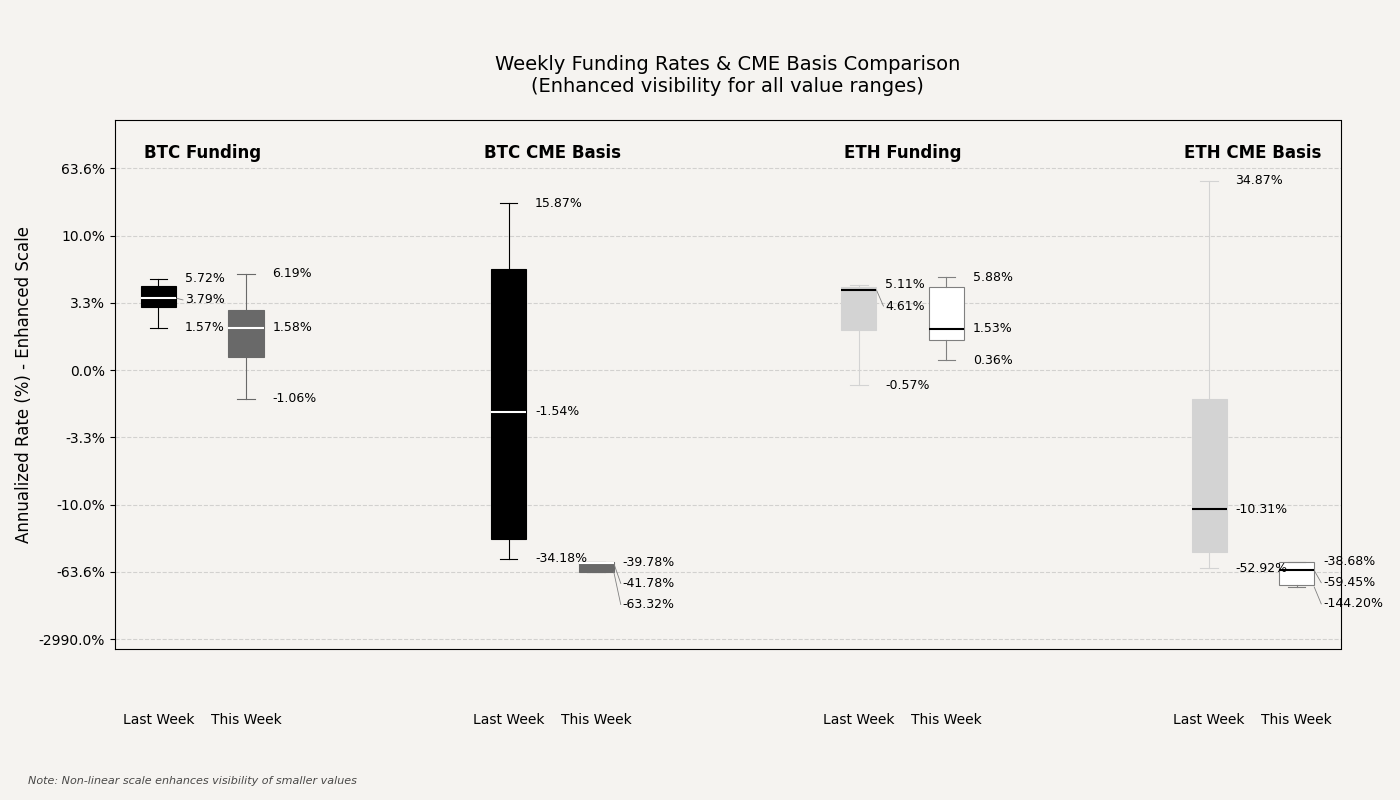

The premium on Bitcoin futures listed on the Chicago Mercantile Exchange (CME) has declined to its lowest level in eight months. According to data from 10x Research, the rolling three-month basis on CME Bitcoin futures has fallen to just 4.3%, a level not seen since October 2023.

The figure recorded is a downturn from levels above 10% seen earlier in 2025, and could mean institutional interest in the largest crypto by market cap is dwindling, heading into the third quarter of 2025.

At the time of this report, Bitcoin is changing hands at around $107,700, an uptick of about 1% over the last 24 hours. Over the past two weeks, the coin has been consolidating in a tight range between $105,000 and $107,700.

The decline in futures premiums spells a loss of forward-looking enthusiasm among professional investors. The drop in what is known as the “basis,” the difference between futures and spot prices, translates to a reduction in arbitrage opportunities and an undefined near-term price direction.

Institutional retreat from arbitrage market positions

According to CME data from Q2, public companies increased their Bitcoin holdings by 131,000 BTC, a surge of 18%, while ETF inflows rose by approximately 8%, an additional 111,000 BTC. These figures indicate that institutional interest in Bitcoin was initially present, at least in aggregate.

However, 10x Research founder Markus Thielen said the drop in yield spreads shows how institutions are less confident about a Bitcoin price move on the upper side.

“When yield spreads fall below a 10% hurdle rate, Bitcoin ETF inflows are typically driven by directional investors rather than arbitrage-focused hedge funds,” he explained. CME basis rates now lie around 4.3% and perpetual funding rates around 1.0%, which means the environment is becoming less favorable for cash-and-carry strategists.

In most cash-and-carry trades, hedge funds exploit price discrepancies between spot and futures markets by simultaneously buying Bitcoin via ETFs and selling futures to lock in a yield. That opportunity is drying up. Not many funds are now willing to deploy capital for the slim return, owing to the sentiment of a “risky environment.”

Funding rates negative, retail momentum stalls

The softening in CME premiums comes against the backdrop of negative funding rates in perpetual futures in offshore exchanges. These rates recently flipped below zero, implying that traders are paying for short positions, another indication of bearish bias in derivatives markets.

Padalan Capital, in a weekly market update, coined the funding slide “a symptom of broader speculative fatigue.”

“A more acute signal of risk-off positioning comes from regulated venues, where the CME-to-spot basis for both Bitcoin and Ethereum has inverted into deeply negative territory,” the firm remarked. Institutions are more than likely seeking safety ahead of the second half of the year, as most CME gaps were filled before Bitcoin’s breakout to new all-time highs late May.

Bitcoin whales’ sentiment is mixed

Per Blockchain intelligence firm CryptoQuant contributor Kripto Mevsimi, on-chain behavior during the final week of June showed Bitcoin whales realized over $641 million in profits and more than $1.24 billion in losses within the same week.

Some investors who entered late in the rally appeared to capitulate, while earlier Q2 buyers likely used the moment to lock in gains. Long-term whales also took profits of approximately $91 million and recorded relatively few losses.

These simultaneous signals of profit-taking and capitulation could represent a local exhaustion point. However, activity levels have since dropped heading into July, the start of a balance period, or a purported change in market behavior in support of bears.

Cryptopolitan Academy: Want to grow your money in 2025? Learn how to do it with DeFi in our upcoming webclass. Save Your Spot

Recommended Articles