Micron Share Price Rises Over 9% to Return to $100. New $50 Billion Domestic Expansion Plan Added as Several Tech Company Executives Increase Holdings of Core US Tech Assets During Correction.

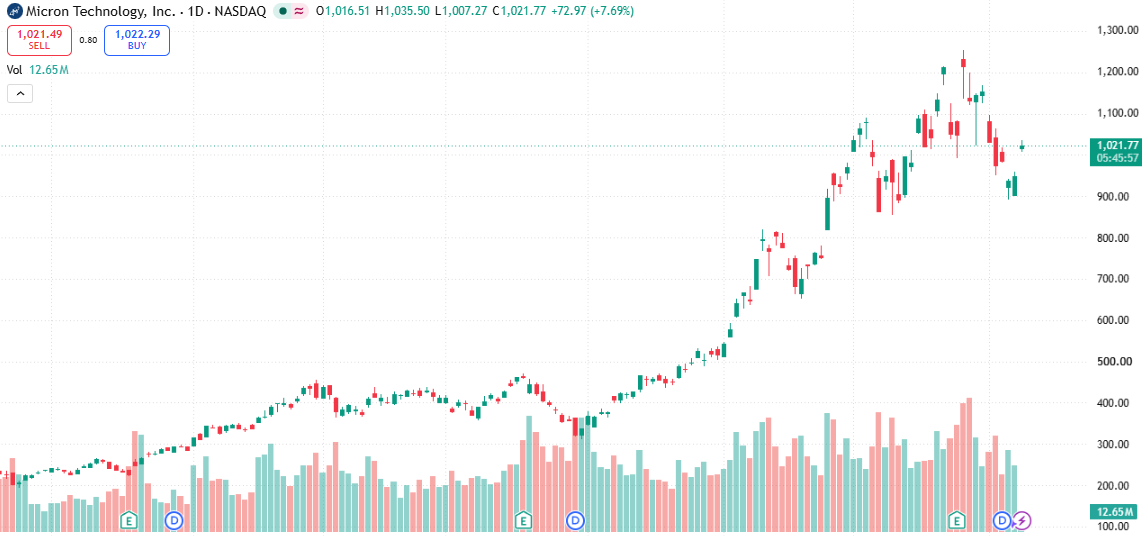

Tradingkey - On July 9, Eastern Time, Micron Technology ( MU) shares reclaimed the $1,000 level, rising 7.69% to $1,021 at the time of writing. Since hitting an all-time high of $1,254.8 on June 25, Micron's stock has pulled back by more than 10%. The early session surge in share price today was catalyzed by multiple favorable factors.

[Source: TradingView]

Micron announced today that it is boosting its previously disclosed US domestic expansion plan to $250 billion, an increase of $50 billion from its original commitment. This move underscores the explosive growth in demand for memory chips driven by the AI infrastructure boom. The projects cover multiple plant construction plans in New York, Idaho, and Virginia, with overall capital expenditures expected to extend through 2035.

In addition, Micron stated it will set aside another $3 billion to strengthen the domestic semiconductor supply chain. This includes providing $500 million in strategic financing to Taiwan-based silicon wafer supplier GlobalWafers Co., with both parties signing a ten-year raw materials supply agreement.

Aside from the company's own corporate actions, Bank of America also offered a positive interpretation of the recent correction in semiconductor stocks. The bank reiterated its "Buy" rating on Micron, viewing the company as still the most attractive investment target in the memory industry.

The firm noted that semiconductor stocks frequently undergo consolidation during the summer, but once the market completes profit-taking and valuation corrections, a new wave of rallies often emerges in the autumn. Bank of America expects global cloud computing and AI infrastructure capital expenditures to approach $1.5 trillion by 2027, representing a growth of approximately 40% to 50% from current levels. In terms of memory chips, the bank believes that as demand for HBM, DDR5, and enterprise storage continues to expand, and AI servers keep driving demand for DRAM and NAND Flash, the memory industry will remain a key beneficiary of the AI investment wave, leaving clear room for valuation recovery.

Renowned investment bank Evercore ISI shared the same view, describing the recent correction as "healthy." The firm further pointed out that even US Treasury yields have shown unusual fluctuations, explaining that in a typical risk-off environment, yields would drop much further, but AI-driven inflation concerns are tempering this reaction. Considering the recent gains in chip stocks, a 20% to 30% correction is actually healthy in the long run.

Meanwhile, data compiled by Sentiment Trader revealed that secondary market buying by insiders—such as directors, executives, and major shareholders of US tech companies—has surged to its highest level since tracking began in 2010. Against a backdrop of market concerns over high AI sector valuations and macroeconomic headwinds, this collective move by industry capital highlights strong confidence in the sector's medium-to-long-term fundamentals. Data shows that the current tech insider buying sentiment index reached a reading of 28, significantly exceeding any previous cyclical peaks over the past fifteen years.

Market analysts noted that insider buying serves as a highly valuable indicator, as executives rely on first-hand operational data to determine that current stock prices offer attractive entry points, remaining unaffected by short-term market volatility.

Recommended Articles