Micron Stock Price Drops 10%—Why the AI Memory Bull Case Still Looks Intact

TradingKey - Micron (MU) shares are trading around $1,032 to $1,037, roughly 10.6% below Tuesday's close of $1,154.29, after reaching an all-time intraday high of $1,255.00 on June 25. Even after the recent pullback, the stock remains up an extraordinary 305% year-to-date through Tuesday and more than 855% over the past twelve months. Investors who bought in at the top have seen a sharp drop in just a couple of sessions, and those who were waiting for a better entry have now found it. Importantly, this isn't a Micron-only selloff. It's been a general reset across the memory market, and that's why the focus should be on the business, not the recent price action.

Fiscal Q3 Results Blew Past Estimates

The stock's strong rally continues to be driven by Micron's fiscal third-quarter earnings, which were released on June 24. Revenue jumped 346% year-over-year to $41.46 billion, well above the consensus estimate of $35.91 billion. Non-GAAP earnings per share of $25.11 far surpassed the $20.28 estimate.

Management also provided positive guidance for fiscal Q4, forecasting revenue of $50 billion and $31 EPS at the midpoint. The forecast does not mean the growth is slowing down, rather it indicates that the momentum may carry on. For investors, that's the prominent number to keep an eye on. If Micron doesn't live up to those expectations, it would mark the first serious dent in the greater memory supercycle story.

CEO Mehrotra Defends the Pricing Strategy

On the earnings call, CEO Sanjay Mehrotra said that years of aggressive customer pricing had led to underinvestment in memory, while AI demand had been picking up. He says that imbalance has created a structural supply shortage that may extend into 2027 or later.

That is a critical point for any investor that is wondering if the price is merely another bubble? Micron feels this is an environment of real supply/demand imbalance and the company has been able to establish a pricing position rather than surrender it to customers. The company also reiterated its plan to spend about $200 billion on manufacturing capacity and research and development, including new fabrication plants in Boise, Idaho and Syracuse, New York.

The GM Supply Deal Locks In Multi-Year Demand

On July 1, Micron announced a Strategic Customer Agreement with General Motors to supply LPDRAM, NOR, and UFS NAND memory products to GM's next generation vehicles.

The agreement is one of 16 long-term customer arrangements that were emphasized on the earnings call and backed by a $2 billion modernization of Micron's Manassas, Virginia fabrication plant. The multi-year supply agreements are particularly significant because they secure future demand and mitigate potential order growth risk, especially as the spending on AI technologies potentially calms in the future.

A DRAM Price-Fixing Lawsuit Adds Legal Overhang

The company, along with Samsung and SK Hynix, is also being sued in a new class-action lawsuit for colluding to set DRAM prices.

These allegations are not legal verdicts at this stage, but it gives yet another layer of uncertainty to an already high valuation stock. The lawsuit is headline risk that investors should keep an eye on, but not to give up on the investment thesis. Prices for memory chips have continued to rise despite legal news, implying that supply and demand remain the most important factors.

Trump Accounts Commitment Keeps Micron in the Spotlight

Micron also gave $250 million to Trump Accounts, a federally-backed children's savings plan. President Donald Trump endorsed the announcement on Truth Social, calling Micron "one of the hottest anywhere in the world.

The pledge doesn't affect Micron's fundamentals, but it does ensure that the company remains a constant topic of political and retail-investor discussion as sentiment continues to be extremely sensitive to headline risk.

Valuation and Insider Selling Are Worth Watching

Some valuation models show that Micron's shares are undervalued compared to discounted cash flow valuations given the company's well-behaved operating results. At the same time, insider selling has exceeded insider buying over the past three months, including share sales by CEO Sanjay Mehrotra.

These moves don't necessarily undermine Micron's growth narrative, but they do make a case for prudent position sizing following what's been an exceptional run. The recent 10% drop is a reminder that even companies that are fundamentally strong can be very volatile.

Analyst Targets and What to Watch Next

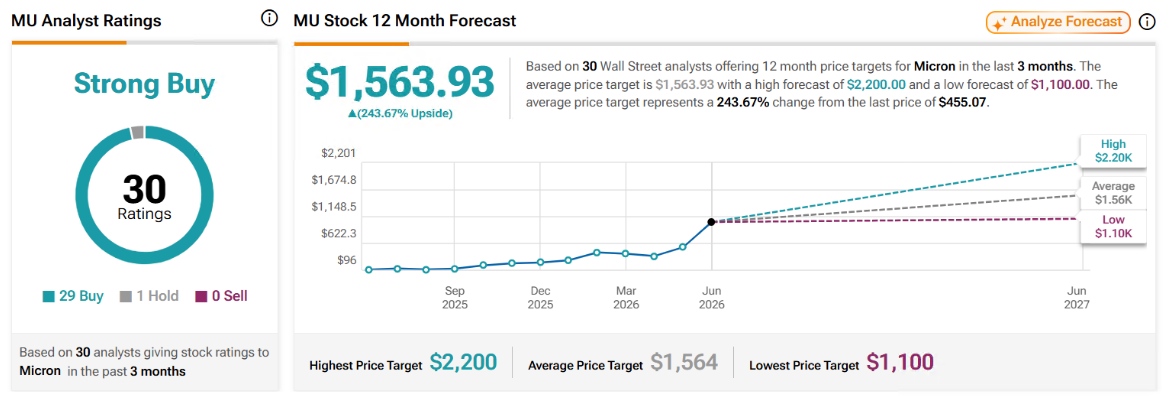

Despite the recent sell-off, Wall Street is being broadly bullish. Mizuho has recently increased its price target to $1,375, while the average analyst consensus is in a $1,564, with most analysts issuing Strong Buy ratings.

Image Source: TipRanks

Those targets suggest a meaningful upside from current levels if Micron can execute on its guidance for the Q4 and keep signing long-term supply deals such as the GM contract. The $1021 to $1037 range is an important support level for bulls to get ready for in the near term. If price breaks below $1,000, there may be further correction to come, but if price returns to above $1,150, buyers are clearly stepping back into the stock.

September will serve as the next big catalyst, but investors will also be watching to see if memory prices continue to improve across the summer and if the DRAM lawsuit evolves into a more serious legal wrinkle. Micron's $0.15 dividend, with an ex-dividend date of July 6, provides a modest additional benefit, though it is unlikely to be the primary reason investors buy the stock.

Recommended Articles