Marvell Technology Has Soared 247% in 2026. Here's How Much Upside It Can Deliver Over the Next 3 Years

Key Points

Marvell Technology serves two key AI infrastructure niches, which explains why its growth rate is poised to pick up.

The stock is expensive right now, but it can justify its valuation by delivering stronger-than-expected growth.

Marvell investors can still expect further upside from the stock, even after its red-hot rally this year.

- 10 stocks we like better than Marvell Technology ›

Marvell Technology (NASDAQ: MRVL) stock has jumped by a stunning 247% so far this year. Investors have been buying shares of this chip designer hand over fist since it became evident that it is poised to capitalize on the fast-growing demand for application-specific integrated circuits (ASICs) and networking equipment in artificial intelligence (AI) data centers.

What's more, Nvidia CEO Jensen Huang's recent statement about Marvell becoming the "next trillion-dollar company" seems to have further boosted investor confidence in this semiconductor stock. However, we are going to look beyond the hype in this article to see whether this high-flying chipmaker can deliver further gains following its phenomenal rally and make investors richer over the next three years.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: The Motley Fool.

Marvell Technology has become extremely expensive, but that's half the story

Marvell's parabolic jump this year explains why its 12-month median price target of $240 sits 23% below its current stock price. After all, Marvell has a trailing price-to-earnings multiple of 106. Also, the forward earnings multiple of 76 isn't cheap either, though it does suggest a nice spike in the company's bottom line.

For comparison, the tech-laden Nasdaq Composite index has an average earnings multiple of 41. So, Marvell will have to consistently deliver stronger-than-expected results and guidance in order to deliver more gains. The good part is that the company can indeed do so. It is worth noting that 85% of the 47 analysts covering Marvell stock still rate it as a buy.

That's because the company is confident it can substantially accelerate growth thanks to the lucrative markets it serves. Bloomberg estimates that the custom AI processor market could grow to $118 billion in 2033, accounting for 19% of overall AI chip sales. However, don't be surprised to see custom chips cornering a bigger share of the AI accelerator market as they are being deployed aggressively by hyperscalers and AI companies to lower operating costs.

On the other hand, Marvell also sells optical connectivity solutions, an area that's becoming the next bottleneck in AI infrastructure. Goldman Sachs expects the optical networking market to grow by a whopping 9x to $154 billion. What's more, the investment firm counts Marvell as a key player in this space, along with Nvidia and Broadcom.

All this explains why Marvell is forecasting its annualized revenue from datacenter interconnect (DCI) optical products to double between fiscal 2026 and 2028 to $1 billion. On the other hand, the annualized revenue of its switching products is expected to jump to $600 million in the current fiscal year, and then to more than $1 billion in the next one.

The custom AI processor business, meanwhile, is poised for some serious acceleration. Marvell expects 20% growth in this segment in the ongoing fiscal 2027. The beginning of new customer programs and more business from existing customers will drive an increase of more than 100% in Marvell's custom silicon revenue next year.

Why Marvell investors can expect more upside over the next three years

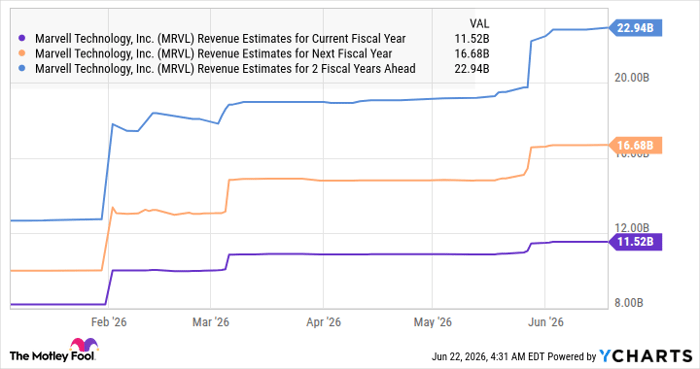

Marvell expects 40% revenue growth in the ongoing fiscal year 2027 (which ends in January next year) to $11.5 billion. The growth rate is poised to accelerate next year, then slow slightly after two years.

Data by YCharts

However, Marvell's growth rate could easily outpace Wall Street's expectations in fiscal 2029 and accelerate further, especially given that large data center investments are unlikely to slow. Let's assume it can clock 50% revenue growth in fiscal 2029, Marvell's revenue will jump to $25 billion. If the stock trades at even 15 times sales at that time (nearly half its current sales multiple of 31), its market cap could reach $375 billion.

That suggests potential upside of 38% over the next three years. However, the massive growth potential in the optical networking space and the steady growth of the custom AI processor market could allow Marvell to clock stronger growth. As a result, Marvell could end up trading at a much higher sales multiple after three years than what I have assumed above, and that's going to pave the way for stronger upside in this AI stock.

Should you buy stock in Marvell Technology right now?

Before you buy stock in Marvell Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Marvell Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $417,305!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,293,148!*

Now, it’s worth noting Stock Advisor’s total average return is 936% — a market-crushing outperformance compared to 209% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 22, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Broadcom, Goldman Sachs Group, Marvell Technology, and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles