TSMC 1Q Preview: How much Upside is There?

We already know the revenue figures for TSMC in Q1, as they report the revenue monthly. The revenue is NT$1.13tn or $35.7bn. This is almost at the top end of the guidance the management gave at the beginning of the year (between US$34.6 billion and US$35.8 billion).

Month | Revenue (NTD) | Approx. Revenue (USD) | Growth (YoY) |

January | NT$401,255M | ~$12,650M | +36.8% |

February | NT$317,657M | ~$10,010M | +22.2% |

March | NT$415,191M | ~$13,050M | +45.2% |

Total Q1 | NT$1,134,103M | ~$35,710M | +35.1% |

Some people may ask, what should we pay attention to at TSMC’s earnings, considering we know the revenue number, and what is the upside for the stock price?

Revenue Growth Well Supported by Demand

Let’s start by discussing the revenue. 35% year-over-year top-line growth is undoubtedly a very strong number, and, in fact, there is a rather good visibility (20%-30% CAGR) when it comes to the revenue in the next 2-3 years, driven by a few tailwinds.

Firstly, we have the sustained demand for 3nm chips driven by growth in agentic AI workloads (Claude Code, OpenClaw) and even stronger demand from ASICs and CPUs, in addition to the strong GPU market. Currently, the shipments of ASICs are half that of the GPUs, but we expected ASICs to grow at a much faster rate and reach parity with GPU production by the end of the decade.

Moving further down the nodes, 2nm is ramping up, and it is expected to contribute a more significant portion of the revenue in 2026 and 2027.

Source: JP Morgan

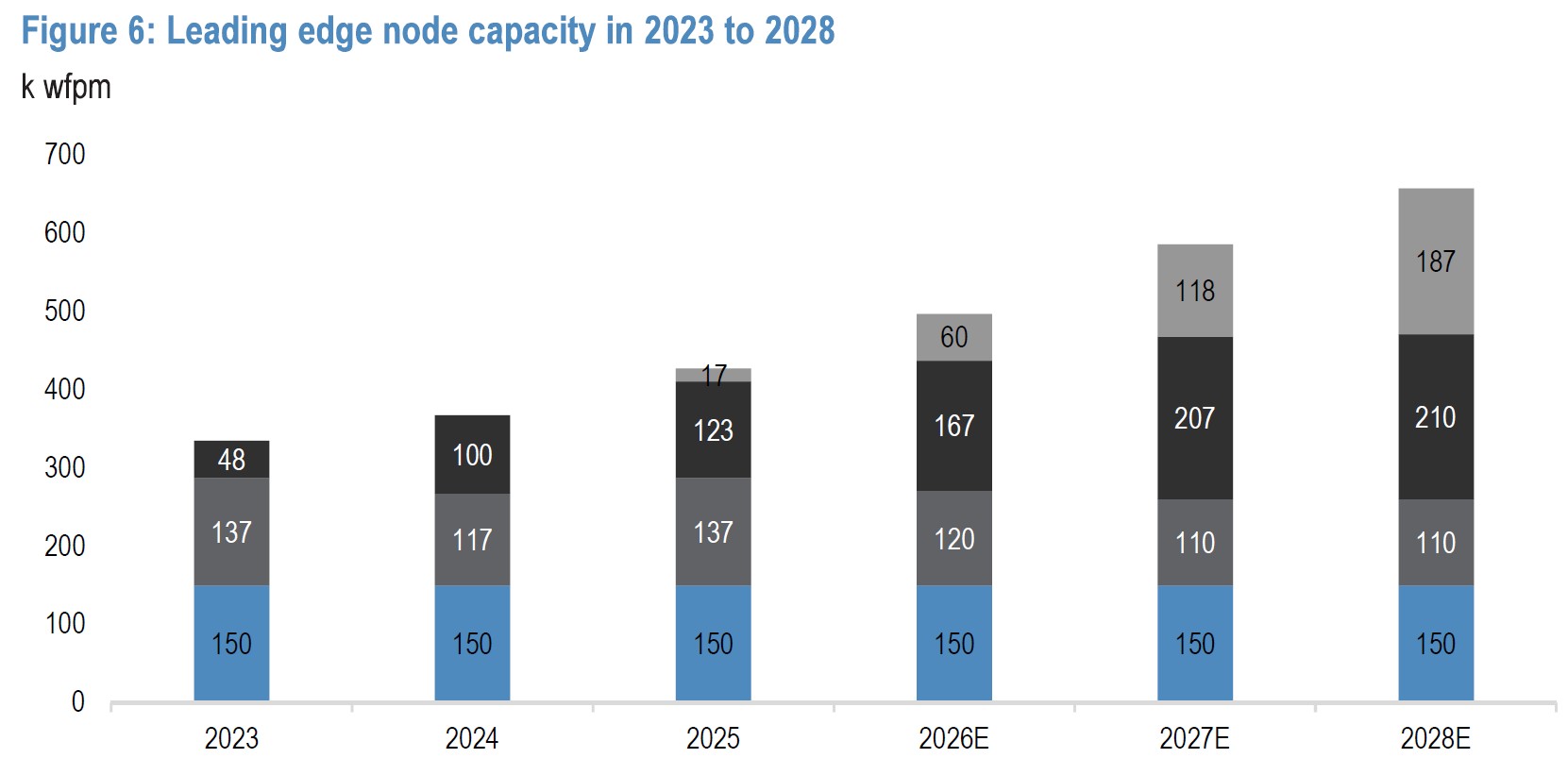

Both 3nm and 2nm face strong demand and restricted supply:

- TSMC is expected to reach 200k wafers per month (wfpm) of 3nm capacity by the end of this year, but the total market demand is estimated at around 240k-250k wfpm, leaving a 40-50k unmet demand

- For 2nm, the gap is even more severe as TSMC capacity would be roughly 60k wfpm, but it can stretch to 80k, while demand is estimated at around 140k wfpm

This kind of distorted supply-demand picture creates an environment where TSMC, as a market leader, can dictate higher prices, and we are not talking about higher pricing from switching from higher to lower nodes, but also higher pricing for a like-to-like basis – same chips cost more this year vs last year.

Beyond the nodes, CoWoS packaging is the emerging star in the already-strong product line of TSMC. It is still a rather small portion of the revenue (less than 10%) but expected to grow faster, as giants like Nvidia, Intel and AMD recognise how important the integration of GPUs with HBM into a unified architecture.

Even in the phone segment, the legacy business representing nearly a third of the TSMC total revenue, we see a moderate upside as Apple is expanding towards lower-priced market segments, which might be capped due to weakness in Android smartphones and PCs due to memory price hikes and suppressed consumer sentiment, and even potential delays in iPhone releases.

Competitive Risks for TSMC

If the demand is here to support the top-line growth, we need to ask if there is anyone who can steal this demand from TSMC.

As of now, in terms of market share, TSMC is absolutely dominating anything at 5nm or lower, but there is no lack of competition, as Intel and Samsung are not idle.

For Intel, 18A is the main hope to compete with TSMC’s 2nm; 18A yield is showing improvements at 65-75%, which is much closer to TSMC's compared with a year ago. We can also see this reflected in the stock performance as INTC is among the major outperformers this year. However, it is too early to believe TSMC is under threat, as TSMC’s projected capex is $52-$56 billion in 2026, while Intel's is expected to be $17-$18 billion for the same period, a spending gap providing a strong safety net. Also, Intel plans to rely on less-proven high-NA EUV compared to TSMC’s low-NA EUV approach, which may cause more setbacks for INTC and hence extra capex.

On the other side, we have Samsung. Like Intel, they also struggled with low yield, but they are now ramping up. Samsung’s 2nm GAA yields were reportedly stuck at 20% in late 2025 but have climbed to approximately 55%–60% as of Q1 2026.

Samsung is the only company on Earth that produces the HBM4 memory, Logic, and advanced packaging under one roof. This reduces the "interconnect penalty”, lowering latency and power consumption by roughly 20% compared to the SK Hynix + TSMC "Allied" approach. However, this major advantage is also their biggest disadvantage – clients like NVDA and APPL may not be so willing to entrust their next-generation blueprints with a company that competes with them. Also, Samsung's capex budget for 2026 is massive - $73 billion, but that is for both logic and memory.

Helium – the Unexpected Headwind

The current geopolitical picture may affect TSMC supply negatively, especially in the case of Helium. Lithography machines need a constant flow of helium to cool the machines and remove oxygen. Without helium to manage temperature, chips can develop microscopic cracks during the etching process. Helium flushes out toxic chemicals. If this isn't perfect, "junk" atoms get trapped inside the chip, making it fail testing immediately.

30-40% of the global helium comes from Qatar, and some sources mentioned 40% increase in helium spot prices

Good news for TSMC is that Helium still presents a relatively small part of the cost structure. Direct materials (wafers, chemicals, gases, and photoresists) typically make up 15%-20% of the TSMC COGS, and within that portion, speciality gases like neon, helium and argon account for roughly 1-2%.

However, apart from cost impact, it is the lack of availability of helium that can hurt TSMC – without enough Helium, the whole production process may be put on hold. So, in case of a cut supply, who gets helium priority?

TSMC has a very high priority for gaining access to Helium, but not the highest priority (healthcare and defense industries usually have a higher priority). However, TSMC can recycle helium – aka they can re-use it – TSMC has 80-95% recovery rates.

Why is the recovery rate that high? Answer: There was a shortage of helium in 2022, and after that, TSM invested a lot in helium recovery tools, unlike other competitors

Also, for logic chips, helium is used in a relatively clean way (cooling and purging) without much mixing with chemicals, in contrast with memory chips (DRAM and NAND), where there are more chemicals mixed with helium, hence it is hard to purify it back for usage.

So overall, this risk for TSMC is rather under control.

Company | Est. Recovery Rate | Main Vulnerability |

TSMC | 80% – 95% | Minor spot-market exposure (~30% Middle East). |

Intel | ~60% – 70% | Higher reliance on fresh U.S. domestic supply (which is stable but finite). |

Samsung | ~40% – 50% | High exposure to Qatar (65%+) and more complex "dirty" memory exhaust streams. |

Profitability is the Big Question

Margin is where the uncertainty for TSMC lies, as there are many factors playing a role here. In FY2025, the gross margin was nearly 60%, and in Q4, that number was 62%, which is a record high for TSMC, considering the margins were in the range of 40%-55% in the past 15 years. This naturally raises the question of whether this level of margin is sustainable.

According to the guidance from the firm, the GPM is expected to be even higher, towards 63% and 65%, supported by FX tailwinds. Since TSMC sells in USD but pays many of its costs in TWD, the 1.5% depreciation of the New Taiwan Dollar makes its local costs look "cheaper" on the balance sheet.

But apart from this, other factors may hinder the margins from going further up and even bring them down.

Another factor worth mentioning is the overseas fab dilution. By trying to avoid geopolitical risks, TSMC is increasingly expanding its production presence in the US. In fact, more fabs overseas, and particularly in the States, would mean higher-than-expected costs – more capex, depreciation and higher operating expenses. Not to mention that depreciation is the single largest expense on TSMC’s income statement, representing nearly 50% of the cost of revenue. According to SemiAnalysis, the Taiwan facility production cost per wafer for 5nm was $6,681, while in the USA, it was $16,123 – 2.4 times higher.

As these overseas fabs contribute a larger percentage of total output, the "blended" gross margin of the company will naturally trend lower compared to when they were Taiwan-based. The US CHIP Act will offset these costs, but to a limited extent.

Valuation

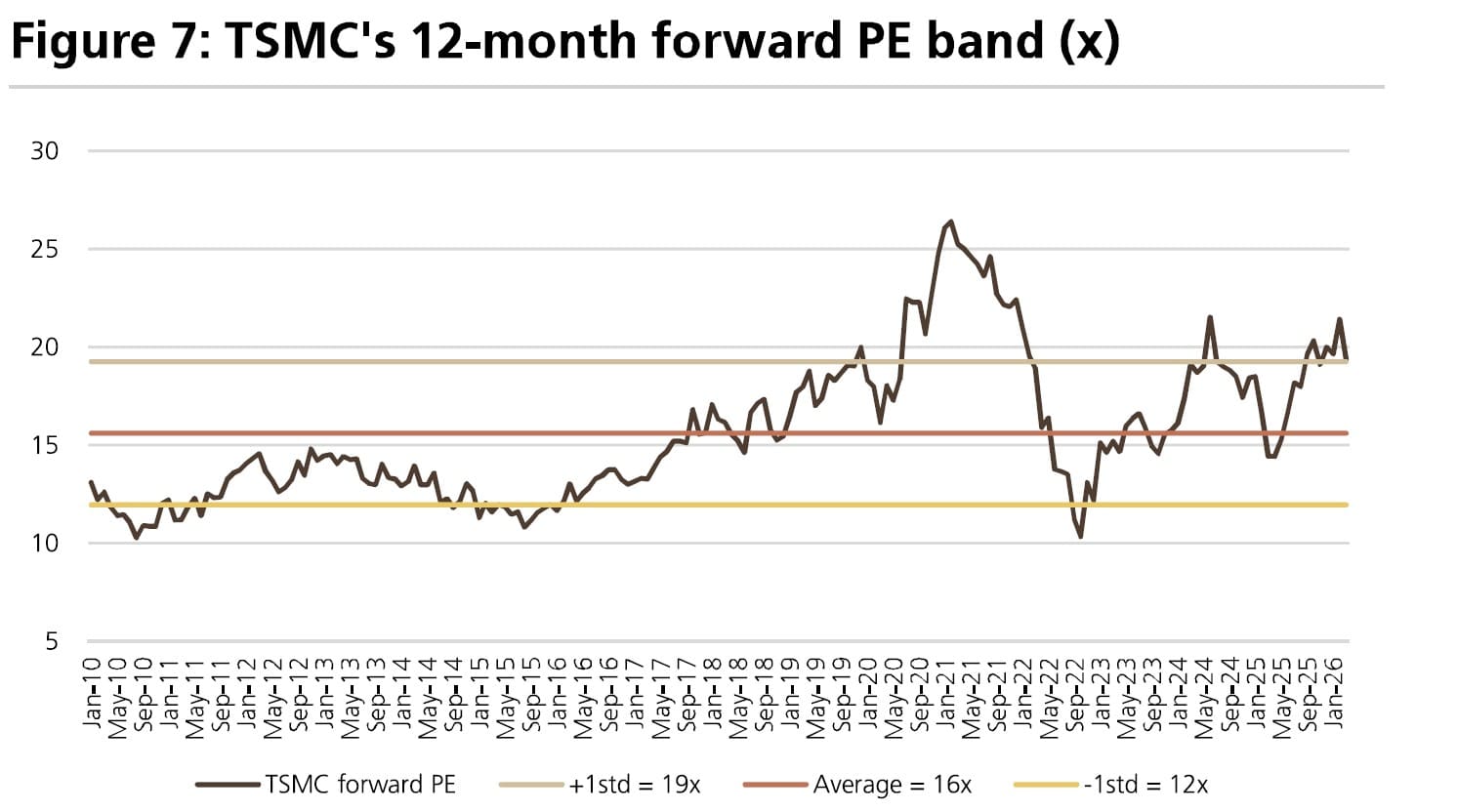

Judging from all this, TSMC seems like a rather low downside/low upside play. The tight supply situation will take time to resolve, and the competitive position of TSMC is very hard to dispute by Samsung and Intel. However, that seems to be priced in.

In terms of forward PE, TSMC is already trading at above low-20s times the earnings, which is higher than the historical average, but still not crazy expensive.

Source: UBS

The issue here is that the current top-line growth rates of 30% and above cannot stay at these levels for long. Once more wafer capacity enters the market, the pricing power will gradually wane, and this will be reflected in the revenue growth. Also, there are enough headwinds (higher depreciation and more expensive US-based fabs) to believe that margin upside is limited too.

Taking all these factors into account, we don’t see much upside for the stock price.

Recommended Articles