Breaking: USD/INR hits record highs amid spike in oil prices, Fed’s hawkish hold

- The Indian Rupee slides to record lows around 95.35 against the US Dollar.

- Oil prices rally further as US President Trump vows to prolong the blockade on Iran.

- More Fed members call for a shift from easing bias.

The Indian Rupee (INR) plunges to record lows against the US Dollar (USD) at open on Thursday. The USD/INR pair jumps to near 95.35 as oil prices rally due to continued United States (US) blockade of Iranian sea ports and a further recovery in the US Dollar (USD), following the Federal Reserve’s (Fed) monetary policy announcement on Wednesday.

At the press time, the WTI Oil price trades almost 1% higher at around $107.00, the highest level seen in over seven weeks.

Trump vows to prolong blockade on Iran

On late Wednesday, US President Donald Trump announced that he has rejected the recent peace proposal from Iran to reopen the Strait of Hormuz, a vital passage for almost 20% of global energy supply whose closure has prompted the supply crisis and has boosted oil prices, which could have delayed negotiations regarding Tehran’s nuclear ambitions.

US President Trump said that Washington will continue the naval blockade of Iran until he secures a deal with Tehran to address the country’s nuclear program.

Currencies from economies, such as India, which rely heavily on oil imports to meet their energy needs, tend to underperform in a high oil price environment.

US Dollar rises as some Fed members stress to shift from easing bias

The US Dollar extends its winning streak for the third trading day on Thursday, partly driven by risk-off sentiment and remarks from Fed Chair Jerome Powell that the “number of officials who would support a move away from an easing bias has increased”.

As of writing, the US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, trades marginally higher to near 99.10.

On Wednesday, the Fed left interest rates steady in the range of 3.50%-3.75%, with an 8-4 majority. One member dissented in favor of a rate cut, while three dissented against the inclusion of an easing bias, according to the monetary policy statement.

In the press conference, Fed Chair Powell warned that the central bank is vigilant to “risks on both sides of our mandate”, adding, “Developments in the Middle East are contributing to uncertainty.”

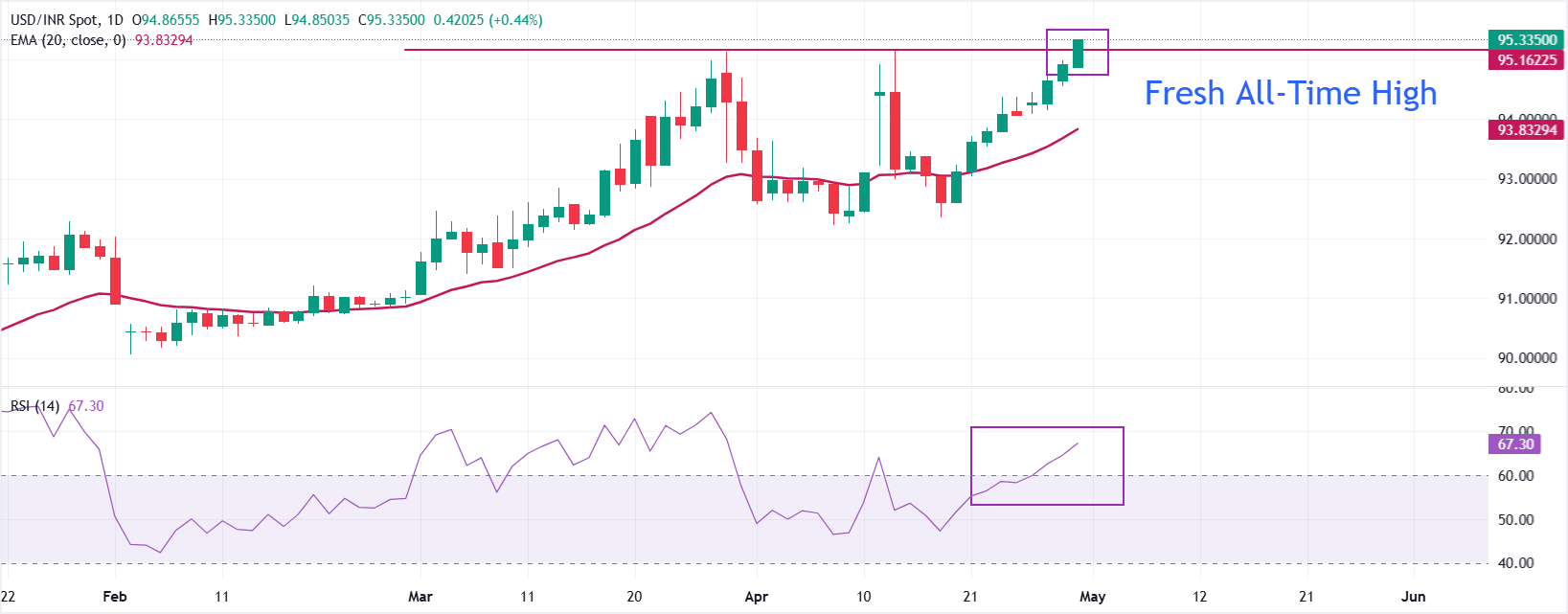

Technical Analysis: USD/INR hits fresh highs around 95.35

USD/INR rallies to near 95.35 on Thursday, the lifetime highest level. The pair holds a firm bullish bias as spot remains well above the 20-period Exponential Moving Average (EMA) at 93.83, keeping the short-term uptrend intact.

The Relative Strength Index (RSI) hovers near 67, indicating strong but not yet extreme upside momentum, which suggests buyers still retain control, though the risk of overextension is building.

On the downside, initial support is aligned with the 20-EMA around 93.83, where a deeper pullback would be expected to attract dip buyers and maintain the broader advance while it holds. A daily close below this dynamic floor would hint at fading upside pressure and open the door to a more extended correction toward prior price congestion levels not yet tested in the current leg. Looking up, the price has entered uncharted territory and will likely extend its rally towards 96.00.

(The technical analysis of this story was written with the help of an AI tool.)

Indian Rupee FAQs

The Indian Rupee (INR) is one of the most sensitive currencies to external factors. The price of Crude Oil (the country is highly dependent on imported Oil), the value of the US Dollar – most trade is conducted in USD – and the level of foreign investment, are all influential. Direct intervention by the Reserve Bank of India (RBI) in FX markets to keep the exchange rate stable, as well as the level of interest rates set by the RBI, are further major influencing factors on the Rupee.

The Reserve Bank of India (RBI) actively intervenes in forex markets to maintain a stable exchange rate, to help facilitate trade. In addition, the RBI tries to maintain the inflation rate at its 4% target by adjusting interest rates. Higher interest rates usually strengthen the Rupee. This is due to the role of the ‘carry trade’ in which investors borrow in countries with lower interest rates so as to place their money in countries’ offering relatively higher interest rates and profit from the difference.

Macroeconomic factors that influence the value of the Rupee include inflation, interest rates, the economic growth rate (GDP), the balance of trade, and inflows from foreign investment. A higher growth rate can lead to more overseas investment, pushing up demand for the Rupee. A less negative balance of trade will eventually lead to a stronger Rupee. Higher interest rates, especially real rates (interest rates less inflation) are also positive for the Rupee. A risk-on environment can lead to greater inflows of Foreign Direct and Indirect Investment (FDI and FII), which also benefit the Rupee.

Higher inflation, particularly, if it is comparatively higher than India’s peers, is generally negative for the currency as it reflects devaluation through oversupply. Inflation also increases the cost of exports, leading to more Rupees being sold to purchase foreign imports, which is Rupee-negative. At the same time, higher inflation usually leads to the Reserve Bank of India (RBI) raising interest rates and this can be positive for the Rupee, due to increased demand from international investors. The opposite effect is true of lower inflation.

Recommended Articles