Intel Has a Warning for AMD Stock Investors

Key Points

Intel's 18A-P process node promises robust performance and efficiency gains over the 18A process node.

The company is already witnessing strong demand for its 18A chips, and the new process node could help land more customers.

Intel has been losing ground to AMD in CPUs, and its 18A-P process node could help arrest the market share slide.

- 10 stocks we like better than Intel ›

Intel (NASDAQ: INTC) has been losing ground to Advanced Micro Devices (NASDAQ: AMD) in the server central processing unit (CPU) market, primarily due to the superior performance and lower costs of the latter's Epyc server CPUs.

In fact, AMD seems better-positioned to capitalize on the growth of the server CPU market right now. After all, AMD is gaining share at a nice clip in server CPUs, a market that has received a nice shot in the arm thanks to the growing demand for AI inference workloads. Intel, however, is preparing to fight back against AMD, as evident from its latest move.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Intel.

Intel is looking to close the technology gap with AMD

Intel recently announced that its advanced 18A-P process node is now in risk production. This is the stage during which chips are produced in low volumes to gather data on whether they will meet customer requirements, what their defect rate is, and whether they deliver the claimed performance and efficiency gains.

It is worth noting that Intel 18A-P is a refined version of the company's 18A process node. The company is promising a 9% improvement in performance compared to the 18A at identical power consumption. Meanwhile, the 18A-P node uses 18% less power while operating at the same performance level as the 18A. Even better, Intel points out that the refined process node is 20% to 40% more thermal resistant, suggesting that it will cost less to cool.

The risk production phase is ideally followed by volume production within the next 12-24 months, as noted by Tom's Hardware. However, as this is the refined version of an existing node, it is likely to take less time to get to that point. Intel has started volume production of client and server chips based on the 18A process already and noted on the April earnings call that this is the "fastest new product ramp in five years."

Importantly, the Xeon 6 server processor, manufactured using Intel 18A, is gaining traction among server CPUs. Nvidia has selected it for its Rubin rack-scale servers. Moreover, Intel points out that demand for its Xeon server CPUs exceeds, suggesting that the company's most advanced process node could allow it to arrest the market share slide it has been experiencing in the CPU market.

Of course, it remains to be seen how Intel 18A-P fares in the risk production phase. However, since the company has already brought the 18A into volume production, there is a good chance the 18A-P will make the cut and enter volume production as well. This could give Intel a much-needed boost against AMD.

Why the 18A-P process could be an important one for Intel

Intel's share of the server CPU market slid by six percentage points year over year to 66.8% in the first quarter of 2026, according to Mercury Research. The chip giant's share of consumer CPUs, meanwhile, dropped by 5.5 percentage points to 70.4%. AMD accounted for the rest of the market.

What's more, AMD's revenue share of these markets is higher than its unit share, suggesting that it enjoys stronger pricing power. If Intel manages to deliver the performance gains it claims and helps lower costs for users by reducing cooling requirements, it can indeed stop AMD from clawing away more market share.

An important point worth noting is that Intel's data center and AI (DCAI) products and the foundry business are already showing promising signs of growth. The company's DCAI revenue increased by 22% year over year in Q1 to $5.1 billion, while the foundry business recorded 16% growth to $5.4 billion. The mass production of the 18A-P node could give both these businesses a shot in the arm.

While Intel will be able to produce more powerful and power-efficient chips thanks to a more advanced node, it is believed that the 18A-P could help it land Apple as a foundry customer. Given that the DCAI and foundry segments produced a combined $10.1 billion revenue out of Intel's overall revenue of $13.6 billion in Q1, they can move the needle in a bigger way for the company, thanks to its product development moves.

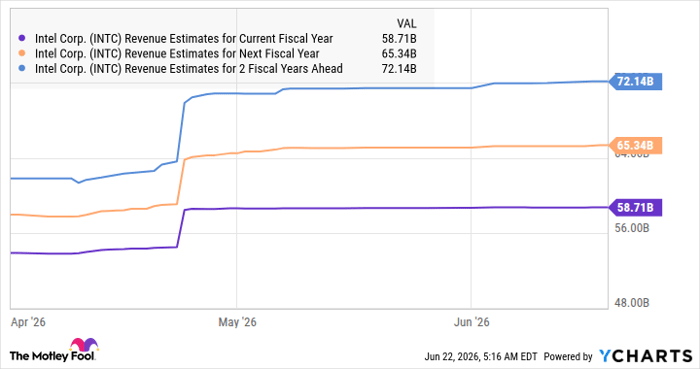

As a result, don't be surprised to see Intel's revenue growth exceeding analysts' expectations of around 10% growth going forward.

Data by YCharts

That's why it may be a good idea for investors to continue holding this AI stock, as the advancements it is making on the product side could help it deliver stronger-than-expected growth, which may translate into more stock price upside.

Should you buy stock in Intel right now?

Before you buy stock in Intel, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Intel wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $417,305!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,293,148!*

Now, it’s worth noting Stock Advisor’s total average return is 936% — a market-crushing outperformance compared to 209% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 22, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Intel, and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles