Got $2,000? Here's Why This Trillion-Dollar Memory Giant Is a Screaming Buy Before June 24.

Key Points

The memory chip market is historically cyclical.

Micron could be poised for further upside with solid results.

- 10 stocks we like better than Micron Technology ›

Few stocks have been as exciting to invest in as Micron Technology (NASDAQ: MU) has over the past few months. Sky-high demand for memory chips has driven Micron's revenue and earnings to swell, resulting in unprecedented business growth. On June 24, investors will get another update on the strength of the business, and the odds are good that Micron will report even greater demand for memory chips than before.

I think Micron's stock could be a great one to scoop up before it reports earnings on June 24, as there's one metric that still makes it look cheap.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

Micron still trades at a cyclical discount

Micron makes memory chips, which are widely used in nearly every computing device. The biggest computing demand over the past few years has come from data centers used specifically for artificial intelligence (AI) workloads. Micron and its peers have been unable to keep up with demand, so prices for their products have soared, leading to huge revenue and earnings growth.

The problem is, investors have seen this before with Micron. The memory chip market is cyclical, with demand rising and falling with economic activity. The biggest question surrounding the memory chip crunch is how long it will last. If the market is nearing the top of the cycle, then investors shouldn't be sticking around to see the bottom. But if it's just the beginning, Micron has a lot more upside.

One of the AI build-out leaders is Nvidia, and it has provided investors with valuable long-term insights. It believes that next year, data center capital expenditures will reach $1 trillion, up from $650 billion in 2026. Long term, Nvidia expects $3 trillion to $4 trillion in global data center capital expenditures by 2030, so there's clearly a huge runway for Micron to grow into.

While the memory chip market is historically cyclical, Micron is entering perhaps one of the longest demand curves it has ever experienced, which means it doesn't need to be valued like a cyclical company right now. But it still is.

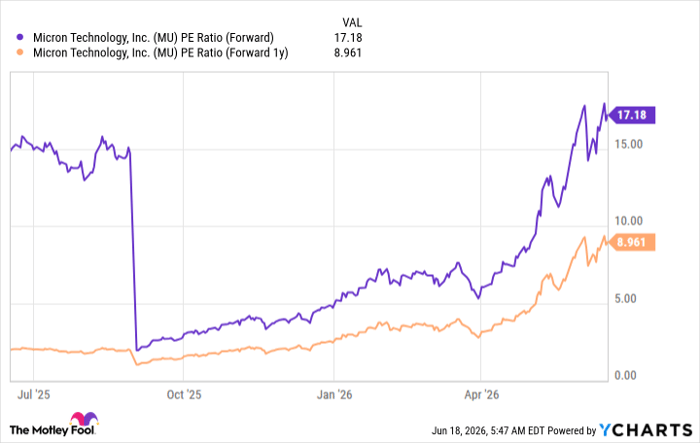

Normally, cyclical companies can't trade at about a 50% discount to their peers, which is why Micron appeared so cheap at the start of the year. However, the market has seen the results and anticipates a strong future, yet the stock still appears fairly cheap.

MU PE Ratio (Forward) data by YCharts

Micron's fiscal year 2026 ends in August, so using FY 2027 earnings is also a solid way to value the stock. With Micron trading at 7 times forward earnings and 9 times FY 2027 earnings, I think it's still a solid bargain and has plenty of room to run, making it a buy before it reports earnings on June 24.

Should you buy stock in Micron Technology right now?

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $417,305!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,293,148!*

Now, it’s worth noting Stock Advisor’s total average return is 936% — a market-crushing outperformance compared to 209% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 22, 2026.

Keithen Drury has positions in Nvidia. The Motley Fool has positions in and recommends Micron Technology and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles