JPMorgan's Latest Forecasts Are Bullish for Gold: Buy the Dip

Key Points

JPMorgan remains bullish on gold despite a reduced forecast.

Central bank demand, including from China, is a key driver.

Buying gold on dips is a good idea amid ongoing global uncertainties, rising debt levels, and the threat of inflation.

- These 10 stocks could mint the next wave of millionaires ›

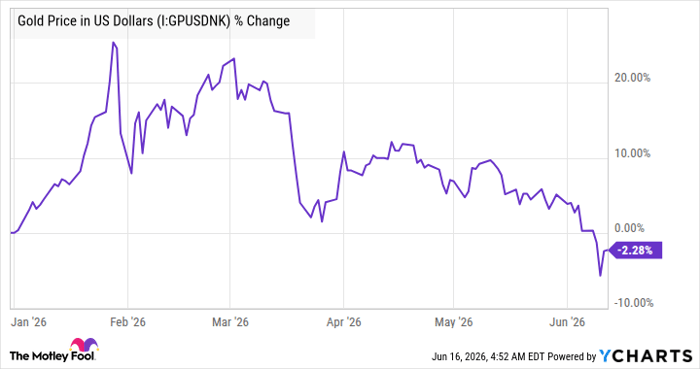

The price of gold has dipped to about $4,320 per ounce in 2026, and forecasters, including JPMorgan, have had to reduce their full-year gold price forecasts accordingly. Still, even though JPMorgan reduced its 2026 forecast to $5,243 per ounce from $5,708, it still implies gold reaching $5,000 per ounce in the fourth quarter -- a 39% increase.

While that forecast may prove overly optimistic, the rationale behind it is sound, and gold remains an attractive asset. Here's why.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Underlying gold demand

JPMorgan Global's argument is that while rising interest rates risk making gold a less attractive asset to hold, longer-term themes driving underlying demand remain in place. These factors include a higher inflationary environment and a concomitant erosion of purchasing power; ongoing U.S. budget deficits and rising debt; continuing geopolitical tensions that may encourage a reduced appetite for U.S. debt; and "U.S. policy unpredictability."

Image source: Getty Images.

While this is not the place to analyze the causes of these factors or their rights and wrongs, it's hard to argue that these issues are going away anytime soon.

One way to see their effects is in the gold demand data published by the World Gold Council. The chart below tracks first-quarter demand over the last 25 years and shows a notable reduction in jewelry demand (red bar) and stable technology demand (yellow). Meanwhile, investment demand (bars, coins, and exchange-traded funds; green and orange bars) has become more important. However, the key swing factor over the years has been the shift in central bank net purchases.

Data source: World Gold Council. Chart by author.

JPMorgan's argument is that China appears to be ramping up gold purchases in the first quarter, even as jewelry and investment demand declined sequentially and year over year. In contrast, overall central bank demand increased sequentially and year over year in Q1.

The outlook for gold in 2026

Overall investment demand ramped strongly through 2025, and it's understandable if it moderated in Q1 2026.

Data source: World Gold Council. Chart by author.

The correction in investment demand is a major reason for the decline in gold prices this year, and it wouldn't be surprising to see further weakness in the near term.

Data by YCharts.

Still, the case for gold remains strong, driven by the assumption that there's little likelihood of an outbreak of geopolitical reconciliation or budgetary discipline anytime soon. As such, it makes sense to have a bias toward buying on any sustained dip in the price of gold.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, Stock Advisor’s total average return is 920%* — a market-crushing outperformance compared to 207% for the S&P 500.

They just revealed what they believe are the 10 best stocks for investors to buy right now, available when you join Stock Advisor.

See the stocks »

*Stock Advisor returns as of June 18, 2026.

JPMorgan Chase is an advertising partner of Motley Fool Money. Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends JPMorgan Chase. The Motley Fool has a disclosure policy.

Recommended Articles