Alibaba’s Silent Rebuild: Valuation Anchored in Efficiency, Not Explosive Growth

- Alibaba expects $1.76 EPS and $33.26 billion in revenue for FQ4 2025, with 25.7% YoY EPS growth.

- Cloud and AIDC are fueling growth, with cloud up 13% YoY and AIDC expanding 32%.

- Free cash flow remains strong, with disciplined cost management and $1.3 billion in share repurchases.

- Alibaba is trading below historical P/E multiples, offering potential for re-rating if fundamentals continue to improve.

TradingKey - Alibaba is due to report FQ4 2025 earnings on May 15 pre-market, with expectations at $1.76 in normalized EPS and $33.26 billion in revenue. Following the strong Q3 beat, in which earnings per share exceeded estimates by $0.29 and revenue exceeded expectations by more than $300 million, consensus estimates see 25.7% YoY EPS growth in Q4, as the business delivers operating leverage with tighter cost containment, led by cost management in marketing and general expenses. Importantly, EPS estimates have been increasingly net positive in recent weeks (9 positive to 3 downward), signaling confidence in Alibaba's simplified capital allocation model and operating trajectory.

Core growth will depend on Alibaba Cloud and the International Digital Commerce Group (AIDC). Cloud Intelligence achieved 13% YoY growth during the last quarter, with EBITA up 33% due to the triple-digit growth of its AI product. Expansion of its footprint with the launch of Qwen 2.5-Max and open-sourced multimodal models should persist. AIDC grew 32% during the last quarter, driven by cross-border advances by AliExpress and Trendyol. Even though still losing money, the segments are growing into profitability with better unit economics and increased platform stickiness, particularly as it deepens its presence in Europe and the Gulf.

Shareholders will keep an eye out for stabilization in China Commerce's margins as well. CMR grew 9% at Taobao/Tmall during Q3, but direct sales fell 9% as underperforming niches were trimmed by Alibaba. With FCF generation steady and share repurchases of $1.3 billion during the previous quarter, the street will look for buybacks to persist and confirmation of further simplification of the portfolio. With trailing-annual earnings of $9.04 and forward PE approaching 14x, well below global peers, the re-rating catalyst for Alibaba's Q4 report may come if Cloud and AIDC's current trajectory is maintained and China retail demonstrates discipline in its margins.

Source: Fiscal Q3 Deck

A Platform Refresh: Monetizing Across Segments

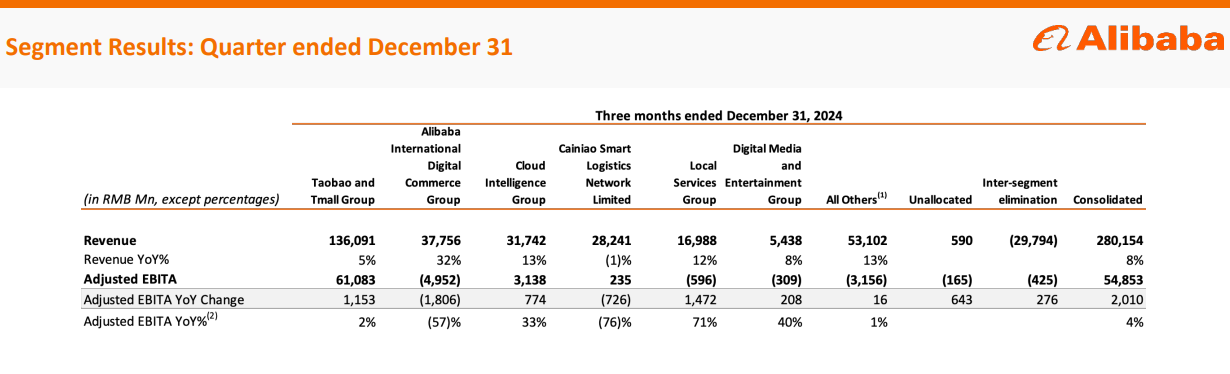

Alibaba's last quarter reflects the deep transformation: Taobao and Tmall, the whole narrative before, now represent merely one chapter. Yes, they still underpinned 9% YoY growth in customer management revenue (CMR) and a 2% adjusted EBITA increase, but the more compelling pivot is its diversified base of operations. China's retail revenue increased by 5% in total, but what is hiding beneath is a tactical 9% reduction from direct sales revenue as part of its pullback. This transition from volume-for-the-sake-of-volume to focus-commerce is at the heart of the new Alibaba.

The highlight was undoubtedly the Alibaba International Digital Commerce Group (AIDC), whose revenue grew 32% YoY to RMB37.8 billion ($5.17 billion). AliExpress and Trendyol retail commerce drove the growth, but at the cost of increased EBITA loss due to aggressive user acquisition spending during global shopping festivals and accelerating market growth in Europe and the Gulf. Sequential unit economics for AliExpress Choice, however, grew, indicating eventual profitability leverage as fixed costs stabilized. Significantly, AIDC's EBITA margin trend is reminiscent of Amazon's early international stages, with early losses accompanied by structural platform investment.

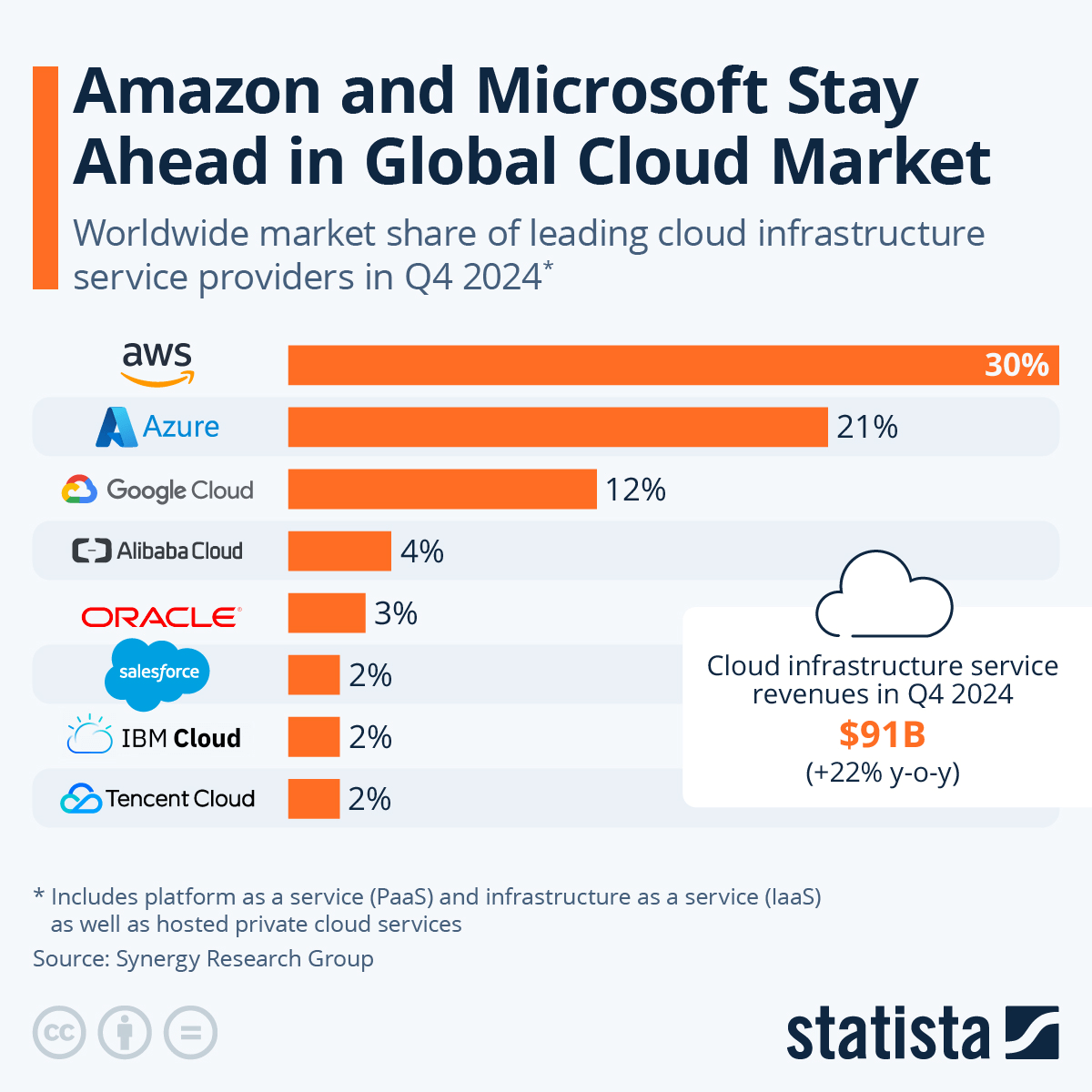

Equally strategic is Cloud Intelligence Group, expanding 13% YoY to RMB31.7 billion ($4.35 billion), with EBITA growing 33%. Public cloud, specifically AI infrastructure, remains dominant, with AI-related revenue posting six consecutive quarters of triple-digit growth. Alibaba's dominance in this space was bolstered by its identification in Gartner and Forrester reports and its fast-growing open-source Qwen model family, now producing more than 90,000 derivative models. In comparison to U.S. hyperscalers under commodity pressure, Alibaba's shift to AI supports both top-line and EBITA growth, a singular lever in an otherwise commoditizing cloud.

Even Cainiao, traditionally a drain on cash, reduced its losses during a revenue decline. EBITA decreased 76% YoY after restructurings but conceals from view a sensible move to better alignment with Alibaba's commerce platforms. Local Services and Digital Media similarly reduced losses, evidencing the group's broad efficiency drive.

Source: Fiscal Q3 Deck

The Competitive Chessboard: Carving a Moat Amid Fragmentation

Alibaba is no longer playing to take every vertical. Rather, it is building competitive defensibility through selective positioning. In China, although JD.com and Pinduoduo still pressure Alibaba in low-cost and logistics commerce, Alibaba is strategically using membership-driven loyalty and enhanced merchant services to drive high-LTV customers. Domestically, the 49 million 88VIP members, a double-digit YoY, are the stickiest user base, generating resilient monetization even as direct sales decline.

Internationally, it's playing a higher-level game. Amazon is still the champion in North America and Western Europe, but AliExpress and Trendyol from Alibaba are making calculated plays into underpenetrated countries like the Gulf and South Korea. Its acquisition of Shinsegae's partnership for AliExpress Korea is a bold move to localize, albeit one Amazon does relatively infrequently, implying a differentiated go-to-market approach focusing on partnership and culture fit.

Alibaba's competitive position is challenged by Tencent Cloud domestically in China and AWS, Azure, and GCP internationally. Yet its government-friendly offerings and control of China's public sector and education verticals provide it with regulatory moat protection. In addition, its open-source AI model with the Qwen family potentially provides platform-like network effects, like Hugging Face's but with Chinese language priority, underappreciated in light of China's trend toward AI localization.

Even in logistics, Cainiao no longer seems so keen to compete head-on against SF Express or JD Logistics. Rather, it is increasingly looking to play the role of back-end logistics enabler well-integrated with Alibaba's commerce platforms and third-party services, generating margin-buffered utility instead of being an independent growth engine.

Source: Statista

Flywheels, FCF & Financial Resilience: Everybody's Favorite Operating

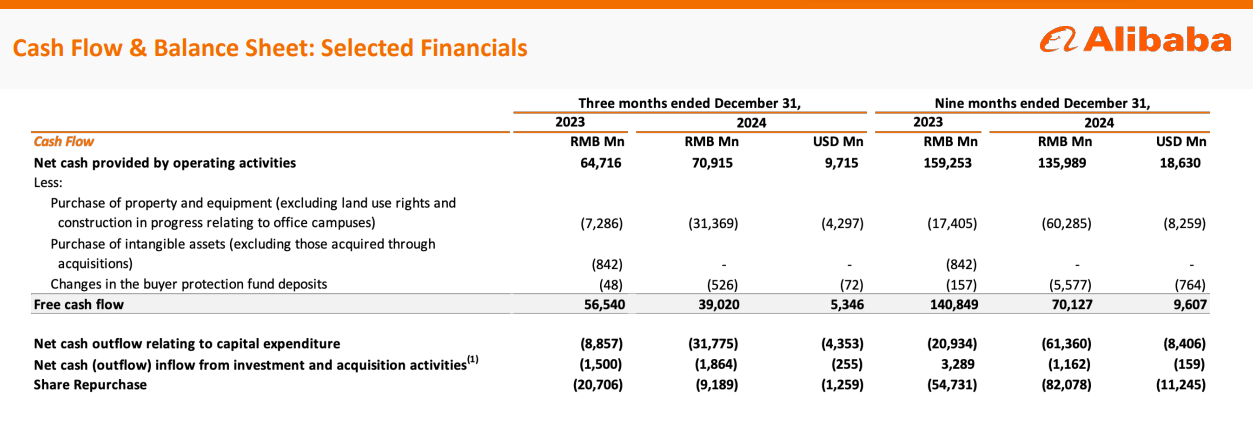

Alibaba's quarterly results for December unveil a quietly compounding efficiency of the company. Adjusted EBITA grew 4% YoY to RMB54.9 billion ($7.5 billion), and free cash flow accelerated, backed by a solid RMB378.5 billion ($51.9 billion) net cash position. This balance sheet strength provides Alibaba with the rare freedom to fund growth, buy back stock, and service debt at the same time, as seen in the issuance of $5 billion of bonds and repurchases of $1.3 billion in Q4.

Cost discipline is seen in all significant categories. Product development spending was flat as a percentage of revenue, and the intensity of the model in terms of sales and marketing fell YoY from 15% to 11.8%, demonstrating discipline without starving growth. G&A even was kept in check. This is part of a larger trend: unit economics are getting better across local services, cloud, and media, suggesting embedded-margin optionality as the model gets larger.

Segment EBITA trends reinforce the same. Cloud EBITA increased by 33% due to the AI mix shift and accretion from the public cloud. Local Services and Media losses decreased 71% and 40% sequentially from the year-ago period. These are not superficial fixes; they are indicative of a business that has inducted cost discipline right across segments. AIDC is the sole red spot, but even there, the sequential trend in margins is shifting.

What's most underappreciated is the compounding power of the share repurchase engine at Alibaba. With only a 0.6% net share count reduction in the last quarter, the headline dilution might appear small. Yet, ongoing repurchases at current depressed valuations build material embedded value per share over time, all the more so with strengthening FCF conversion from growth segments such as Cloud and International Commerce.

Source: Fiscal Q3 Deck

Revised Valuation Section: Alibaba's Valuation Based on Compressed Multiples in Light of Operating Strength

Alibaba's valuation is still significantly discounted against its historical standards and industry averages, even in the face of structural improvements in its operations. As of May 7, 2025, it is still trading at 14.63x trailing non-GAAP P/E and 14.23x forward P/E (non-GAAP), at a 22.8% and 5.7% discount, respectively, to its 5-year averages. GAAP metrics indicate similar compression, with the forward P/E at 16.47, well below the historical average of 21.48. This compression in valuation has been ongoing even as Alibaba has recorded 25%+ YoY EPS growth in the last quarter and has exceeded earnings estimates routinely.

On a PEG basis, its current PEG ratio is merely 0.70 (trailing) and 0.76 (forward non-GAAP), with the stock's earnings growth not being priced in completely. With its forward PEG ratio at 48% below the sector median of 1.46, there's undervaluation when adjusted for growth. Equally, EV/sales and EV/EBITDA ratios reflect operational efficiency and scale benefits not factored into current price multiples. Its forward EV/EBITDA is at 10.00, roughly 14% below its 5-year average and still near the sector median, even as its cloud and international segments deliver superior growth and margin trajectories.

The stock's price-to-cash-flow ratios are slightly higher (13.28x trailing, 13.49x forward) but represent intensified free cash flow generation after restructuring, not deteriorating quality. At just 1.57% dividend yield, below the sector median, the value story in Alibaba isn't about payouts but compounding at its core. The 2.15x P/B is slightly above the sector median and is supported by a balance sheet with $51.9 billion in net cash and a lean, cash-producing operating model. In short, Alibaba is an unusual compounder still trading like a restructuring risk, with asymmetric re-rating potential if market sentiment matches up with better fundamentals.

Source: Precedence Research

Risks: Lag in Restructuring, Political Winds, and Market Myopia

Alibaba's restructuring provides both marginal and strategic leverage, but execution risk is present. Sun Art and Intime divestitures simplify, yet won't significantly drive margins unless discipline in reinvesting declines. AIDC profitability is still a multi-quarter work in process, and regulatory resistance in international markets, particularly in Europe, will limit market share reach regardless of JV initiatives.

China's macro environment is also at risk. Any tightening of policy or pullback from consumers will weaken domestic retail and logistics growth. In addition, even with enhanced capital control, the conglomerate model confines transparency, with the potential to discourage U.S. institutional capital until segment reporting is made easier after reorganization.

Finally, there is ongoing US-China geopolitical tension. Any escalation, delisting threats, restrictions on exports, or barriers to the flow of capital might disproportionately impact Alibaba's investor base and valuation multiples, even where fundamentals are strong.

Alibaba's quarter in December represents a structural inflection point. No longer the growth-at-any-cost juggernaut, it is now a leaner, strategically diversified platform compounding quietly both efficiency and shareholder value. With cloud traction driven by AI, resilient commerce, and valuation contraction at cross-purposes to the business, Alibaba presents an asymmetric opportunity, not founded in hype, but in monetizable substance.

Source: BlackRock

Recommended Articles