This Glorious Growth Stock Is Up 68% in 12 Months. Here's Why More Gains Could Follow

Key Points

DigitalOcean provides cloud and AI services exclusively to small and medium-sized businesses.

The company's annual run-rate revenue for its AI business soared by a whopping 150% year over year in Q4.

Despite a 68% gain over the last 12 months, DigitalOcean stock still looks cheap based on two widely used valuation metrics.

- 10 stocks we like better than DigitalOcean ›

The cloud computing industry is dominated by trillion-dollar tech giants like Amazon and Microsoft, which offer hundreds of solutions to help their business customers thrive in the digital age. They include everything from simple data storage to complex software development tools.

DigitalOcean (NYSE: DOCN) is another cloud provider, but it exclusively serves small and medium-sized businesses (SMBs) with a targeted suite of cost-effective solutions. It's now using that blueprint to help its customers develop and deploy artificial intelligence (AI) software, by providing them with computing capacity from state-of-the-art data centers, and a growing portfolio of third-party models from companies like Anthropic.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

DigitalOcean stock has soared by 68% over the last 12 months, but with a market capitalization of just $5.7 billion, it's still a tiny player in the cloud and AI space. Here's why further upside might be on the horizon.

Image source: Getty Images.

Helping even the smallest businesses tap into AI

The largest providers in the cloud industry primarily focus on customers with the highest spending potential, so SMBs are often underserved. DigitalOcean built its entire business on filling that gap by offering SMBs highly personalized service, transparent and affordable pricing, and a simple dashboard which makes deploying cloud and AI services easy. This is an ideal combination of features for small enterprises with limited financial resources.

To serve its AI customers, DigitalOcean has set up a series of data centers fitted with advanced chips from suppliers like Nvidia and Advanced Micro Devices. It allows customers to start with just one chip and scale up as needed, which is perfect for deploying basic chatbots or web-based customer service assistants. DigitalOcean says its prices are up to 75% cheaper than similar infrastructure offered by the hyperscale cloud providers.

These data centers and chips provide the necessary computing capacity for AI workloads, but SMBs also need access to ready-made large language models (LLMs) to achieve their AI software or agentic goals. DigitalOcean's Gradient platform hosts the latest models from top developers like OpenAI, Anthropic, Meta Platforms, and more, giving SMBs a versatile set of options to cover all their needs.

Revenue growth is accelerating, thanks to AI

DigitalOcean had a record $970 million in annual recurring revenue (ARR) at the end of the fourth quarter of 2025, which was an 18% increase from the year-ago period. It was the second consecutive quarter in which that growth rate accelerated, primarily because of soaring demand for AI services.

In fact, DigitalOcean had $120 million in ARR from its AI products and services, specifically, which was up by an eye-popping 150% year over year. The company expects its overall revenue growth to accelerate to 21% in 2026 and then to 30% in 2027, thanks to the incredible momentum in its AI business.

DigitalOcean's strong top-line results also flowed to the bottom line in 2025. The company produced a generally accepted accounting principles (GAAP) net income of $259.3 million, which grew by a staggering 207% from the previous year.

Even after excluding a series of one-off tax benefits, DigitalOcean's adjusted net income still grew by 13% to $223.2 million for the year.

DigitalOcean stock still looks attractive

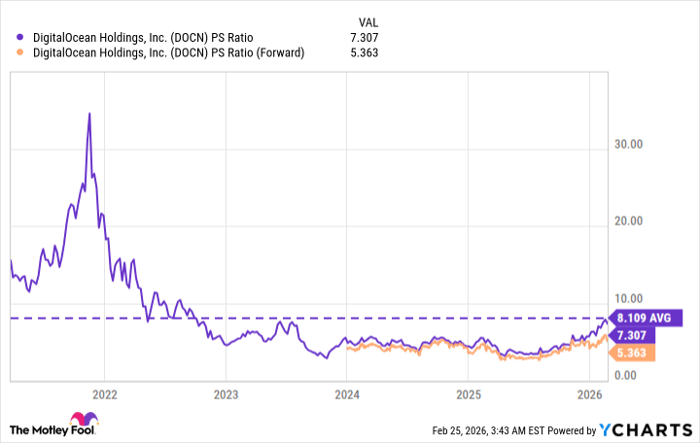

Despite the 68% gain in DigitalOcean stock over the past year, it's still trading at a price-to-sales (P/S) ratio of just 7.3, which is actually a discount to its average of 8.1 since going public in 2021. The stock looks even cheaper when measured against the company's forecasted 2026 revenue, which places it at a forward P/S ratio of just 5.3.

Data by YCharts.

In other words, DigitalOcean stock would have to soar by 51% before the end of this year just to trade in line with its long-term average P/S ratio of 8.1.

Moreover, based on DigitalOcean's 2025 GAAP earnings of $2.52 per share, its stock is trading at a price-to-earnings (P/E) ratio of just 24.9. That is a discount to the overall market, with the S&P 500 index trading at a P/E ratio of 25.4, and the Nasdaq-100 index trading at a P/E ratio of 31.6.

DigitalOcean stock looks cheap based on two widely used valuation metrics, so it certainly has room to build on its recent gains. That means it could be a great buy right now, especially for investors who are willing to hold it for at least the next two years. That will give the company time to deliver on its forecasted acceleration in revenue growth during 2026 and 2027.

Should you buy stock in DigitalOcean right now?

Before you buy stock in DigitalOcean, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and DigitalOcean wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $456,188!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,133,413!*

Now, it’s worth noting Stock Advisor’s total average return is 916% — a market-crushing outperformance compared to 194% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of February 27, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Amazon, DigitalOcean, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles