Prediction: This Overlooked AI Infrastructure Stock Could Double in 2026. Here's Why

Key Points

Seagate's earnings growth has accelerated amid strong demand for storage solutions in AI data centers.

The company should benefit from further price improvements in hard disk drives, which will lead to a significant earnings jump.

- 10 stocks we like better than Seagate Technology Plc ›

Seagate Technology (NASDAQ: STX) is playing a key role in the artificial intelligence (AI) infrastructure market, where the demand for data storage to help train models and run inference applications is increasing rapidly.

It may not be as popular as Sandisk or Micron Technology among investors, but Seagate has quietly clocked remarkable gains of 304% in the past year. The good part is that the company still has room for more upside in 2026, driven by heavy spending on AI data centers by hyperscalers and AI companies.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Let's look at the reasons this underrated tech company has the potential to double in 2026.

Image source: Getty Images.

AI-fueled storage demand has supercharged Seagate's growth

Seagate released its fiscal 2026 second-quarter results (for the three months ended Jan. 2, 2026) on Jan. 28. The company's revenue increased by 21.5% year over year to $2.82 billion. However, its earnings increased by a much more impressive 53% to $3.11 per share.

Seagate manufactures data storage solutions, including traditional hard disk drives (HDDs) and solid-state drives (SSDs). Its offerings are used in both enterprise and consumer applications. Seagate management points out that the adoption of AI applications is creating the need for more storage in data centers.

The demand for Seagate's high-capacity drives, used in data centers, was solid last quarter. Importantly, the company says that it has already sold all of the high-capacity nearline drive storage products it expects to produce in 2026 and has started accepting orders for the first half of 2027. Even better, Seagate anticipates the strong demand trend will continue beyond the next two years. According to CEO William Mosley:

Further out, demand visibility is strengthening based on the long-term agreements in place with major cloud customers through calendar '27. Additionally, multiple cloud customers are discussing their demand growth projections for calendar '28, underscoring that supply assurance remains their highest priority.

It is evident that demand for AI data center storage solutions exceeds supply. This has led to a big jump in the prices of both HDDs and SSDs. As Seagate and peer Western Digital have sold out their entire 2026 capacity, it is easy to see why HDD prices shot up by 50% this year.

Meanwhile, the prices of SSDs are 16 times those of HDDs. That's not surprising, as the shortage of HDDs has led AI data centers to turn to SSDs. This also explains why Seagate expects the HDD market's revenue to increase at a mid-teens compound annual growth rate between 2024 and 2028, as compared to a low-teens rate between 2026 and 2024.

Specifically, the company sees its addressable revenue opportunity almost doubling from $13 billion in 2024 to $23 billion in 2028, though don't be surprised if that number grows further due to the aggressive AI data center build-out in the coming years.

Here's why the stock can double this year

We have already seen that Seagate is clocking remarkable earnings growth due to the favorable demand-supply dynamics in the storage market. The good news for investors is that the trend is here to stay in 2026, which is why Seagate should be able to sustain its terrific earnings growth momentum.

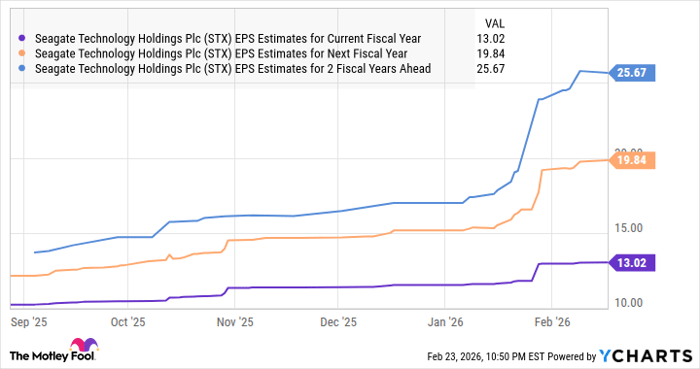

Analysts are anticipating a 61% increase in Seagate's earnings in the current fiscal year to $13.02 per share, followed by another solid increase in the next fiscal year.

Data by YCharts.

Seagate has already clocked $5.72 per share in earnings in the first half of fiscal 2026, indicating that it is poised to earn another $7.30 per share in the second half. The chart above shows that Seagate's earnings in fiscal 2027 (which will begin in July) are likely to land closer to $20 per share. Assuming Seagate earns half of that in the first half of fiscal 2027 (which will end in December 2026 or early January 2027), its earnings for calendar 2026 will land at $17.30 per share.

Multiplying the projected earnings by the U.S. tech sector's average price-to-earnings ratio of 41 suggests a stock price of $721. That's almost 77% higher than its current stock price. However, this AI stock could even double in 2026, as it could register stronger earnings growth due to the catalysts discussed above.

Seagate is already poised to increase earnings at a much higher rate than the broader market, which could lead the market to reward it with a higher multiple. Seagate's stock price could double this year, which is why investors should consider adding this tech stock to their portfolios before it soars to new highs.

Should you buy stock in Seagate Technology Plc right now?

Before you buy stock in Seagate Technology Plc, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Seagate Technology Plc wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $445,995!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,198,823!*

Now, it’s worth noting Stock Advisor’s total average return is 927% — a market-crushing outperformance compared to 194% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of February 26, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Micron Technology and Western Digital. The Motley Fool has a disclosure policy.

Recommended Articles