Oracle’s FY2026 Q1 Preview: Will OpenAI Contract Spark a Broadcom-Like Stock Surge?

TradingKey - Database software giant Oracle (ORCL.US) will release its Q1 FY2026 earnings after the market close on September 9, with investors closely watching for upbeat guidance on OCI revenue and backlog orders. As analysts raise targets and expectations, could Oracle’s stock replicate the post-earnings rally seen at Broadcom following its OpenAI-related contract announcement?

According to TradingKey’s consensus data, analysts expect:

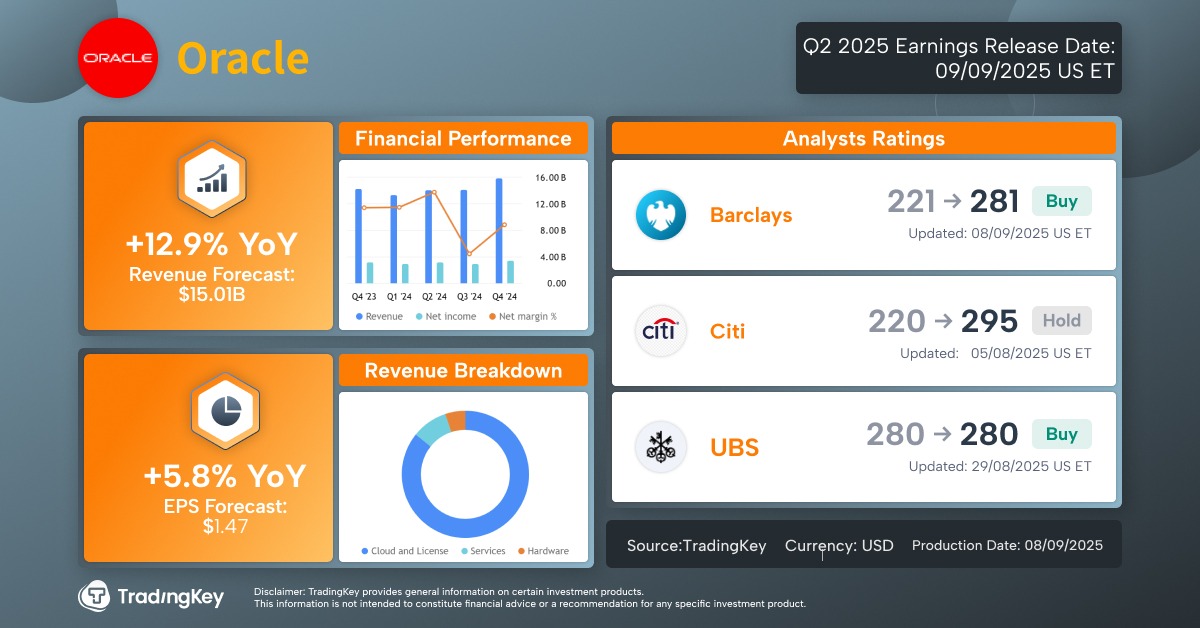

- Revenue: $15.01 billion, up 12.9% YoY

- EPS: $1.47, up 5.8% YoY

- Cloud revenue: $6.9 billion, up 23% YoY

When Oracle reported its Q4 FY2025 results in June, management delivered highly optimistic guidance, forecasting:

- FY2026 cloud revenue growth accelerating to over 40%, up from 24% in FY2025

- Cloud infrastructure growth rising to over 70%, up from 50%

Notably, Oracle projected RPO (Remaining Performance Obligations) — a key indicator of future revenue — to grow by over 100% in FY2026, driven by a rapidly expanding backlogged work.

The $30 Billion Contract

In early July, Oracle revealed a landmark cloud deal expected to generate $30 billion in annual revenue starting in 2028 — triple the size of its 2025 data center infrastructure revenue.

Reports from Bloomberg and the Financial Times suggest the client is OpenAI, marking a major step in the “Stargate” project — a joint U.S. AI infrastructure initiative. To support this, OpenAI is leasing 4.5 GW of data center power capacity from Oracle, equivalent to one-quarter of the total U.S. data center capacity today.

Barclays analyst Raimo Lenschow said the $30 billion deal significantly raises Oracle’s stakes during its seasonally slow period.

Lenschow noted that for the Q1 report, investors should focus on management commentary rather than just the quarter’s results. He expects more details on:

- The impact of the contract on RPO

- The capital expenditures required to fulfill the deal

TradingKey analyst Viga Liu said that driven by AI infrastructure demand and multi-cloud adoption, RPO is expected to grow further from last quarter’s $138 billion. The quarter’s performance will hinge on when large contracts go live and the pace of workload scaling.

Morgan Stanley analyst Keith Weiss expects Oracle could raise its FY2029 revenue target from $104 billion to $125 billion, fueled by recent contracts and growing backlog.

This narrative — where customer news drives growth optimism — echoes Broadcom’s recent 13% two-day stock surge after it disclosed a “$10 billion order”, widely believed to be from OpenAI. Oracle may now have a psychological blueprint for a similar rally.

Analysts Raise Targets Ahead of Earnings

In the days leading up to the report, several institutions raised Oracle’s price targets:

- Citi: $186 → $240

- Morgan Stanley: $175 → $246

- Barclays: $221 → $281

- TD Cowen: up to $325

Jefferies analysts remain bullish, citing leading indicators pointing to an inflection point in OCI revenue and backlog growth in coming quarters. However, they note that seasonal softness in software revenue and margins could partially offset the strong data.

Risks Amid High Expectations

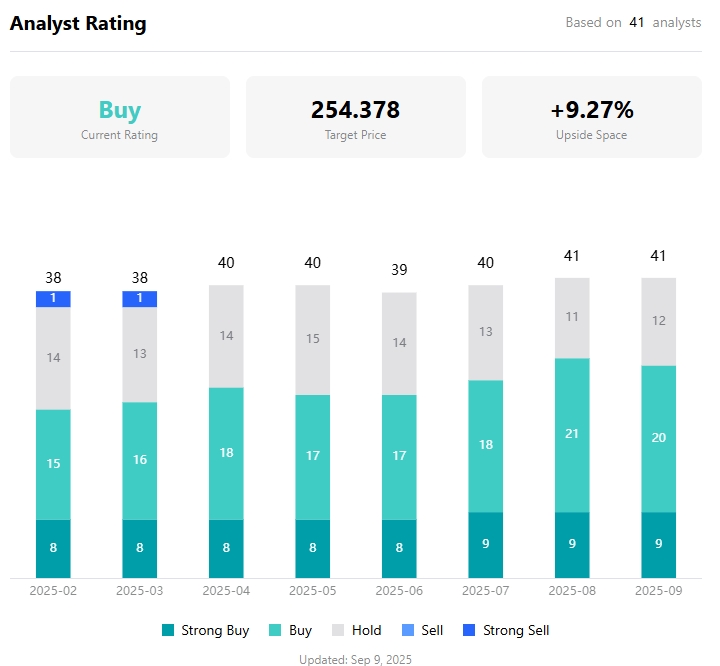

According to TradingKey, the Wall Street consensus target price for Oracle is $254.38, implying over 9% upside. However, 13 out of 40 analysts (32.5%) rate the stock as “Hold”, reflecting a cautiously optimistic sentiment.

Monness Crespi Hardt analysts maintain a Hold rating, arguing that while Oracle’s cloud transition and generative AI opportunities are promising, the stock appears overvalued. They also highlight concerns over high capital expenditures and negative free cash flow, which could limit financial flexibility.

Oracle’s forward P/E of 53.45 is at a 3-year high. Despite broad institutional buying in U.S. tech stocks, institutional holdings in Oracle dropped 0.29% MoM, according to TradingKey’s stock scoring tool.

While Morgan Stanley acknowledges AI-driven revenue growth, it warns that profitability may lag. The firm notes Oracle avoided reaffirming its prior 45% operating margin target for FY2026 in its last earnings call. Combined with recent AI-related layoffs, this suggests rising cost pressures.

Morgan Stanley points out:

- Legacy on-premise database: ~97% gross margin

- Strategic SaaS business: ~75% gross margin

- New AI infrastructure business: likely only ~40% gross margin

As a result, Morgan Stanley forecasts FY2029 as a year of “revenue growth without profit growth”, with operating margins falling from 44% in FY2025 to 39% in FY2029.

Recommended Articles