Sandisk Stock Was the Biggest Winner in the First Half of 2026. What's Next for the Second Half?

Key Points

The company is benefiting from a memory chip shortage that could last for several years.

While Sandisk's stock has soared, it still isn't all that expensive given the industry's outlook.

- 10 stocks we like better than Sandisk ›

Sandisk (NASDAQ: SNDK) is the best-performing S&P 500 stock so far in 2026, and it isn't particularly close. It's up around 800% so far in 2026, easily outperforming second-place Micron Technology, which is up "only" about 300%. That's a simply incredible performance for just six months.

Still, after a run like that, it's reasonable to wonder if there is further upside ahead or if Sandisk has delivered everything that it's going to deliver in 2026.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

Although it may seem surprising, I think there is plenty of upside left in Sandisk's stock in the second half of 2026, especially with the major shortages going on in its industry. While it won't return another 800% from here, it could still reward investors quite well.

Image source: The Motley Fool.

The memory chip shortage is getting worse

Sandisk makes NAND memory, which is primarily utilized for long-term data storage. Most of the NAND memory you'll encounter in a data center comes in the form of solid-state drives (SSDs), which are used for long-term information storage. Sandisk and its peers aren't used to the massive demand being generated by data centers, and this cohort doesn't have the production capacity necessary to meet demand. As a result, prices for memory chips are soaring, and Sandisk is benefiting from it.

Everyone in the industry is scrambling to stand up more capacity, but it may be a losing battle. Micron, another memory chip maker, believes that "tight conditions" will persist beyond 2027, which bodes well for the demand curve Sandisk is seeing.

Compounding this is a rapidly expanding data center build-out plan; Nvidia believes global data center spending could reach $3 trillion to $4 trillion annually by 2030. That creates an environment where Sandisk and its peers can succeed for a long time, making the stock an intriguing buy.

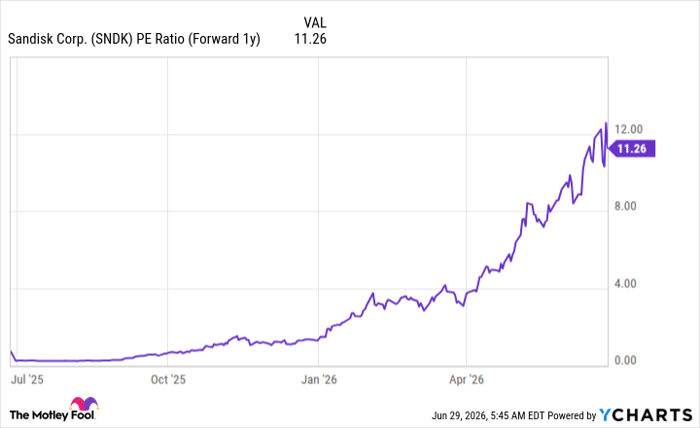

Wall Street analysts project major growth ahead for Sandisk, with fiscal fourth-quarter growth of 336% (ended in June) and 122% growth for fiscal 2027. As long as the stock is reasonably priced, this means Sandisk stock could easily go higher from here, and fortunately for investors, it is. I'm using fiscal 2027 estimates to value Sandisk's stock, since it just started:

SNDK PE Ratio (Forward 1y) data by YCharts

At 11 times fiscal 2027 earnings, Sandisk stock isn't very expensive, and could easily double from here and still be reasonably valued. As a result, I think Sandisk could head higher from today's levels, and makes for a great buy now.

Should you buy stock in Sandisk right now?

Before you buy stock in Sandisk, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Sandisk wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $418,761!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,195,804!*

Now, it’s worth noting Stock Advisor’s total average return is 918% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 4, 2026.

Keithen Drury has positions in Nvidia. The Motley Fool has positions in and recommends Micron Technology and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles