Is Palantir Stock a Buy Right Now? A Bullish Case Despite the YTD Pullback

$300M USDA Deal Signals Fresh Breath Beyond Defense

TradingKey - Before I get to my optimism, I believe it is worthwhile explaining why Palantir Technologies Inc (NASDAQ: PLTR) is currently at the present trough. First, according to Euronews, Palantir is facing headwinds in the European market by citing that the use of Palantir services risks the sovereignty of Europe. Well, while this could sound appropriate in the lens of self-sustenance for Europe, Palantir remains the company you don’t want, but you actually need.

Let’s see it from another perspective, what I mean here. After these headwinds, Palantir’s expansion in Europe is still happening. For example, according to EUPerspectives, European financial institutions are still increasing their shareholding at Palantir by nearly by 70% in 2025. BNP Paribas, Barclays, Deutsche Bank, and others altogether increased their take by $27 billion, which signals that the company has an undeniable growth projection. Despite headwinds in 2025, now to your surprise, Palantir reported a revenue of $4.6 billion in 2025, representing 56% YoY growth. So far, we can deduce that the sell-off is probably caused by investors’ concern about whether the company will recover from this, and my answer is that I believe it has the capacity to regain its upward momentum. But let’s save this for later under financials.

One reason I believe it will recover its bullish momentum is the current revenue guidance of $7.66 billion in 2026. This isn’t just a buzzword, but fundamentals keep proving possibilities. This now brings me back to my $300M USDA deal beyond the recent defense contract.

Beyond Palantir’s recent mega deal with the US Army, amounting to over $10 billion, the contracts keep coming in. According to CNBC, Palantir has been contracted by the US Department of Agriculture (USDA) in a $300 deal. Under this contract, Palantir will be managing farmland as a geopolitical risk that threatens global supply chains. From where I sit, these fundamentals give the company an upper hand in increasing its revenues, which is why I believe, as a growth-based investor, the current bearish market offers an entry point.

71% Revenue Guidance is a Sign Of Potential Upside For Growth-Oriented Investors

After recording a revenue of $1.282 billion, representing 85% YoY growth, in the latest quarter (Q1’2026), Palantir management has upgraded its FY2026 guidance to 21% YoY. In my view, two things are at play here. First is solid fundamentals, as explained above, such as a $300 million and $10 billion contract with the US defense. For example, since the contract performance has already started, annualizing revenue generation from this contract would mean $1 billion from this contract since it runs for 10 years.

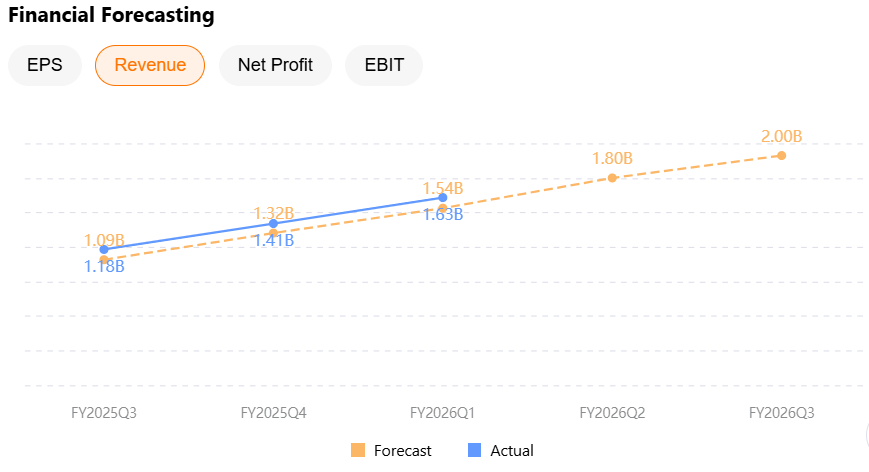

At 71% YoY revenue forecast, this is approximately more than $7.66 billion for the FY2026, up from $5.224 billion in FY2025. More so, Palantir’s top line has been beating analysts’ estimates, and the image below is a testament to this fact. This gives the impression that it is likely that the company has the potential to sustain its strong fundamentals. What you see as the current stock price trough, the solid fundamentals are now visible here under its revenue report card.

Since there are no serious or major foreseeable threats to Palantir’s current AI business at the moment, I will make some assumptions here. Now that the company was able to report a quarterly revenue of $1.282 billion, annualizing this revenue gives a revenue of $5.128 billion. Here is where the optimism lies: the Q2’26 guidance stands at around $1.797 billion to $1.801 billion. Q1’26, which saw a revenue growth of 85% YoY, resulted in a revenue beat by 18.08%. If all goes well, the company is likely to maintain a minimum of 10% revenue beat per quarter. This is because, as these contracts’ performance continues taking shape and more keep coming, issues such as the UK will not be a major factor in the revenue growth of the company.

Let’s see this in a more pragmatic way to unravel what I mean here, in the recent quarter Q1’26, 79% of the revenues came from the US, and only 8% of the total came from the UK at $130.091 million. The rest of the world revenue came in at $220.426 million. It also confirms that even when the UK ceases its contract with Palantir, the company has a high potential to make more from the rest of the world, which is why, to me, I believe Palantir remains a growth company. This answers why I believe that the UK issue, which resulted in the current trough, nears an end, and this serves as a better entry point.

Source: TradingKey

Source: TradingKey

What Does Peer Valuation Check Say?

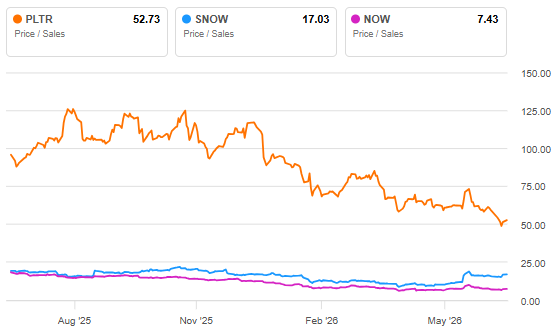

I will now value Palantir using Price-to-sales (P/S ratio) and comparing its peers, such as Snowflake Inc (NASDAQ: SNOW) and ServiceNow Inc (NASDAQ: NOW). A keen look at the P/S ratio between peers in the image below shows that all along, Palantir has been in the lead. Even now that it is experiencing a trough, its P/E ratio is 52.73x, significantly higher compared to SNOW at 17.03x and NOW at 7.43x. Honestly, at the current price, Palantir is expensive, but when you look at it from a growth perspective, it shows an undervaluation. Let’s take, for example, forward revenue growth below.

Source: Seeking Alpha

PLTR has a forward revenue growth YoY of 57.51%, which is a testament that the company’s current valuation is fair relative to its peers. NOW’s forward revenue stands at 20.50% and SNOW at 28.19%, which is a distant away from PLTR. Since I have a perspective about this company as a growth company, this is a testament to why I am optimistic about this company. Its growth is almost double that of its close peers.

Source: Seeking Alpha

Source: Seeking Alpha

Takeaway and Why I Reiterate My Buying

On June 29, PLTR’s stock price was traded above $115.88, this company was not cheap, but when compared to its peers, the fair price picture comes into play. The solid P/S multiple at 52.73x aligns with the fundamental optimism outlook of increasing contracts, long-term contracts, and other revenue drivers. Having said that, this P/S ratio shows a solid forward expectation over a deterioration, which to me is an angle worth considering. After all, at 85% revenue increase so far in Q2’26, with most of the revenues from the US, the company is likely to sustain this growth projection long-term.

Having said that, I will also consider my previous explanations in alignment with analysts’ estimates (Wall Street and Seeking Alpha) on the price target at a range of $186-$197, representing 30%-36% upside potential. To me, after looking at the current performance and the estimates, I believe a $200 price target is a solid possibility. Honestly, Palantir is no longer a speculative AI but a strongly embedded infrastructure with an increasing customer acceptance and a preferred government service provider. That said, I am reiterating my bullish stance.

Recommended Articles