Apple Q2 Fiscal Quarter Preview: iPhone Sales Grow Against the Trend, But Cost 'Sword of Damocles' Hangs High

TradingKey - After the market close on April 30, ET, Apple (AAPL.US) will release its fiscal second-quarter 2026 financial results. This marks the first earnings report since Tim Cook announced his retirement plan.

Return to Steady Growth

In the first quarter of fiscal 2026, Apple just set a record high revenue of $143.8 billion. iPhone revenue rose 23% year-over-year to $85.3 billion, and Greater China revenue increased 38% year-over-year to over $25.5 billion, beating market expectations by $4.7 billion and becoming the strongest engine behind Apple's record growth.

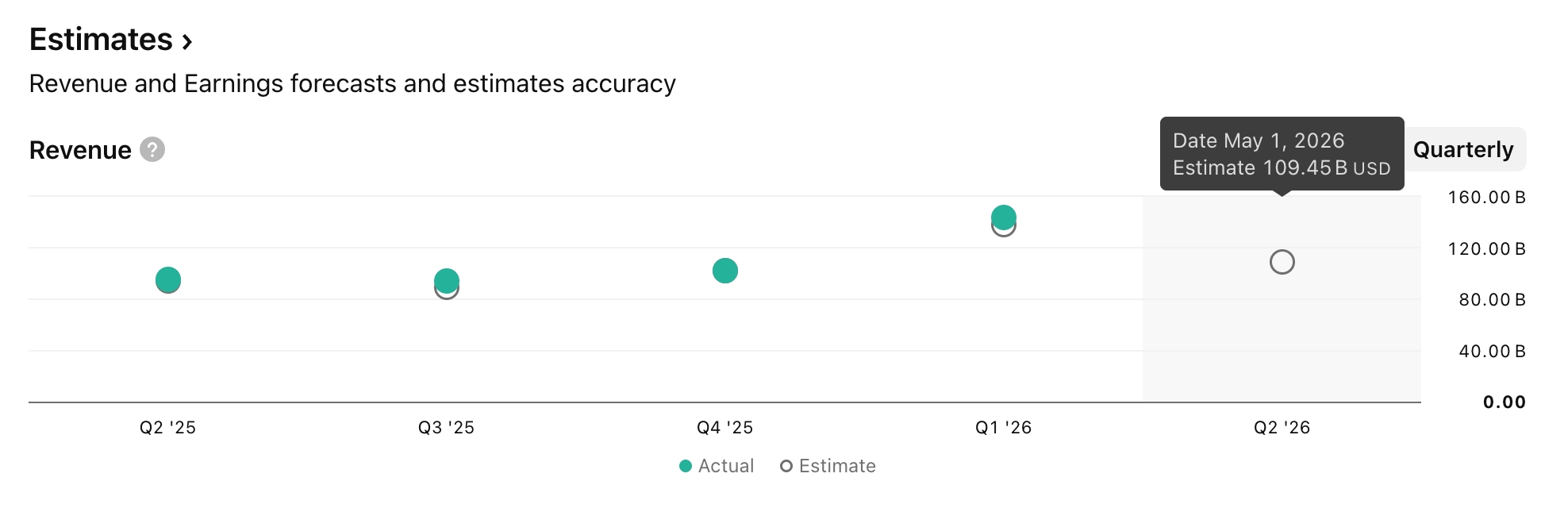

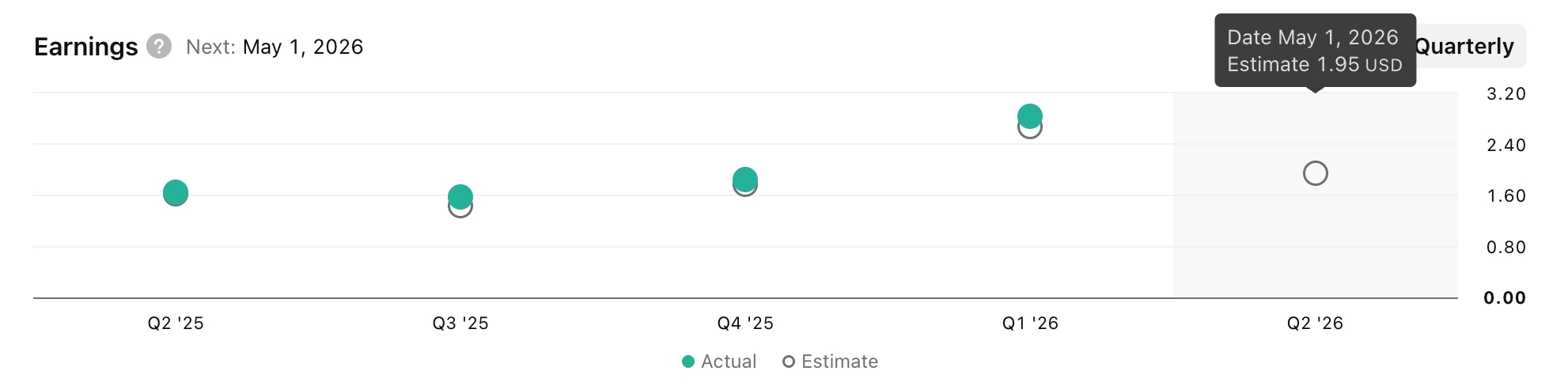

For Apple's second fiscal quarter, consensus market expectations have become clear. Wall Street generally expects Q2 revenue to be approximately $109.5 billion, up about 15% year-over-year, with earnings per share of $1.95. Although down sequentially, the year-over-year growth remains substantial.

By segment, the iPhone is expected to remain the primary revenue driver, with Goldman Sachs forecasting revenue of $56.3 billion; the services business is likely to maintain a 14% growth rate, consistent with Q1; Mac revenue is projected to be flat year-over-year, but the MacBook Neo launched in March could be a "small surprise" in the earnings report.

Dual Sales Growth in China and the US Builds a Robust Product Moat

The primary highlight of this earnings report is the iPhone, which accounts for over half of Apple's revenue. According to data disclosed so far, the iPhone 17 demonstrated a dual-market success in both China and the U.S. during Q2.

Data from Counterpoint indicates that during the first nine weeks of 2026 in the Chinese market, the overall Chinese smartphone market contracted by approximately 4% year-over-year, yet Apple's iPhone sales surged by about 23% against the trend.

Analysis points out that Apple's ability to expand against the trend amidst the contraction of the Chinese market can be attributed to three factors:

Demand for consumer electronics spurred by Chinese subsidy policies has placed the iPhone 17 precisely within the sweet spot of consumer acceptance.

Furthermore, Apple secured lower costs than its competitors by signing long-term supply agreements ahead of partners such as Samsung, thereby avoiding price increases.

At the same time, Apple's high-end models have larger profit margins, enabling the company to absorb some of the upward pressure on costs.

In the U.S. market, demand for high-end models is equally robust. Trade-in subsidies provided by carriers have made the Pro Max more accessible, while the high-margin iPhone 17 Pro series is supporting Apple's revenue and profit resilience.

Cost Pressures and Tariffs: Profit Margins Under Pressure

While revenue growth is expected, the cost pressures facing the iPhone are under close market scrutiny. Earlier this year, UBS described memory costs as a "Sword of Damocles" hanging over Apple.

UBS warned that while Apple successfully avoided cost shocks in the December 2025 quarter through pre-emptive price locking and production deployment, gross margins for the June and September quarters may face 50 to 100 basis points of downward pressure as production for the next-generation iPhone peaks. UBS thus expressed concern regarding the company's gross margin guidance of 48.0% and 47.8% for the June and September quarters, respectively.

Goldman Sachs provided a starkly different assessment, contending that the market is "overly pessimistic" about Apple. The firm noted that Apple has a stronger capacity to absorb challenges than its peers, stating, "Given Apple's relatively strong market position, we believe current market concerns appear overly pessimistic."

Notably, the iPhone's "growth against the trend" in China provides some support for this perspective. As competitors were forced to hike prices, Apple kept its pricing stable, an advantage that allowed Apple to passively capture more market share. Whether Apple can sustain this advantage in the coming quarters depends largely on the duration of its pre-emptive price-locking strategy.

The Road to AI Catch-up and CEO Turnover

In the AI space, Apple has transitioned from "developing behind closed doors" to "leveraging external partnerships." In January 2026, Apple reached a multi-year strategic AI partnership with Google, where Google's Gemini model will be embedded into the Apple Intelligence system to provide underlying language model support for Siri. This collaboration signals Apple's move to abandon its fully proprietary AI tech stack in exchange for an accelerated product rollout schedule. HSBC Research believes that Apple Intelligence still needs time to prove its actual contribution to revenue.

For Apple, the June WWDC will be the year's most significant AI narrative milestone. At the event, Apple will need to demonstrate what the "concrete implementation of its AI strategy" looks like, including the new Siri's interactive experience, the Apple Intelligence feature matrix, and the developer integration ecosystem.

The market focus is on whether Apple's AI narrative can translate into actual demand for device upgrades. Wedbush analyst Dan Ives previously labeled 2026 as "the year Apple finally enters the AI race."

Meanwhile, the CEO transition is the second major narrative beyond the earnings report. Cook has announced that he will step down as CEO on September 1, with John Ternus, Senior Vice President of Hardware Engineering, set to take over. HSBC Research suggests that whether a successor with a technical background can identify the next hardware breakthrough after the iPhone 17 will be a primary focus for ongoing investor evaluation.

Recommended Articles