Lam Research Corp Stock (LRCX) Moved Down by 4.38% on Jun 26: A Full Analysis

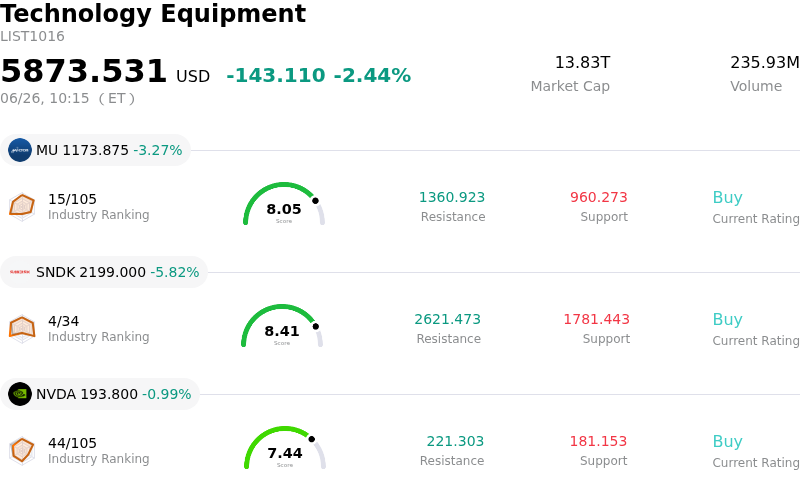

Lam Research Corp (LRCX) moved down by 4.38%. The Technology Equipment sector is down by 2.44%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 3.27%; SanDisk Corporation (SNDK) down 5.82%; NVIDIA Corp (NVDA) down 0.99%.

What is driving Lam Research Corp (LRCX)’s stock price down today?

The notable decline in Lam Research shares reflects a broader technology and semiconductor sector sell-off as investors reassess high valuations across the artificial intelligence value chain. While optimistic forward guidance from industry peers initially boosted the sector, the rally quickly faded. Market participants have grown increasingly concerned about the massive capital expenditures required for AI infrastructure and whether consumer technology giants can monetize these investments quickly enough. As downstream companies adjust prices to counter rising chip and memory costs, the market has adopted a more cautious stance, triggering profit-taking across the entire chip-equipment landscape.

As a global leader in wafer fabrication equipment, Lam Research is uniquely exposed to changes in memory and logic chip capital commitments. The company’s advanced etch and deposition systems are essential for producing next-generation semiconductors and high-bandwidth memory. However, this high concentration in memory capex makes the stock highly sensitive to cyclical shifts. Signs of a potential near-term cooling in capital commitments, combined with a decline in customer down payments, have led investors to temper their expectations, putting downward pressure on the stock despite its strong underlying market position.

The correction is further exacerbated by technical and sentiment-driven factors. Following an extraordinary year-to-date rally, the company's valuation multiples had stretched significantly above historical averages, leaving little margin of safety. Recent disclosures of insider selling at elevated price levels have also weighed on retail and institutional investor confidence. During periods of sector-wide rotation out of high-multiple growth stocks, institutional investors frequently trim positions to secure gains, contributing to increased intraday volatility for top-tier equipment suppliers like Lam Research.

Despite the short-term pullback, the structural drivers for the company remain solid. Lam Research recently updated its wafer fabrication equipment industry outlook upward, driven by long-term demand for advanced packaging and high-aspect-ratio etching. Wall Street analysts generally maintain a favorable view of the company’s strong balance sheet, high-margin service revenue, and central role in the AI hardware buildout. Today’s downward movement represents a valuation reset and short-term de-risking in a volatile macroeconomic environment rather than a fundamental decay in the company's operational strength.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 4.260, indicating a buy signal. The RSI at 64.738 suggests neutral condition and the Williams %R at 7.411 suggests overbought condition. Please monitor closely.

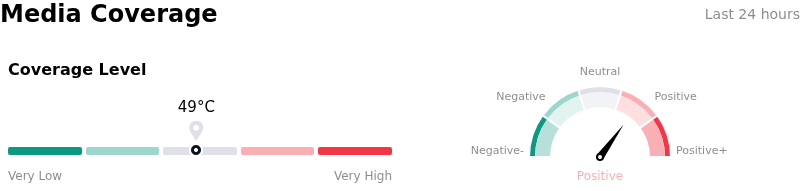

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $337.58, a high of $480.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Direct Exposure to Customer Capacity Reallocations (SK Hynix): SK Hynix's announcement on June 23, 2026, to slow advanced AI chip (HBM and advanced NAND) production in favor of commodity DRAM directly compresses Lam's order outlook. Commodity chip manufacturing requires significantly fewer process steps and lower equipment intensity for deposition and etching per wafer, reducing the revenue potential of Lam's installed base.

- Severe Deceleration in Shipment Growth and Falling Down Payments: Driven by cyclical cooling in both 3D NAND and mature-logic nodes, institutional analysts have flagged a drastic projected drop in system shipment growth to just 3% in 2026 (down from 82% in 2025). This structural slowdown is compounded by falling customer down payments, indicating a near-term cooling of customer capital commitments.

- Geopolitical Risk and High China Revenue Concentration: China accounts for a substantial 34% to 35% of Lam's total revenue. This high concentration leaves the company highly exposed to expanding US export control regulations that limit advanced wafer-fabrication equipment sales to Chinese fabs, compounding the impact of moderating domestic investments in the region.

- Valuation Compression and Significant Insider Divestments: Following a year-to-date surge that pushed Lam's trailing P/E ratio past 69x, the stock's sharp ~10% drop on June 23, 2026, highlighted extreme susceptibility to multiple compression. This volatility is further exacerbated by recent Form 4 filings disclosing material insider liquidations, including a $19.1 million divestment by Director Eric Brandt (a 21.48% decrease in direct holdings) and an 11.58% position reduction by SVP Neil J. Fernandes.

Recommended Articles