SpaceX Is the Most Expensive Stock in the $2 Trillion Club, and It's Not Even Close

Key Points

Seven publicly traded companies currently have valuations of $2 trillion or more, and SpaceX is the newest member of that exclusive club.

SpaceX operates in the space transportation, satellite internet connectivity, and artificial intelligence industries.

- 10 stocks we like better than Space Exploration Technologies ›

Space Exploration Technologies (NASDAQ: SPCX), better known as SpaceX, went public on Friday, and by Monday's close, it had already rocketed higher by 28% from its first day opening price of $150. The company now has a market capitalization of well over $2 trillion, joining Nvidia, Alphabet, Apple, Microsoft, Amazon, and Taiwan Semiconductor Manufacturing in that exclusive club.

SpaceX has a unique business that includes operations in space transportation, satellite internet connectivity, and artificial intelligence (AI) infrastructure, and its revenue is forecast to soar over the next couple of years. However, its stock is substantially more expensive than each of its peers in the $2 trillion club, which creates an uncomfortable risk vs. reward situation for investors.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: The Motley Fool.

SpaceX is tackling a huge addressable market

SpaceX is best known for developing the world's first reusable rockets, which have reduced the cost of traveling to space by over 90%. The company's Falcon 9 and Falcon Heavy rockets deliver commercial payloads into orbit on behalf of its enterprise customers, and it already owns 80% of this market. Its Starship rocket will soon begin commercial flights, and with four times the payload capacity of Falcon 9, it could generate significantly more income per trip.

SpaceX has also launched more than 9,600 of its own satellites into orbit, which make up the infrastructure layer of its Starlink internet service. Starlink had over 10.3 million paying subscribers as of March 31, which was more than twice as many as it had at the same time last year. The company will soon start deploying its V3 satellites, which provide up to 1,024 gigabytes of bandwidth, representing a tenfold increase over the current V2 satellites.

These new satellites could attract demand from a wider group of potential customers, boosting SpaceX's connectivity business, which was already responsible for over 60% of the company's total revenue last year.

Finally, there is the AI business, which SpaceX effectively acquired when it bought Elon Musk's xAI in an all-stock deal earlier this year. The company now operates data centers like Colossus and Colossus II, which it uses to develop AI models, but it also rents spare computing capacity to other companies like Anthropic and Alphabet, which is a lucrative business model.

Anthropic could spend $1.25 billion per month to lease data center capacity from SpaceX going forward, and Alphabet could be spending up to $920 million per month starting this October.

All three of SpaceX's core businesses have enormous addressable markets, but the company believes AI is the most valuable by far:

|

SpaceX Segment |

Total Addressable Market |

|---|---|

|

Space |

$370 billion |

|

Connectivity |

$1.6 trillion |

|

AI |

$26.5 trillion |

|

Total |

$28.5 trillion |

Data source: SpaceX IPO roadshow presentation.

SpaceX could triple its current revenue in 2027, but those gains might already be priced in

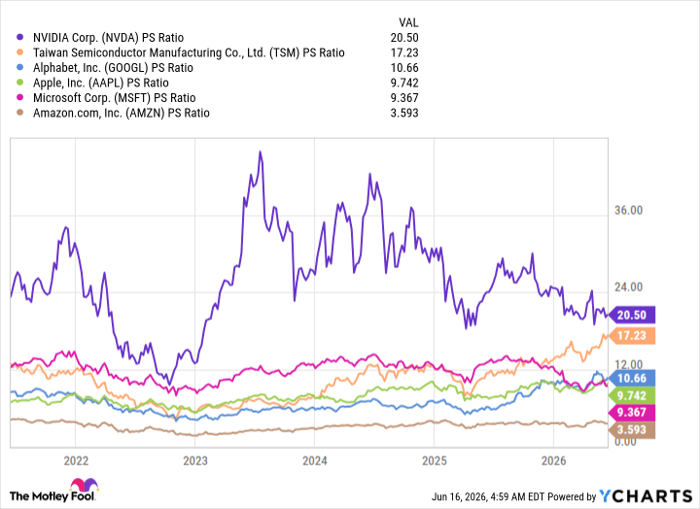

SpaceX generated $19.3 billion in total revenue over the last four quarters, so based on the company's market capitalization of $2.5 trillion as of the close on Monday, its stock traded at a price-to-sales (P/S) ratio of 129.5.

The other six stocks in the $2 trillion club have an average P/S ratio of just 11.8, which makes SpaceX a whopping 11 times as expensive as the group.

NVDA PS Ratio data by YCharts.

With that said, Wall Street predicts SpaceX will more than triple its revenue to $64.5 billion in 2027, so investors are pricing in some of that potential growth today. But I would argue they might be going too far, because even if we assume the company will hit the Street's target, its forward P/S ratio is still 38.7.

In other words, even if SpaceX stock doesn't rise any further, it would still be materially more expensive than any of its peers in the $2 trillion club 18 months from now. If the company happens to produce less revenue than anticipated next year than Wall Street expects, then its stock could suffer a sharp correction.

In my opinion, that doesn't leave investors with a very attractive risk vs. reward proposition, so this stock might not be the greatest buy right now.

Should you buy stock in Space Exploration Technologies right now?

Before you buy stock in Space Exploration Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Space Exploration Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $424,531!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,273,016!*

Now, it’s worth noting Stock Advisor’s total average return is 940% — a market-crushing outperformance compared to 209% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 18, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Recommended Articles