These 4 Core Artificial Intelligence (AI) Hyperscalers Are Screaming Buys Today

Key Points

All four artificial intelligence (AI) hyperscalers have a strong-enough core business to fund most of their data center build-outs.

Amazon, Microsoft, and Alphabet are seeing this spending pay off.

There are still questions surrounding Meta Platforms' spending.

- These 10 stocks could mint the next wave of millionaires ›

Artificial intelligence (AI) hyperscalers are among the most popular investments today. The big four are also the ones often quoted as spending the most on data center capital expenditures. However, other pure plays like OpenAI and Anthropic would add a significant amount to this total if included.

The four major AI hyperscalers are Microsoft (NASDAQ: MSFT), Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL), Amazon (NASDAQ: AMZN), and Meta Platforms (NASDAQ: META). Each company is spending hundreds of billions of dollars on data center capital expenditures this year to meet AI demand.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Despite their huge spending bills, I think each looks like a solid investment right now.

Furthermore, these four also have core businesses that allow them to self-fund most of their spending. I think all four companies are solid, long-term investments and will make investors a lot of money if AI can be monetized effectively over the next decade.

Image source: Getty Images.

Four core businesses help fund AI aspirations

For Microsoft, its core business is business productivity software. Its business has the closest tie to AI, as these tools can be integrated into Microsoft's core offerings and, through Azure, its cloud computing platform.

In fact, Microsoft's AI business has an annual run rate of $37 billion, growing at a 123% pace. Azure grew revenue by 40%, demonstrating strong demand for its computing capabilities. With growth rates like that, it justifies Microsoft's heavy spending on data centers to sustain it, and Microsoft will be a force to be reckoned with in the AI realm for a while.

Amazon's commerce business is solid, but it really has no direct tie to its broader AI build-out. Instead, Amazon Web Services (AWS) is spending all of the money.

However, investors should probably think of Amazon more as a computing company that happens to do commerce. In the first quarter, AWS accounted for 59% of Amazon's operating profits, making it the company's primary profit driver. While Amazon's commerce business can still benefit from its AI improvements, AWS is the primary beneficiary. AWS grew revenue at a 29% clip in Q1 -- its best mark in nearly four years.

Amazon is also spending the most on capital expenditures this year, with expected spending of $200 billion. However, if Amazon can continue to accelerate AWS's growth rate, it will be worth it in the end.

Alphabet's primary business is advertising, with Google Search being its cash cow. Alphabet is also pushing its own AI model, Gemini, and has integrated that into its core search business. However, its Google Cloud business is growing faster than AWS and Azure, rising 63% in Q1.

If Alphabet can maintain that growth rate over the next few years, it will be well positioned to take the company to new heights. If Gemini can also become a go-to AI model, it will likely place additional workload on Google Cloud's servers, further benefiting the company.

The odd company out in this group is Meta Platforms. Its primary business is advertising on its social media platforms, including Facebook, Instagram, Threads, and WhatsApp. Advertising accounts for nearly all of Meta's revenue.

While Meta has incorporated several AI tools in its advertising platform, it really has no true AI revenue stream like the other three. Meta has considered launching a cloud computing business but is currently using all of its available compute internally.

Meta has several products in the pipeline, such as AI glasses and a personal superintelligence model, but none of these have been released to date, and there's no guarantee they will pan out. As a result, the market is a bit more skeptical of Meta's AI spending. However, that's what makes it the best deal of the four.

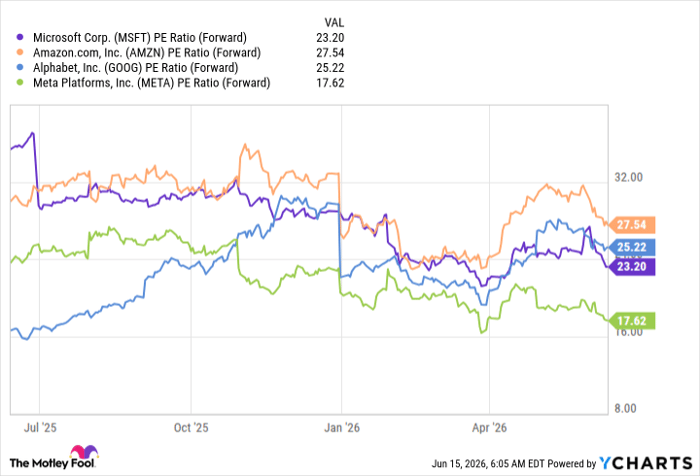

The AI hyperscalers range from pricey to cheap

Because all four companies are growing relatively quickly, forward earnings are the best tool for assessing them. From this standpoint, Meta Platforms is the cheapest, but it's likely because it's spending heavily without a ton to show for it. Meanwhile, Amazon is the most expensive because it has strong growth prospects and probably the most resilient core business.

MSFT PE Ratio (Forward) data by YCharts

All these stocks really aren't that terribly priced for their growth rates. If AI can deliver meaningful contributions across all four companies, then the stocks are strong buys here.

I think investors are already seeing the benefit in three of them, with Alphabet, Microsoft, and Amazon having strong cloud computing offerings. Meta is still working on its AI product, and if it delivers, it will have a huge upside, too.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $538,621!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $57,033!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $424,531!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

See the 3 stocks »

*Stock Advisor returns as of June 18, 2026.

Keithen Drury has positions in Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool has a disclosure policy.

Recommended Articles