Canada CPI is expected to jump in March amid higher energy prices

- The Canadian Consumer Price Index is seen accelerating 1.1% in March following a 0.5% increase in February.

- The yearly CPI inflation is expected to have jumped to 2.5%, above the BoC’s target

- The Canadian Dollar maintains a positive tone against the US Dollar in April.

Canada’s economic docket opens on Monday with the key Consumer Price Index (CPI) figures for March, which will be closely watched to gauge the inflationary impact of the war in Iran. The data, released by Statistics Canada, is likely to confirm a significant increase in price pressures, driven by higher energy costs.

Market analysts foresee the monthly CPI accelerating 1.1%, more than twice the 0.5% reading seen before the war started in February. Meanwhile, on an annual basis, the CPI is expected to have grown at a 2.5% year-on-year (YoY) rate, from 1.8% in the previous month.

The sharp increase in Oil and Gas prices, due to the blockade of the Strait of Hormuz, would have been the main driver of higher inflationary figures. However, the core inflation, which strips the influence of energy and food prices, is seen fairly steady, rising 0.3% in March, compared to 0.4% in the previous month, and ticking up to 2.4% from 2.3% year-on-year.

These figures are likely to raise some eyebrows at the Bank of Canada’s (BoC) monetary policy committee, and, highly likely, bring the possibility of a rate hike back to the table. The BoC has lowered interest rates by 2.75% over the last two years.

What can we expect from Canada’s inflation rate?

Canada’s central bank left its benchmark interest rate unchanged, at 2.25%, at its March 18 meeting, but the monetary policy statement already warned about “increased volatility in global energy prices and financial markets, and heightened the risks to the global economy", stemming from the US-Iran war.

Inflation data for March will corroborate those fears. As previously stated, headline CPI inflation is expected to rise to 2.5% while core inflation would pick up to 2.4%, in both cases significantly above the central bank’s 2% inflation target.

These figures will definitely raise market speculation about monetary tightening, although the broader macroeconomic picture clouds the bank’s monetary policy stance. The Canadian economy contracted by 0.2% in the last quarter of 2025, and the monthly Gross Domestic Product (GDP) showed a meagre 0.1% growth in January. Ivey Purchasing Managers’ Index (PMI) data from March revealed that business activity contracted for the first time since November, hinting at a soft end of the quarter.

In this context, BoC policymakers are likely to think twice before hiking interest rates too early, as it might damage an already frail growth, tipping the economy into a recession. ING’s analyst Francesco Pesole points out: "Markets are pricing around 40bp of tightening by December, which looks too aggressive considering the BoC has not signalled much appetite for hikes, and attention may soon shift to USMCA renegotiations – a major downside risk for Canada’s activity and jobs."

When is the Canada CPI data due, and how could it affect USD/CAD?

Canada’s Consumer Price Index figures for March will be released by Statistics Canada on Monday at 12:30 GMT. Higher inflation figures, when they are driven by stronger economic activity and a tight labour market, tend to have a positive impact on the currency. This time, however, the scenario is somewhat different.

Canadian economic growth remains sluggish, weighed down by the higher tariffs from the US, its main trading partner. With this in mind, a sharp increase in inflation will create a headache for the Bank of Canada, which will have to choose between supporting economic growth and combating inflation, and might hurt the Loonie.

All things considered, a strong CPI is likely to raise concerns about stagflation and put the Canadian Dollar under pressure. In the current scenario, the CAD would be favoured by softer-than-expected inflation figures, which would buy some time for the Bank of Canada to wait for additional data before deciding its next monetary policy steps.

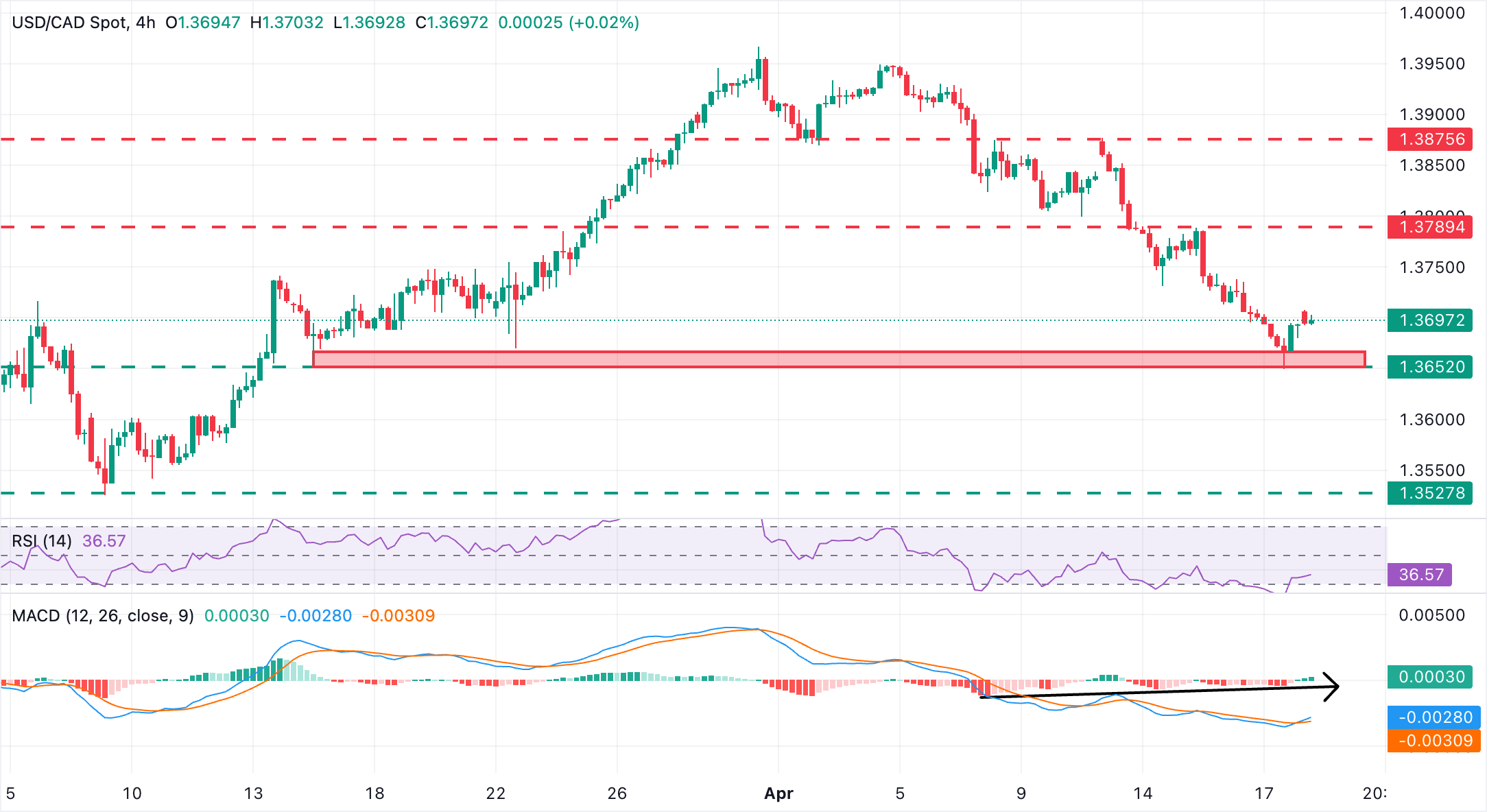

Regarding the USD/CAD, Guillermo Alcala, FX Analyst at FXStreet, observes the pair’s downward trend since early April, rather due to the US Dollar’s weakness, amid investors’ optimism about a resolution of the Middle East conflict, than to any intrinsic Canadian Dollar strength.

“Canadian Dollar bulls are focusing on the area between 1.3650 and 1.3670, where the USD/CAD found support last week and also on March 16 and 23, before the March 9 low at 1.3525”. Alcalá, however, warns about technical indicators: “The overbought levels in the 4-hour Relative StrengthIndex (RSI) and some bearish divergence in the Moving Average Convergence Divergence (MACD) histogram suggest that a corrective reaction might be ahead.”

On the upside, Alcalá sees the “1.3735 area (April 14 low) as immediate resistance, ahead of the April 15 high, right below 1.3790, and the April 13 highs around 1.3875.”

Economic Indicator

BoC Consumer Price Index Core (YoY)

The BoC Consumer Price Index Core, released by the Bank of Canada (BoC) on a monthly basis, represents changes in prices for Canadian consumers by comparing the cost of a fixed basket of goods and services. It is considered a measure of underlying inflation as it excludes eight of the most-volatile components: fruits, vegetables, gasoline, fuel oil, natural gas, mortgage interest, intercity transportation and tobacco products. The YoY reading compares prices in the reference month to the same month a year earlier. Generally, a high reading is seen as bullish for the Canadian Dollar (CAD), while a low reading is seen as bearish.

Read more.Next release: Mon Apr 20, 2026 12:30

Frequency: Monthly

Consensus: -

Previous: 2.3%

Source: Statistics Canada

Bank of Canada FAQs

The Bank of Canada (BoC), based in Ottawa, is the institution that sets interest rates and manages monetary policy for Canada. It does so at eight scheduled meetings a year and ad hoc emergency meetings that are held as required. The BoC primary mandate is to maintain price stability, which means keeping inflation at between 1-3%. Its main tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will usually result in a stronger Canadian Dollar (CAD) and vice versa. Other tools used include quantitative easing and tightening.

In extreme situations, the Bank of Canada can enact a policy tool called Quantitative Easing. QE is the process by which the BoC prints Canadian Dollars for the purpose of buying assets – usually government or corporate bonds – from financial institutions. QE usually results in a weaker CAD. QE is a last resort when simply lowering interest rates is unlikely to achieve the objective of price stability. The Bank of Canada used the measure during the Great Financial Crisis of 2009-11 when credit froze after banks lost faith in each other’s ability to repay debts.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the Bank of Canada purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the BoC stops buying more assets, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive (or bullish) for the Canadian Dollar.

추천 기사