Mexican Peso trims some of Banxico-related losses following interest-rate cut

- The Mexican peso edges up slightly, recovering some of the previous day’s losses.

- Banxico cuts rates while the Fed remains cautious, highlighting a contrasting economic outlook that doesn’t bode well for the Peso.

- USD/MXN edges down as traders anticipate US Michigan Sentiment data, with inflation expectations and consumer confidence in focus.

The Mexican peso (MXN) is consolidating against the US dollar (USD) on Friday after recovering some of the ground lost on Thursday after the Banco de Mexico (Banxico) decided to cut interest rates, as expected.

At the time of writing, USD/MXN is trading near 19.485, down 0.04% on the day, as the pair pulls back slightly following Thursday’s rebound. Persistent trade-related uncertainty and diverging central bank policies remain key themes guiding price action.

Market participants await the preliminary release of the University of Michigan consumer sentiment data at 14:00 GMT, a key event risk that could influence near-term USD/MXN direction.

The United States will publish three closely watched indicators: the Consumer Sentiment Index, the Consumer Expectations Index, and the 1-year and 5-year Inflation Expectations for May. These measures offer timely insights into household confidence, perceived price pressures, and consumer behavior – critical inputs for shaping Federal Reserve (Fed) policy expectations.

Fed flags inflation risks from structural shocks

The Federal Reserve (Fed) has adopted a cautious stance in light of softening economic signals and persistent supply-side uncertainty. Speaking after the release of Thursday’s April data, Fed Chair Jerome Powell addressed the twin themes of slowing momentum and inflation risks.

The Producer Price Index (PPI) unexpectedly declined by 0.5% compared with the previous month –its steepest drop since 2009 –while retail sales rose by only 0.1%, suggesting subdued consumer demand.

During his opening speech at the Second Thomas Laubach Research Conference on Thursday, Powell noted, “The economy may be entering a period marked by more frequent and persistent supply shocks,” while adding that the central bank remains “attentive to signs of cooling demand” and that “inflation is moving in the right direction, though the path forward remains uncertain.”

While these developments may delay any shift toward policy easing, they also underscore the delicate balancing act the Fed faces as it monitors inflation and growth risks simultaneously.

Banxico rate cut underscores domestic slowdown

On the other side of the policy spectrum, Banxico delivered a 50 basis-point rate cut on Thursday as expected, lowering its benchmark interest rate to 8.5% in a unanimous decision. The move extended its easing cycle for a seventh straight meeting as the central bank seeks to stimulate a sluggish domestic economy. In its post-meeting statement, Banxico stated that:

“The Board estimates that looking ahead, it could continue calibrating the monetary policy stance and consider adjusting it in similar magnitudes. It anticipates that the inflationary environment will allow to continue the rate cutting cycle, albeit maintaining a restrictive stance.”

With Banxico signaling more easing and the Federal Reserve maintaining a cautious but steady tone, the policy divergence continues to favor the US Dollar. Still, USD/MXN remains vulnerable to headline-driven risk shifts, and the University of Michigan sentiment data could inject additional volatility. Trade policy developments and inflation expectations will also remain key drivers in shaping the near-term path for the Peso.

Mexican Peso daily digest: Banxico warns about trade risks to the economy

- The Banxico lowered its benchmark interest rate by 50 basis points to 8.5%. In the statement, the bank signaled that further similar cuts could be considered going forward.

- Banxico warned about the effects of the current trade standoff with the United States on the country’s economy. “The environment of uncertainty and trade tensions poses significant downward risks,” the bank said in its statement.

- Rising US-Mexico trade tensions threaten Mexico’s export-reliant economy, where over 80% of exports go to the US. Tariffs on goods such as steel and aluminium could disrupt supply chains, dampen investor sentiment, and weigh on growth.

- Concerns about the economic downturn have weighed in on Banxico. While inflation has picked up in recent months to 3.93% in April, the bank still expects inflation to return to its 3% target in the third quarter of 2026.

- The US has imposed 25% tariffs on certain Mexican imports not covered by the USMCA, citing security and drug enforcement concerns, adding further uncertainty to bilateral trade relations.

- According to Reuters, Mexico’s Economy Minister has proposed an early review of the USMCA, ahead of the 2026 timeline, to reassure investors and preserve the framework underpinning over $1.5 trillion in annual North American trade.

- The US economy contracted at an annualized rate of 0.3% in Q1, marking the first decline since 2022. This unexpected downturn was primarily driven by a surge in imports as businesses and consumers accelerated purchases ahead of new tariffs introduced by the Trump administration.

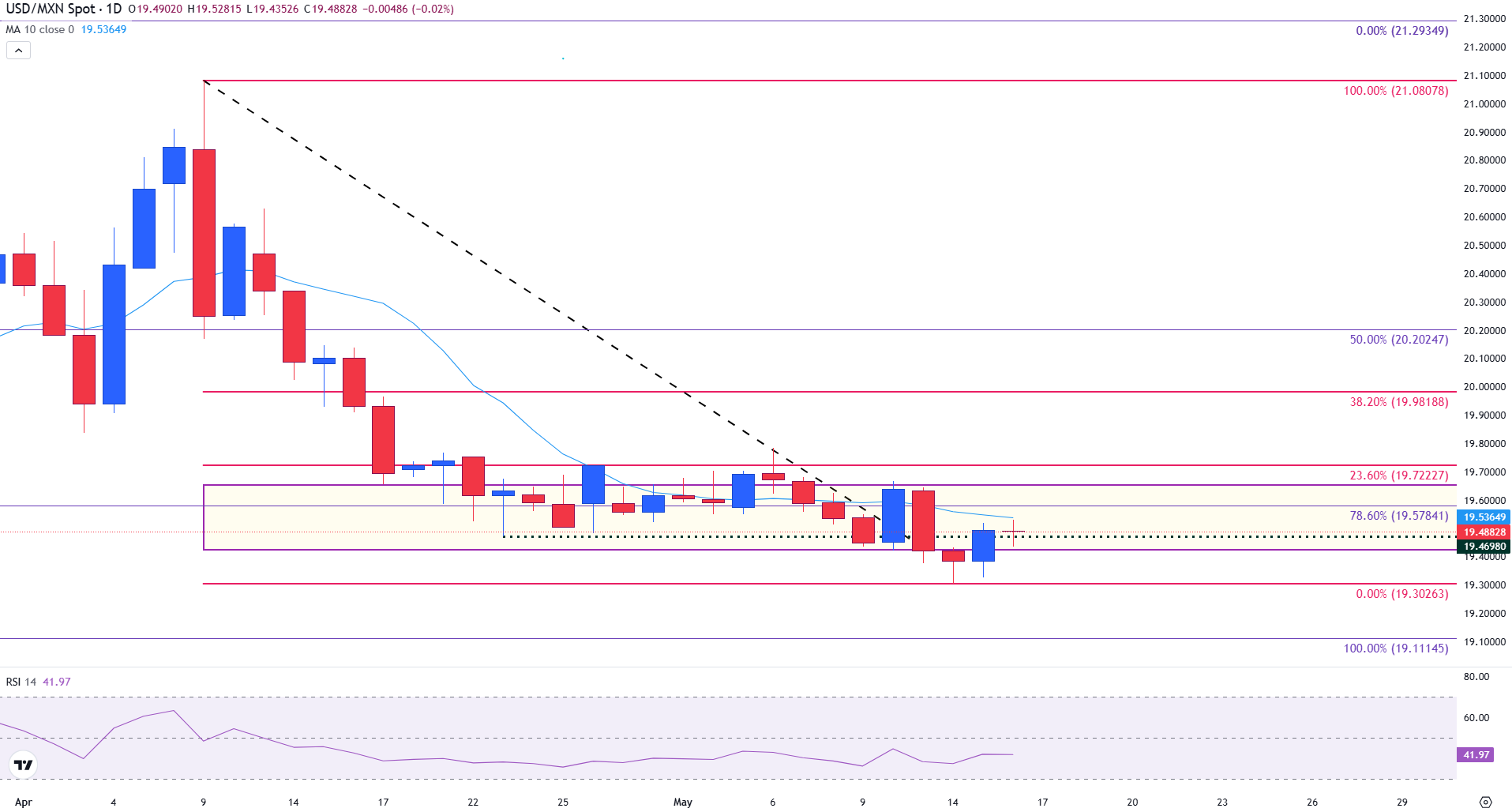

Technical Analysis: USD/MXN bearish consolidation signals further weakness

USD/MXN remains under pressure, extending its decline below the 78.6% Fibonacci retracement of the October to February rally at 19.57. The pair is currently trading around 19.45, having failed to reclaim the key psychological level of 19.50, with 19.40 acting as immediate resistance. This reinforces the prevailing bearish momentum and suggests sellers remain firmly in control.

The consolidation range highlighted in the yellow box has continued to contain price action over the past few weeks. However, repeated failures to break higher and the prevailing downtrend signal that a bearish continuation remains likely. This technical setup is in line with persistent downside pressure, as the pair struggles to gain traction above its short-term moving averages.

The next major support lies near the October low at 19.11, a critical level that could serve as a medium-term target if bearish momentum persists. A break below this area would open the door to further losses, potentially exposing the psychological 19.00 level.

On the upside, initial resistance is seen at 19.40, followed by the 78.6% Fibonacci retracement at 19.57. A sustained break above this zone could mark the beginning of a shift in sentiment, bringing the psychological 19.60 area back into focus.

USD/MXN daily chart

The 10-day Simple Moving Average (SMA), currently at 19.53, continues to act as dynamic resistance, repeatedly capping upside attempts. Meanwhile, the Relative Strength Index (RSI) stands at around 40, indicating mild bearish momentum. Although not yet in oversold territory, the RSI suggests there is room for additional downside before a technically driven rebound becomes more probable.

Risk sentiment FAQs

In the world of financial jargon the two widely used terms “risk-on” and “risk off'' refer to the level of risk that investors are willing to stomach during the period referenced. In a “risk-on” market, investors are optimistic about the future and more willing to buy risky assets. In a “risk-off” market investors start to ‘play it safe’ because they are worried about the future, and therefore buy less risky assets that are more certain of bringing a return, even if it is relatively modest.

Typically, during periods of “risk-on”, stock markets will rise, most commodities – except Gold – will also gain in value, since they benefit from a positive growth outlook. The currencies of nations that are heavy commodity exporters strengthen because of increased demand, and Cryptocurrencies rise. In a “risk-off” market, Bonds go up – especially major government Bonds – Gold shines, and safe-haven currencies such as the Japanese Yen, Swiss Franc and US Dollar all benefit.

The Australian Dollar (AUD), the Canadian Dollar (CAD), the New Zealand Dollar (NZD) and minor FX like the Ruble (RUB) and the South African Rand (ZAR), all tend to rise in markets that are “risk-on”. This is because the economies of these currencies are heavily reliant on commodity exports for growth, and commodities tend to rise in price during risk-on periods. This is because investors foresee greater demand for raw materials in the future due to heightened economic activity.

The major currencies that tend to rise during periods of “risk-off” are the US Dollar (USD), the Japanese Yen (JPY) and the Swiss Franc (CHF). The US Dollar, because it is the world’s reserve currency, and because in times of crisis investors buy US government debt, which is seen as safe because the largest economy in the world is unlikely to default. The Yen, from increased demand for Japanese government bonds, because a high proportion are held by domestic investors who are unlikely to dump them – even in a crisis. The Swiss Franc, because strict Swiss banking laws offer investors enhanced capital protection.

추천 기사