Jensen Huang Just Named Marvell the Next $1 Trillion Stock. Is the Stock a Buy Following a 129% Surge?

Key Points

Marvell Technology is benefiting from a couple of solid growth opportunities in the AI infrastructure space.

The company may be underestimating its growth potential, as the demand for custom AI processors and networking chips is poised to rise rapidly.

Marvell has become expensive following its recent rally, but it can justify its valuation by delivering better-than-expected growth.

- 10 stocks we like better than Marvell Technology ›

Marvell Technology (NASDAQ: MRVL) stock has witnessed a phenomenal surge lately, rising an incredible 129% over the past three months, as investors have taken cognizance of the company's growing prominence in the artificial intelligence (AI) infrastructure space.

Marvell stock got a big boost recently after Nvidia CEO Jensen Huang remarked that the chip designer could be the next one to join the trillion-dollar market cap club. Investors, however, may be wondering if it is a good idea to buy this semiconductor stock following its parabolic jump.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Let's take a closer look at Marvell's business and see if it can indeed live up to Huang's prophecy and become a multibagger in the future.

Image source: The Motley Fool.

Marvell Technology is capitalizing on two sizzling growth opportunities in AI infrastructure

Marvell designs custom chips, known as application-specific integrated circuits (ASICs), to perform specific tasks. These custom chips have witnessed a phenomenal surge in demand due to their deployment in AI data centers. Goldman Sachs estimates that custom ASIC shipments could equal sales of graphics processing units (GPUs) by next year.

That's not surprising, as custom ASICs are ideal for running AI inference workloads since they are designed to perform specific tasks. As a result, these chips are not as complex as general-purpose computing chips like GPUs, and they can perform the specific task they are designed for more efficiently.

Hyperscalers and AI companies have been ramping up the deployment of custom ASICs. Marvell noted in May that its custom chip revenue could more than double in the next fiscal year, driven by both new and existing customers. For comparison, the company anticipates its custom ASIC revenue will increase by just 20% in the current fiscal year.

Importantly, this isn't the only AI infrastructure opportunity powering Marvell's growth. The company also sells optical networking products, the demand for which is substantially outpacing supply. Optical networking is emerging as a key bottleneck in AI data centers, as it helps transport large data sets quickly across AI data centers and chip clusters, so that accelerators such as GPUs and ASICs don't sit idle.

In fact, Goldman Sachs is expecting a whopping 9x increase in sales of optical networking components in just two years. That's the reason why Marvell's data center interconnect and switching business is growing rapidly. The company expects a 70% increase in its interconnect business this year, while the switching business is anticipated to generate $1 billion in revenue in fiscal 2028, up from $600 million this year.

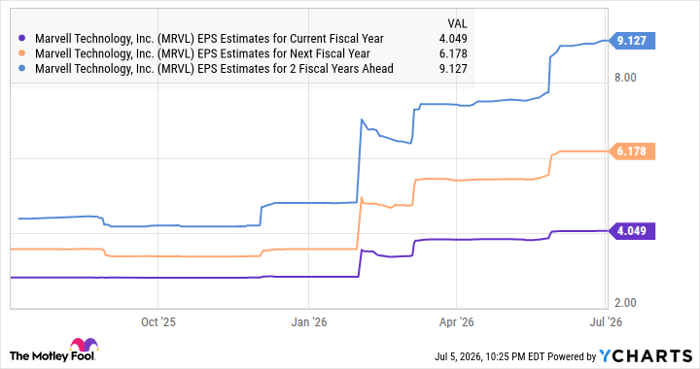

These healthy growth rates explain why analysts have been raising their earnings expectations from Marvell.

Data by YCharts

The company's earnings are projected to increase by 43% in the current fiscal year, and the chart above clearly suggests it is on track to sustain strong growth over the next couple of years. What's worth noting is that Marvell sees its data center total addressable market (TAM) reaching $94 billion in 2028, driven by growing demand for custom chips, switching, and interconnect solutions.

The company believes it can capture 20% of this market in 2028, translating into almost $19 billion in data center revenue. That will be more than 3x Marvell's fiscal 2026 data center revenue of $6.1 billion. However, Marvell may be underestimating its potential opportunity. Goldman Sachs notes that the optical networking market could reach a whopping $154 billion due to AI.

Market research provider Oplexa Insights estimates that the custom AI market could generate a massive $600 billion in revenue in 2033. As a result, Marvell could sustain its outstanding growth rates for a long time to come, powered by the huge investments in AI data centers.

The stock has become expensive following its parabolic jump

Marvell trades at a significant premium right now. It has a trailing earnings multiple of 94. The forward earnings multiple of 67, though lower, is still on the expensive side. Meanwhile, its price-to-sales ratio of 27 isn't cheap either.

However, Nvidia CEO Jensen Huang's prediction suggests the stock could jump almost 5x from current levels, given its $215 billion market cap as of this writing. To achieve that, Marvell will have to keep growing at a tremendous pace over the coming years. The good news is that the company seems capable of doing so, given the huge addressable opportunity it is sitting on.

Also, the market share gains Marvell is projecting from its expanding clientele could eventually justify its valuation and allow it to soar higher. That's why growth-oriented investors with a strong risk appetite can consider buying this AI stock following its recent surge. In contrast, those seeking a cheaper custom AI chip and networking play can consider this name to capitalize on this fast-growing AI infrastructure niche.

Should you buy stock in Marvell Technology right now?

Before you buy stock in Marvell Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Marvell Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $418,761!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,195,804!*

Now, it’s worth noting Stock Advisor’s total average return is 918% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 6, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Goldman Sachs Group, Marvell Technology, and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles