TradingKey Daily Market Briefing: AI Chip Stocks Pull Back, Micron Falls Over 6%, June Non-Farm Payroll Data Becomes Market Focus

Tracking Market Trends

TradingKey - On June 26, Eastern Time, the three major U.S. stock indexes closed mixed. Tech stocks remained under pressure, and the semiconductor sector continued its correction, dragging the Nasdaq Composite down for its fifth consecutive trading day.

At the close, the Dow Jones Industrial Average fell 0.09% to 51,881.18 points; the S&P 500 Index ticked down 0.05% to 7,354.02 points; and the Nasdaq Composite Index fell 0.24% to 25,297.62 points. The Philadelphia Semiconductor Index fell over 5%, marking its largest weekly drop in over a year. AI chip stocks pulled back further, showing that market concerns over the return on AI capital expenditures are still simmering.

In terms of sectors and individual stocks, the semiconductor sector remained under pressure, with Nvidia ( NVDA ), AMD ( AMD ), Micron Technology ( MU) and other chip stocks generally trading lower. Micron, which had previously surged on its earnings report, saw profit-taking and fell over 6%. The healthcare sector stood out, with Moderna surging 12.59%, driving the broader biotech sector higher and helping the market narrow its losses. The energy sector performed weakly, weighed down by a pullback in international oil prices.

In the commodity markets, easing concerns over the Middle East situation saw WTI ( USOIL) crude fall below $70, hitting a recent low. Cooling expectations of an earlier Fed rate hike boosted gold's rebound, with spot gold ( XAUUSD) reclaiming around $4,060.

Market Headlines

This week, market focus will shift to the U.S. June non-farm payrolls report. Analysts expect non-farm payroll growth to slow compared to the previous reading, with the unemployment rate projected to remain around 4.3%. If the labor market continues to cool, it will strengthen market expectations for Federal Reserve rate cuts later this year. Conversely, if the employment data is unexpectedly strong, it could drive Treasury yields and the U.S. dollar higher, exerting fresh valuation pressure on growth and tech stocks.

Tensions between the United States and Iran continue to escalate. U.S. President Trump stated that if the conflict escalates further, Iran "might no longer exist." The U.S. military launched airstrikes in southern Iran for two consecutive days, while the Iranian military threatened to launch "hellish" attacks on U.S. bases and vowed to take a tougher stance on "non-compliant" vessels passing through the Strait of Hormuz. Affected by the strikes, Iran was absent from the technical talks between the U.S. and Iran originally scheduled for Sunday in Switzerland; the U.S. stated that both sides plan to resume talks on June 30 in Doha, the capital of Qatar.

New uncertainties emerge for the Lebanon-Israel ceasefire framework agreement. Following the tripartite framework agreement reached by Israel, Lebanon, and the U.S., Israeli Prime Minister Benjamin Netanyahu stated that the Israeli military will remain in the "security zone" of southern Lebanon until Hezbollah is disarmed. However, Hezbollah declared the agreement void, and the Israeli military subsequently continued airstrikes in southern Lebanon, claiming to have killed several Hezbollah militants and pledging to continue operations to eliminate security threats.

SpaceX to be included in the Nasdaq 100 Index on July 7. Nasdaq announced that SpaceX (SPCX) will be officially included in the Nasdaq 100 Index on July 7. The market believes this adjustment is expected to attract ETFs and passive funds tracking the Nasdaq 100 to allocate to SpaceX, potentially providing incremental capital support for its stock price in the short term, while further enhancing its market influence in the AI, aerospace, and technology sectors.

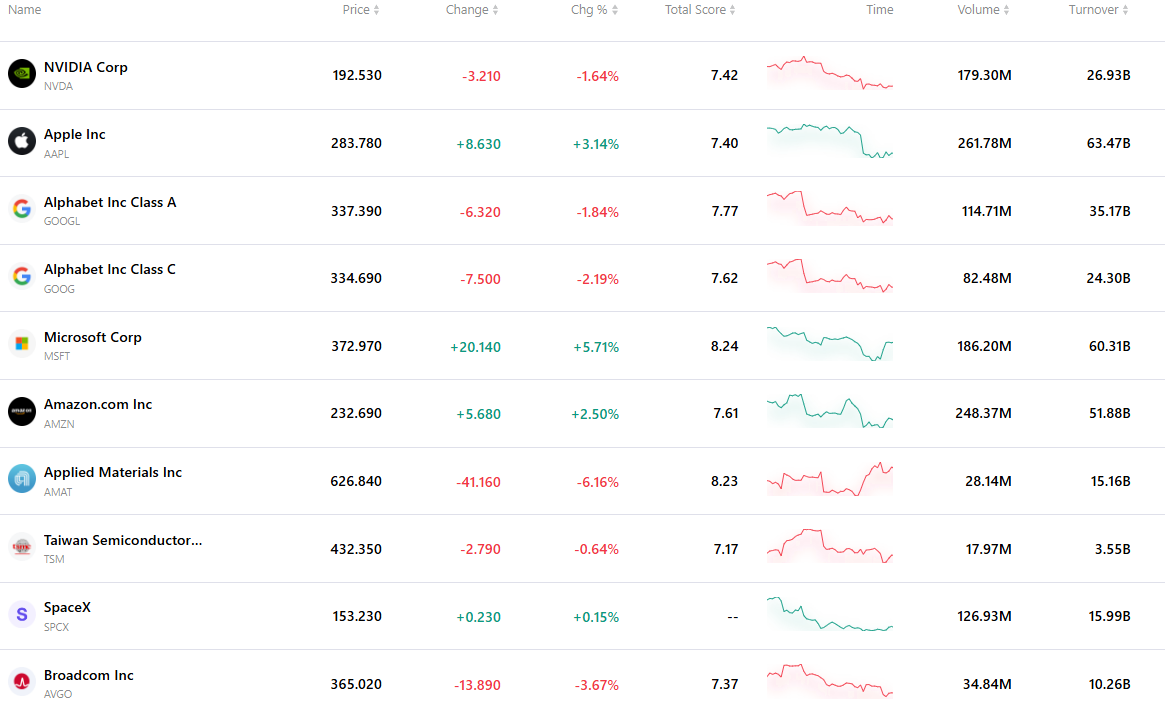

Top 10 most active stocks

The table below lists the ten most actively traded stocks in the market recently. Supported by massive trading volumes and excellent liquidity, these assets have become key benchmarks for tracking global market dynamics.

Recommended Articles