1 Glorious Growth Stock Down 84% to Buy on the Dip in June

Key Points

Docusign's digital agreement management tools kept thousands of businesses running at the height of the pandemic.

Demand for the company's products faded as social conditions began returning to normal in 2022, resulting in a steep sell-off in its stock.

Docusign now has a new platform that uses artificial intelligence to transform contract management processes, and it could turn the company's fortunes around.

- 10 stocks we like better than Docusign ›

Docusign (NASDAQ: DOCU) used to be known for its e-signature and digital contract management software that allowed thousands of businesses to continue making deals at the height of the pandemic, when lockdowns and social restrictions prevented travel. As a result, its stock soared to an all-time high of $310 in late 2021, a tenfold increase from its 2018 initial public offering (IPO) price of $29.

But demand cooled for Docusign's platform after 2022 as social conditions mostly returned to normal, causing a sharp slowdown in the company's revenue growth. Its stock now trades at just $48 as I write this, which is 84% below its 2021 peak.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

However, that might present an opportunity for long-term investors: In 2024 Docusign launched a new platform, powered by artificial intelligence (AI), called Intelligent Agreement Management (IAM), which completely transforms contract management processes for businesses. It's already experiencing strong demand, and it could be the bullish catalyst Docusign needs for a long-term turnaround.

Image source: Getty Images.

IAM is a powerful enterprise platform

In 2024, global consulting network Deloitte conducted a study that found businesses waste over 55 billion hours each year due to inefficient agreement management processes, resulting in $2 trillion in lost economic value. IAM was built to solve that very problem.

One of IAM's most powerful resources is called Navigator, a digital repository where businesses have already collectively stored millions of agreements. It uses AI to extract important information from every document and then makes that discoverable via a search function, so employees no longer have to spend hours digging through contracts manually. It also uses AI to track expiration dates, so management can stop auto-renewals for contracts they no longer need, or get ahead of sales agreements that are about to lapse.

Then there is AI-Assisted Review, which uses an organization's preset standards to autonomously identify risks and opportunities in every agreement. Docusign says one of its customers, Crete United, used this tool to reduce contract negotiation times by 80% and improve deal execution speed by 90%.

As of April 30, the end of Docusign's fiscal 2027 first quarter, IAM accounted for just 12.6% of the company's total annual recurring revenue (ARR). That was up from 10.8% in the fourth quarter of fiscal 2026, just three months earlier, but it's clear there's still a long runway for growth.

Steady growth on the top and bottom lines

Docusign generated $830.2 million in revenue during the fiscal 2027 first quarter, which topped management's forecast range of $822 million to $826 million. That was a modest growth rate of 9%, so the company certainly isn't shooting the lights out right now -- especially compared to five years ago, when quarterly sales growth was regularly above 40%.

However, management is sacrificing some top-line growth to focus more on profitability so it can build a more sustainable business for the long term. Total operating expenses were flat during the first quarter, with a small reduction in marketing spending, typically a growth-oriented cost.

As a result, Docusign managed to generate a profit based on generally accepted accounting principles (GAAP) of $78.2 million for the period, which was a year-over-year increase of 8%. After excluding one-off and noncash expenses like stock-based compensation, the company delivered a much bigger adjusted (non-GAAP) profit of $214.9 million.

Docusign could give up some of its profits by investing more heavily in areas like research and development (R&D) and marketing, which would likely lead to faster revenue growth. This is a useful lever that management could pull in the future.

Docusign stock is attractively valued right now

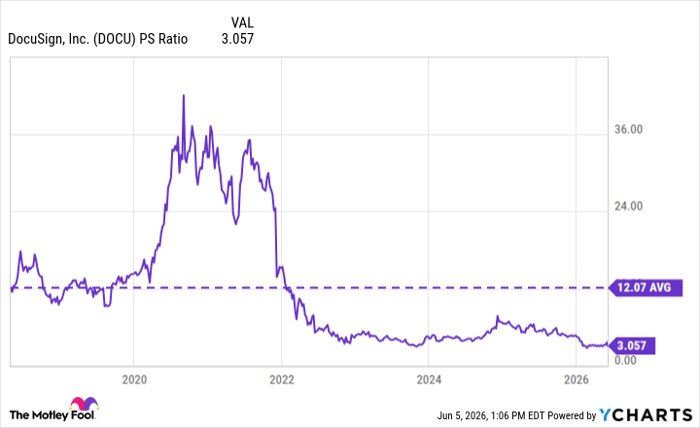

Docusign is currently trading at a price-to-sales (P/S) ratio of 3.1, which is a steep discount to its long-term average of 12.1 dating back to its IPO. The stock looks quite attractive from that perspective.

DOCU PS Ratio data by YCharts.

Based on trailing-12-month GAAP earnings of $1.57 per share, Docusign's price-to-earnings (P/E) ratio is 30.9. That's a discount to the Nasdaq-100 index, which is trading at a P/E of 35.2, so Docusign is slightly cheaper than the broader technology market right now.

Therefore, as IAM becomes a larger part of the company's revenue, I think Docusign's current stock price offers investors an attractive long-term entry point.

Should you buy stock in Docusign right now?

Before you buy stock in Docusign, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Docusign wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $443,191!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,258,838!*

Now, it’s worth noting Stock Advisor’s total average return is 941% — a market-crushing outperformance compared to 206% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 8, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Docusign. The Motley Fool has a disclosure policy.

Recommended Articles