My Top 4 Stocks That Benefit Most from the $725 Billion AI Infrastructure Supercycle

Key Points

Chip stocks such as Nvidia, Broadcom, and AMD have shown that their revenue and earnings are growing at incredible rates due to the huge amount of money being spent on AI data centers.

TSMC is the go-to foundry partner for chip designers capitalizing on the AI boom, making it a no-brainer buy right now.

- 10 stocks we like better than Nvidia ›

The artificial intelligence (AI) infrastructure boom isn't slowing down, as major hyperscalers, governments, and AI companies continue to invest hundreds of billions of dollars to set up more AI data centers.

As reported by the Financial Times, the top four hyperscalers in the U.S. -- Google, Microsoft, Meta Platforms, and Amazon are going to spend $725 billion on capex this year, a 77% increase from last year's levels. The overall spending, however, could be much higher, as AI companies, neocloud infrastructure providers, and governments are also spending huge sums on the AI infrastructure build-out.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

It is easy to see why companies continue to invest aggressively in AI data centers. The demand for AI computing capacity exceeds supply, and these hyperscalers need to satisfy more than $2 trillion in contractual backlogs based on their remaining performance obligations (RPO). Though there are several AI stocks you can buy to benefit from this $725 billion opportunity, we are going to take a closer look at four names that are well-positioned to make the most of the booming AI infrastructure supercycle.

Image source: Getty Images.

These chip stocks will be definitive winners of the AI infrastructure boom

A nice chunk of the massive AI infrastructure spending this year will be allocated to semiconductors. Gartner estimates that non-memory semiconductors, such as graphics cards and custom AI processors, will generate a whopping $687 billion in revenue this year.

Nvidia (NASDAQ: NVDA) should be one of the first semiconductor stocks you should consider buying to capitalize on the massive AI infrastructure investments. That's because the company continues to crush the competition in AI chips, as evident from its latest quarterly results. Nvidia's fiscal 2027 Q1 revenue (for the three months ended April 26) increased by 85% year over year to a record $81.6 billion.

The company is anticipating $91 billion in revenue for the current quarter, which points toward stronger growth of 95% year over year. This acceleration in Nvidia's growth can be attributed to the company's strong $1 trillion sales forecast for its Blackwell and Vera Rubin graphics cards in 2026 and 2027. Additionally, the company has unlocked a new growth opportunity by deciding to offer its server processors as a stand-alone product.

Nvidia sees a $200 billion revenue opportunity in the server processor market, which has been untapped by the company so far. Importantly, the company anticipates $20 billion in server CPU sales this year, complementing the healthy growth that it is going to witness in the data center GPU market.

On the other hand, Advanced Micro Devices (NASDAQ: AMD) is also making solid progress in the AI chip space. Though its growth isn't as impressive as Nvidia's, the company's diversified presence in server processors, graphics cards, and edge devices, such as computers, positions it well to capitalize on AI chip growth across multiple applications.

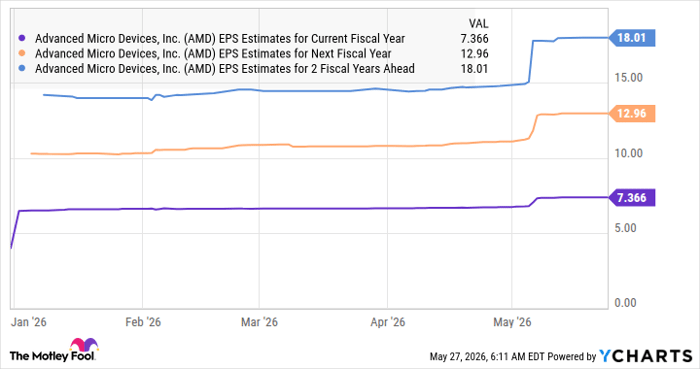

AMD has sizable contracts to deploy AI chips for companies such as OpenAI and Meta Platforms. These contracts are set to kick off this year, which explains why AMD anticipates 46% year-over-year revenue growth in the current quarter, up from the 38% increase it saw in Q1. Analysts are anticipating a solid year-over-year increase of 76% in AMD's earnings this year to $7.37 per share, followed by notable jumps in 2027 and 2028.

Data by YCharts

If the company can indeed achieve $18.01 in earnings per share in 2028 and trades at 43 times earnings at that time (in line with the Nasdaq Composite index's average earnings multiple), its stock price could reach $774 within the next three years. That's a potential upside of 53%, giving investors a solid reason to buy it right away.

Broadcom (NASDAQ: AVGO) is another top name in the AI chip industry that's witnessing strong demand for its custom processors. Hyperscalers have been developing in-house data center processors, known as application-specific integrated circuits (ASICs), to run AI workloads cost-effectively in data centers.

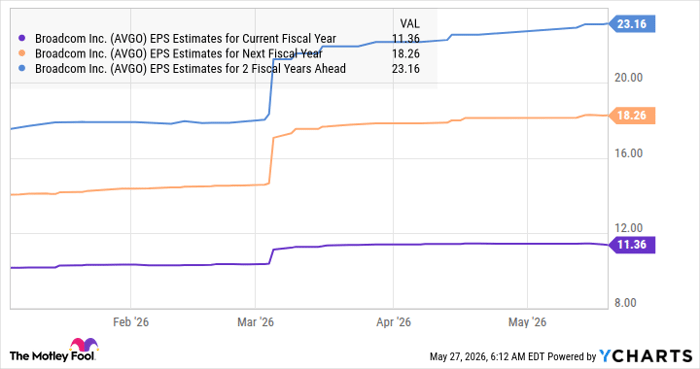

Counterpoint Research estimates that shipments of ASICs for AI servers could triple by 2027, compared with 2024 levels. The firm expects Broadcom to remain the top custom AI processor company next year with an estimated 60% market share. Not surprisingly, Broadcom expects its AI chip revenue to soar to more than $100 billion in 2027. That's going to be a massive improvement compared to the $20 billion AI revenue Broadcom reported last year.

This big surge is going to fuel remarkable growth in Broadcom's bottom line, with analysts expecting its earnings to double in just two years.

Data by YCharts

This terrific earnings growth potential suggests Broadcom stock could surge impressively if it trades in line with the Nasdaq Composite.

This company plays an indispensable role in AI infrastructure

All three chip designers discussed above rely on the same foundry for manufacturing their chips -- Taiwan Semiconductor Manufacturing (NYSE: TSM). TSMC, therefore, is the bigger pick-and-shovel AI infrastructure play, as strong demand for various types of AI chips will ensure healthy long-term growth for the foundry giant.

Moreover, TSMC is the world's largest foundry with a market share of 72%, according to Counterpoint Research. This makes TSMC a safe bet on the secular growth of the AI infrastructure market. In fact, the company sees its revenue from sales of AI accelerators increasing in the mid-to-high 50% range through 2029.

With TSMC stock trading at just 26 times forward earnings, it makes sense to buy this AI kingpin considering that its earnings are expected to jump to $24.95 per share in 2028, an increase of almost 2.5x compared to its earnings in 2025. Importantly, TSMC can sustain its solid earnings growth for a longer period, which means it has the potential to make investors significantly richer.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $471,072!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,303,352!*

Now, it’s worth noting Stock Advisor’s total average return is 983% — a market-crushing outperformance compared to 210% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 28, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Amazon, Broadcom, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Gartner. The Motley Fool has a disclosure policy.

Recommended Articles