New Fed Chair Kevin Warsh Thinks the Agency Made the Largest Policy Error in 50 Years During the COVID-19 Pandemic. Fixing It May Not Be So Fun for Wall Street.

Key Points

New Federal Reserve Chair Kevin Warsh has never been a fan of quantitative easing.

Naturally, he's been very critical of how the Fed's balance sheet ballooned to close to $9 trillion following the pandemic.

However, unwinding the Fed's balance sheet may not be so favorable for the stock market.

- These 10 stocks could mint the next wave of millionaires ›

Kevin Warsh has officially been sworn in as the new chair of the Federal Reserve's Board of Governors. If his past comments are to be believed, big changes could be coming to the Fed regarding how it thinks about inflation, the size of its balance sheet, and even how it communicates with the public.

Warsh has been critical of the Fed and thinks that, under Jerome Powell's leadership, the agency made one of its largest policy errors in 50 years. But reversing this move won't happen overnight -- and may not be so fun for Wall Street.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

What the Fed did

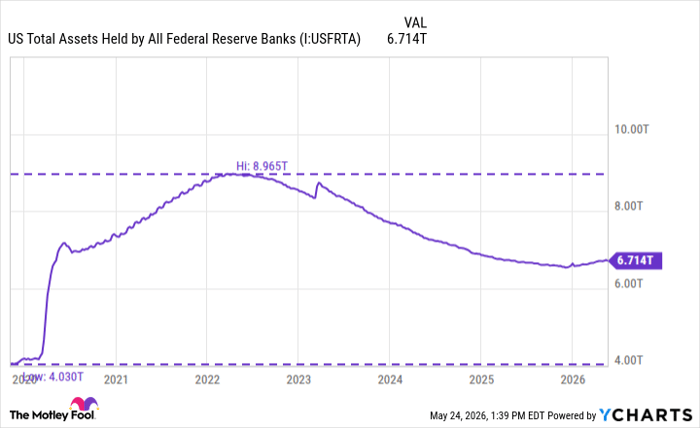

At the beginning of the COVID-19 pandemic in 2020, the Federal Reserve cut interest rates to zero and restarted quantitative easing (QE), the process of purchasing U.S. Treasury bonds and mortgage-backed securities (MBS) to flood the economy with liquidity. This swelled the Fed's balance sheet over the next few years to nearly $9 trillion in assets. At the same time, the federal government was also implementing significant stimulus measures.

US Total Assets Held by All Federal Reserve Banks data by YCharts

Now, officials were responding to a particularly scary time for the world and the economy, so there are still varying opinions on whether the Fed and the government acted correctly. However, during congressional testimony in April, Warsh referred to the COVID-era moves as "the biggest economic policy error in 40 or 50 years."

Many blame QE, the Fed's large balance sheet, and government stimulus for some of the highest inflation in 40 years, which peaked at over 9% in the summer of 2022. While inflation has slowed significantly, prices are still rising, and affordability has become one of the largest problems in the U.S. today.

Warsh believes that using the Fed's balance sheet as a monetary tool disproportionately benefits people who own assets, such as homes or stocks, which have performed extremely well since the Great Recession.

The fix is easier said than done

Fixing the Fed's large balance sheet is fairly simple on the surface: If the balance sheet is too big, the Fed simply needs to shrink it. However, doing so without disrupting financial markets is easier said than done.

The Fed shrinks its balance sheet using quantitative tightening (QT): Instead of buying bonds and mortgage-backed securities, the Fed either sells them or lets the bonds mature without reinvesting the proceeds. This effectively pulls money out of the economy and could, in theory, put downward pressure on assets such as equities and home values.

Conducting QT requires a delicate touch and can turn nasty if the Fed isn't careful.

For instance, under former chair Jerome Powell, the Fed began conducting QT in 2018, which extended into 2019. But QT had unintended consequences, as it reduced cash circulating in the market, forcing various market participants to seek short-term financing in the reverse repo market. The excess demand led yields in the reverse repo market to soar, forcing the Fed to abruptly end QT and actually begin injecting liquidity into the market again.

To Powell's credit, the Fed has reduced its balance sheet to about $6.7 trillion since it peaked in 2022. But it had to halt QT once again toward the end of last year due to declining bank reserves, which the Fed described as at "ample levels."

Since December, the Federal Open Market Committee (FOMC), which sets monetary policy, has been conducting reserve management purchases totaling $40 billion in U.S. Treasury bills each month.

Ultimately, getting the balance sheet down will take some finessing, as Warsh acknowledged in his April testimony, saying, "Slowly and deliberatively, I believe we need a smaller central bank balance sheet. As I mentioned, it took 18 years to create this balance sheet problem, and we won't be able to fix it in 18 minutes."

Why it may not be so fun for Wall Street

Experts believe QE led to inflated asset prices, so QT could deflate them. If there's less money circulating through the economy, in theory, that's less money to drive home demand, less for private markets like private equity and venture capital, and less for newer alternative assets like cryptocurrencies.

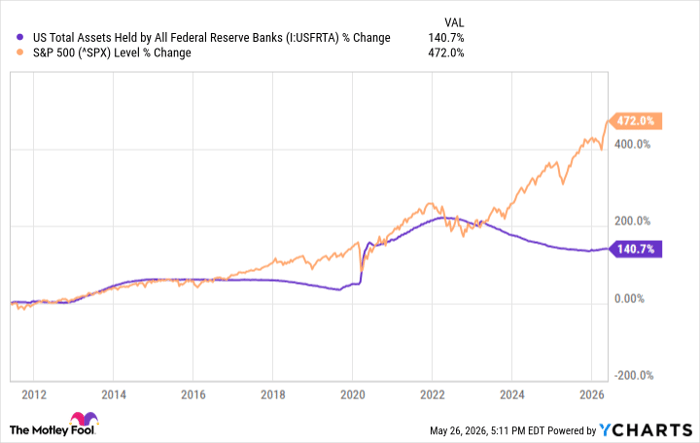

I wouldn't necessarily call it a trend, but in the past, one could argue there was some correlation between QE/QT and the broader stock market; more recently, though, the two certainly haven't been correlated.

US Total Assets Held by All Federal Reserve Banks data by YCharts

Now, investors should understand that QE and QT are relatively new concepts. The Fed had never used its balance sheet as a monetary tool like this until the Great Recession in 2008.

So it's still going to be hard to predict exactly how QT will impact financial markets, and other factors could affect markets as well. Warsh also said that if the Fed's balance sheet is reduced, interest rates could likely be lower, inflation could be in a better position, and the economy could be stronger.

So, while the market may be able to push through the Fed's balance sheet shrinkage, the policy is still typically viewed as a headwind for stocks and may not be so fun for investors when everything is said and done.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, Stock Advisor’s total average return is 986%* — a market-crushing outperformance compared to 208% for the S&P 500.

They just revealed what they believe are the 10 best stocks for investors to buy right now, available when you join Stock Advisor.

See the stocks »

*Stock Advisor returns as of May 26, 2026.

The Motley Fool has a disclosure policy.

Recommended Articles