Super Micro Computer's Sales More Than Doubled Last Quarter. Here's Why I'd Still Stay Far Away From the Stock

Key Points

Super Micro Computer's sales looked strong in Q3, rising by 123%.

Low margins, however, continue to be a problem for the company.

The stock is cheap, but investors may have lost trust in it due to previous reporting issues.

- 10 stocks we like better than Super Micro Computer ›

Super Micro Computer (NASDAQ: SMCI) recently posted some incredibly strong sales numbers, with its top line more than doubling. Net sales of $10.2 billion for the third quarter of Fiscal 2026, which ended on March 31, were up an impressive 123% year over year. The company, which is involved in the sale of key technology infrastructure for businesses, including servers for artificial intelligence (AI), has experienced tremendous growth in recent years.

But while its sales have been impressive, that may not be enough of a reason to invest in the tech stock. Here's why, despite its strong top-line numbers, I'd stay far away from it.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

The company's razor-thin margins are a huge concern

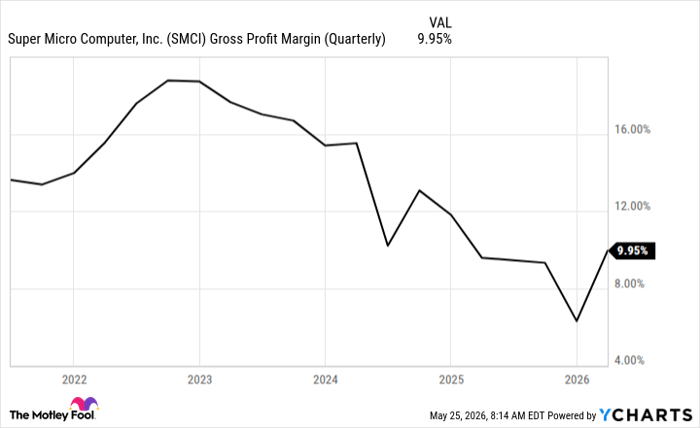

A big problem that continues to plague Super Micro Computer is that its margins are extremely low. This means that its cost of revenue is high, and thus, a small portion of its revenue is left over to cover operating expenses and flow through to the bottom line. In its most recent quarter, which ended on March 31, Super Micro's gross margin was just under 10%.

SMCI Gross Profit Margin (Quarterly) data by YCharts

While margins have improved modestly for Super Micro, they remain incredibly low. And over the past nine months, while revenue has risen by 72% to $27.9 billion, its gross profit has risen by just 21% to $2.3 billion. The company has been doing well due to strong demand as a result of AI, but if that slows down, then that would only make things worse; C3.ai's incredibly strong revenue growth is making up for its low margins, enabling it to generate solid gains on the bottom line. But if things change, that may quickly no longer be the case.

Super Micro stock may look cheap, but it's not worth the risk

In the past 12 months, shares of C3.ai have declined by 14%. Today, the stock trades at a relatively low 19 times its trailing earnings, which may seem like a bargain given that the average stock on the S&P 500 trades at 26 times its earnings.

Super Micro, however, has had accounting issues in the past, with its auditors previously resigning, calling into question the company's controls and processes. While there haven't been any big concerns that have popped up since then, it's still an issue that may continue to weigh on the stock and give investors reason to question the strength of its numbers. And when you add in its low margins and dependence on AI-fueled growth, it leaves you with a stock that contains a bit more risk than it's worth.

Should you buy stock in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $477,813!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,320,088!*

Now, it’s worth noting Stock Advisor’s total average return is 986% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 25, 2026.

David Jagielski, CPA has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Recommended Articles