Lam Research Corp Stock (LRCX) Moved Up by 6.62% on Jun 29: Drivers Behind the Movement

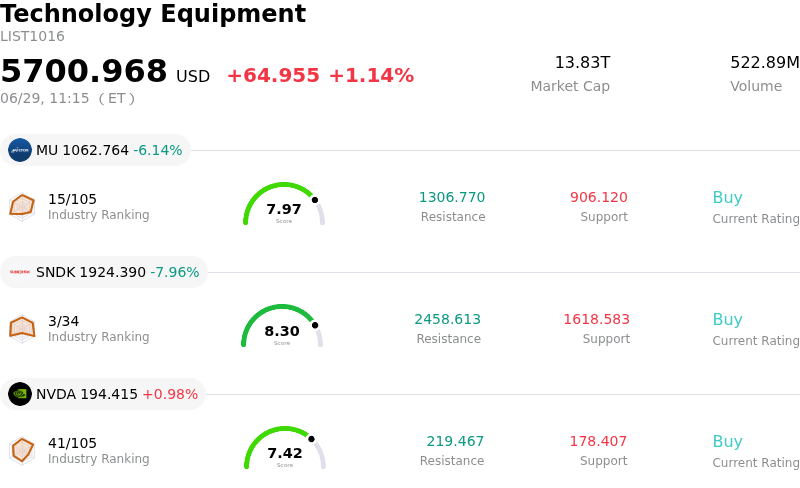

Lam Research Corp (LRCX) moved up by 6.62%. The Technology Equipment sector is up by 1.14%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 6.54%; SanDisk Corporation (SNDK) down 7.96%; NVIDIA Corp (NVDA) up 0.98%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research experienced a robust upward movement today, fueled by a high-profile analyst upgrade and renewed investor confidence in the semiconductor capital equipment sector. This sharp recovery comes directly after a period of sector-wide consolidation and profit-taking in the AI hardware space. The primary driver for today's bullish momentum was Cantor Fitzgerald raising its price target on the company to $500 from $425, while maintaining an Overweight rating. In its research note, the firm highlighted that Lam Research is capturing the most market share among its peers in the semiconductor capital equipment space.

Further driving the positive sentiment, analysts noted that institutional investors are increasingly pricing in expanding wafer fabrication equipment forecasts that stretch through 2030. This long-term growth outlook is heavily underpinned by the global transition toward artificial intelligence infrastructure. Lam Research serves as a critical supplier of the highly specialized etching and deposition equipment required to manufacture leading-edge chips, high-bandwidth memory, and advanced packaging configurations. As semiconductor architectures transition into more complex three-dimensional structures, the demand for Lam’s atomic-level precision tools scales exponentially.

The positive commentary from Cantor Fitzgerald is part of a broader wave of Wall Street upgrades and target price hikes over the past week. Major financial institutions, including Bank of America and Wells Fargo, have recently raised their price targets to $480 and $450 respectively, pointing to record-setting quarterly earnings and a raised industry wafer fabrication equipment outlook for 2026. This concerted bullishness has effectively countered recent market anxieties regarding geopolitical export regulations and short-term capacity adjustments from memory manufacturers.

Overall, the combination of dominant market share gains, long-term secular tailwinds in AI packaging, and aggressive price target revisions by leading sell-side analysts has reignited buying pressure. The strong upward move underscores Lam Research's indispensable position within the global semiconductor supply chain, solidifying its status as a core beneficiary of the ongoing AI infrastructure buildout.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 1.314, indicating a buy signal. The RSI at 57.869 suggests neutral condition and the Williams %R at 29.555 suggests buy condition. Please monitor closely.

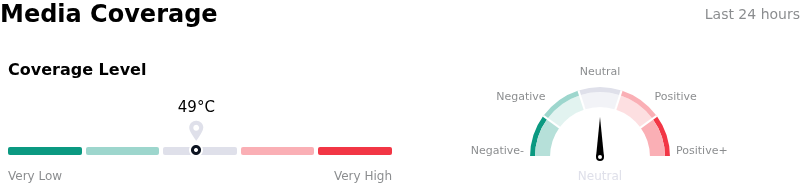

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $337.58, a high of $480.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- **Exposure to Customer Capacity Shifts**: SK Hynix's decision to shift manufacturing capacity away from advanced AI configurations (such as HBM and advanced NAND) toward commodity DRAM compresses the near-term order pipeline for Lam Research. Because commodity manufacturing requires significantly fewer deposition and etching process steps, this reallocation lowers the revenue-generation potential of Lam’s advanced toolsets.

- **Severe Deceleration in Shipment Growth**: Driven by expected cyclical cooling in both 3D NAND and mature-logic nodes, institutional analysts have highlighted a projected deceleration in Lam Research's system shipment growth down to just 3% in 2026 from 82% in 2025. This structural slowdown is compounded by falling customer down payments, signaling a near-term cooling of customer capital commitments.

- **Geopolitical and China Revenue Concentration Risks**: With China generating approximately 34% to 35% of total revenue, Lam Research remains highly vulnerable to expanding trade restrictions. This exposure has been exacerbated by the Department of Commerce's restrictions halting advanced tool shipments to Chinese fabrication facilities, including Hua Hong and Huali Microelectronics, which threatens regional market share and top-line stability.

- **Valuation Susceptibility and Insider Liquidations**: Trading at an elevated valuation with a trailing P/E ratio exceeding 69x, the stock faces high susceptibility to multiple compression during broader semiconductor sector pullbacks. This vulnerability is highlighted by recent Form 4 SEC filings disclosing significant insider stock liquidations, including a $19.1 million divestment by Director Eric Brandt and a position reduction by SVP Neil J. Fernandes.

Recommended Articles