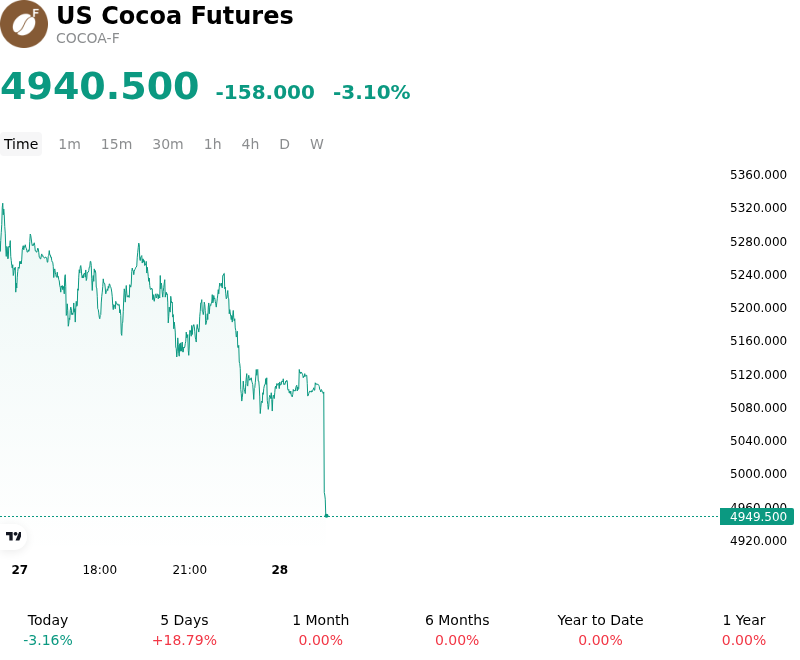

US Cocoa Futures (COCOA-F) Is down 3.10% on Jun 29: What Changed in Supply and Demand?

US Cocoa Futures (COCOA-F) is down 3.10% at Jun 29 04:55(ET), now at $4940.5, with a 7-day up of 10.14%.

What is driving US Cocoa Futures (COCOA-F)’s stock price down today?

The intraday decline in cocoa futures is primarily driven by emerging signs of expanding global supplies and rising exchange-certified inventories, which have prompted extensive long liquidation following a sharp rally to multi-month highs. Investors are increasingly focusing on improved physical availability in West Africa and structural demand destruction, which are collectively easing the supply-demand imbalance that previously drove prices upward.

A major catalyst for the downward pressure is the notable acceleration in exports and port arrivals from key West African producers. Export data from Nigeria, the world's fifth-largest producer, revealed that cocoa shipments in May surged by twenty-eight percent year-on-year. Furthermore, cumulative port arrivals in Ivory Coast, the global leader in cocoa production, have shown robust double-digit growth compared to the prior marketing season. These strong shipping volumes indicate that West African supply is recovering more rapidly than anticipated, helping to dissipate anxieties over long-term production deficits.

Compounding this supply recovery is the steady accumulation of physical stocks. ICE-certified cocoa inventories have recently climbed to a multi-year high, exceeding 2.9 million bags. This rebuild in exchange warehouse stocks signals that near-term physical tightness is dissipating, which diminishes the scarcity premium that has historically supported elevated futures contracts.

On the demand side, historically high retail prices continue to trigger severe demand destruction. Global processors have indicated highly subdued volume growth expectations as elevated input costs force chocolate manufacturers to reduce processing volumes or utilize alternative fats. This structural shift is supported by weak grind data, which showed significant year-on-year declines in first-quarter cocoa grindings across both Europe and North America. The combination of recovering West African supplies, growing exchange inventories, and stagnant global grind activity has forced institutional investors to reassess the commodity’s pricing trajectory, leading to profit-taking and the unwinding of speculative long positions.

More details about US Cocoa Futures (COCOA-F)

Recent Events and Risks:

- Surging West African Port Deliveries and Exports: Recent data indicates a significant easing of regional supply constraints, highlighted by a 28% year-on-year surge in Nigerian cocoa exports for May to 18,034 MT. Concurrently, cumulative port arrivals in the Ivory Coast reached 1.95 million metric tons, up 18.9% compared to the same period last season, prompting aggressive long liquidation in futures markets.

- Multi-Year Highs in Exchange-Certified Stocks: ICE-certified cocoa inventories climbed to a 1.75-year high of 2,948,286 bags in late June 2026. This persistent build in exchange warehouse stocks signals a major recovery in near-term physical availability, removing the immediate supply squeeze and capping upside price potential.

- Severe Processing Demand Destruction: Sustained high commodity prices have led to structural demand destruction, as evidenced by weak global processing data. First-quarter cocoa grindings dropped 3.8% year-on-year in North America and plunged 7.8% in Europe to a 17-year Q1 low, indicating that chocolate manufacturers are cutting back production and struggling with weak consumer volume growth.

- Unwinding of Geopolitical and Logistical Risk Premiums: The normalization of shipping corridors and the easing of geopolitical tensions, particularly regarding shipping lanes, have reduced freight rates and insurance surcharges. The removal of this built-in logistical risk premium has prompted speculative funds to close out long positions, adding technical downward pressure on NY and London futures contracts.

Recommended Articles