The Best 3 Consumer Staples Stocks to Buy and Hold for Decades

Key Points

While growth stocks have soared higher over the last year, many consumer staples stocks have dipped.

The three consumer staples stocks below have dropped between 48% and 56% from their 52-week highs.

Though they may be more volatile, these three offer market-beating potential following their declines.

- 10 stocks we like better than Chewy ›

While I may be taking a few liberties in calling the three stocks in this article consumer "staples" companies, I think each business offers a lot of the defensive traits that make the sector intriguing to investors. Not only do these businesses offer products I'd consider staples in their respective niches, but each stock also offers promising outperformance potential at a reasonable valuation.

Although these may not be your grandparents' consumer staples -- and may display more volatility than Colgate-Palmolive, for example -- I think each of these stocks could turn into "steady-Eddie" types of stocks over time and are worth buying and holding for decades.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: The Motley Fool.

1. Chewy: 56% below 52-week high

I would argue that the leading pet goods e-commerce company, Chewy (NYSE: CHWY), has become a "new age" consumer staples stock, as the humanization of pets megatrend has made spending on our furry friends incredibly resilient, regardless of the economy.

This notion is especially true for Chewy, which generates 84% of its revenue from its booming Autoship sales. Autoship lets Chewy customers schedule and automate the ordering and delivery of repeat items, such as pet food, treats, or healthcare products. This Autoship revenue is incredibly resilient, giving Chewy a large, recurring sales base it can plan its operations around month to month.

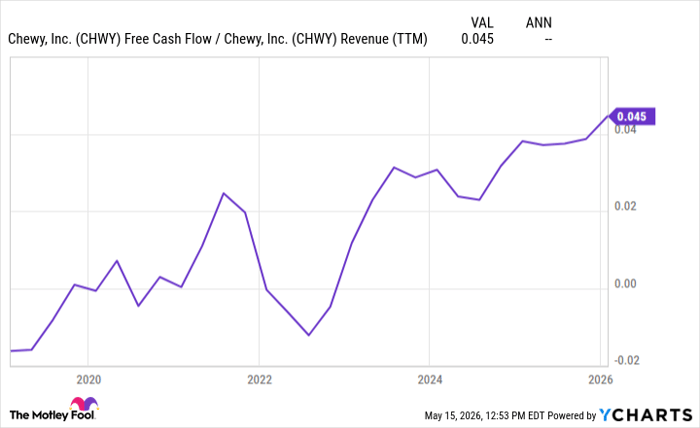

Said another way, 84% of Chewy's revenue is automated, without customers needing to place an order (outside of the original Autoship setup). To me, that's as consumer "staple-y" as it gets. Best yet for investors, the company's operations have continued to streamline beautifully, as evidenced by its free-cash-flow (FCF) ratio.

Fundamental Chart data by YCharts.

Expanding into higher-margin areas such as Chewy Vet Care (CVC) clinics, private-label goods, advertising, veterinary software, pet insurance, and pharmacy products, the company could see its margins continue to rise.

However, despite growing revenue and free cash flow by 8% and 24%, respectively, in 2025 -- with Autoship sales rising 14% -- Chewy saw its stock drop 56% from its 52-week high. Now trading at just 13 times forward earnings, Chewy's reasonable valuation is more than supported by its steady sales growth, improving margins, and expansion in the veterinary industry.

2. Stride: 48% below 52-week high

Getting a good K-12 (or even adult) education is one of the most important factors influencing our lives. For that reason, I think Stride (NYSE: LRN) and its technology-based online education system are quickly becoming a staple for many parents (and lifelong learners) seeking an education outside traditional school options. Whether it's a public school looking to provide a virtual school for home-schooled students or a local school district picking a class from Stride's curriculum that it can't effectively cover with its own staff, the company helps bring the educational system into the digital era.

Over the years, Stride was a pretty steady stock that held a leadership position in its niche. However, it lost some of its "consumer staples" feel in 2025 when the company experienced major issues implementing a platform upgrade. This disruption caused Stride to miss out on 10,000 to 15,000 enrollments -- a sizable figure compared to its total enrollment base of 244,500 today. Following this news, the stock tanked and is just now starting to regain its footing.

However, despite this self-inflicted error, Stride has largely recovered, with enrollments rising 2% in its last quarter and with operating income back to normal levels. Management stated that Stride is still on track to grow revenue by 10% annually through 2028 and reach over $8 in earnings per share that year. While artificial intelligence (AI) will be a persistent threat to any education company, Stride is well protected by educational regulations and the need for its teachers to solve human-to-human problems (even over laptops), making it less susceptible to disruption.

Trading at 11 times forward earnings following last year's shellacking, Stride is a consumer staples stock with significant long-term potential.

Image source: The Motley Fool.

3. Sprouts Farmers Market: 52% below 52-week high

From 2023 to 2025, better-for-you and attributed-focused grocer Sprouts Farmers Market (NASDAQ: SFM) saw its stock skyrocket from $30 to over $170 as the market decided its growth story was underappreciated. However, as much as I like Sprouts Farmers Market's stock, its valuation probably got quite a bit ahead of itself, which helped cause the subsequent drop back to around $90 today.

Despite this incredible volatility in its share price, Sprouts' actual operations have been rather steady -- almost staples-like, I'd dare say. While grocers certainly fit the consumer staples billing, Sprouts is unique thanks to its focus on attribute-based products, such as vegan, gluten-free, non-GMO, organic, responsibly sourced, and more. This differentiation stands out, particularly in a time when consumers are actively seeking healthier food options, and millions use GLP-1 medicines.

Best yet for investors, Sprouts delivers these unique products at a reasonable price as it tests thousands of new product ideas annually and often goes on to create private-label versions of its most popular creations. Despite macroeconomic headwinds that have hindered the company's operations over the last year, Sprouts inched its sales 4% higher in the latest quarter and continued its steady expansion beyond California, Texas, and Florida, which account for more than half its stores.

If Sprouts is even remotely successful at expanding from its current store count of 483 to its long-term goal of 1,400, the company could be a steal at just 15 times forward earnings today.

Should you buy stock in Chewy right now?

Before you buy stock in Chewy, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Chewy wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $469,293!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,381,332!*

Now, it’s worth noting Stock Advisor’s total average return is 993% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 18, 2026.

Josh Kohn-Lindquist has positions in Chewy, Sprouts Farmers Market, and Stride. The Motley Fool has positions in and recommends Chewy, Sprouts Farmers Market, and Stride. The Motley Fool recommends the following options: long January 2028 $75 calls on Sprouts Farmers Market and short January 2028 $85 calls on Sprouts Farmers Market. The Motley Fool has a disclosure policy.

Recommended Articles