Tech Sell-Off: 2 "Magnificent Seven" Stocks to Buy With $500 and Hold Forever

Key Points

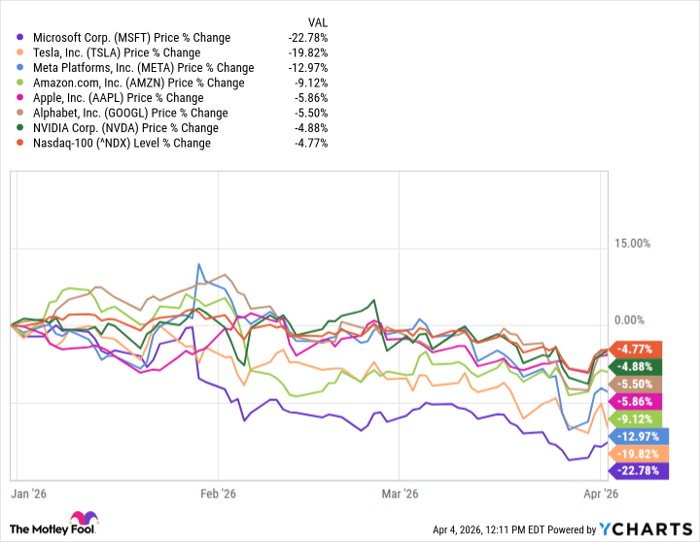

The high-growth "Magnificent Seven" stocks have suffered an average decline of 11.5% in 2026 so far, while the Nasdaq-100 index is down just 4.8%.

These stocks rarely underperform the rest of the market, so this weak period might be a fantastic long-term buying opportunity.

Amazon and Alphabet are two Magnificent Seven stocks that look particularly attractive right now.

- These 10 stocks could mint the next wave of millionaires ›

In 2023, Wall Street analyst Michael Hartnett nicknamed a group of America's largest companies the "Magnificent Seven" because of their dominance in various areas of the technology industry and their tendency to generate faster revenue and earnings growth than the rest of the market. The companies (in no particular order) are:

- Nvidia

- Apple

- Alphabet (NASDAQ: GOOGL)(NASDAQ: GOOG)

- Microsoft

- Amazon (NASDAQ: AMZN)

- Meta Platforms

- Tesla

The Magnificent Seven consistently deliver higher returns than the rest of the stock market, but they are suffering a rare period of underperformance right now. The Nasdaq-100 index is down 4.8% in 2026 so far because of the ongoing geopolitical tensions in the Middle East, whereas the average Magnificent Seven stock has suffered a much sharper year-to-date decline of 11.5%.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Data by YCharts.

High-growth stocks tend to experience more volatility during times of uncertainty, but this also creates buying opportunities. There is a legitimate case for owning each of the Magnificent Seven stocks, but I want to highlight Amazon and Alphabet, which look particularly attractive right now. Investors with $500 available to invest can pick up a single share in each company; here's why it might be a smart move.

Image source: Getty Images.

The case for Amazon

Amazon was a pioneer of the e-commerce industry in the late 1990s, and the Amazon.com retail platform is still its single largest source of revenue. However, the company has leveraged its success to enter other markets, like streaming, digital advertising, and cloud computing, over the last 20 years. The expansion is paying off, particularly in the cloud industry, where Amazon Web Services (AWS) is now the undisputed leader.

AWS offers hundreds of solutions to help businesses thrive in the digital age, from simple data storage to complex software development tools, but the platform has also become the center of Amazon's artificial intelligence (AI) strategy. AWS now operates hundreds of specialized data centers all over the world, and it rents the computing capacity to businesses so they can develop and deploy AI software.

These data centers are fitted with specialized AI chips from suppliers like Nvidia, but Amazon also designed its own. Its latest Trainium2 chip delivers 40% better price performance than competing hardware, and Trainium3, which launched recently, offers a further improvement of 40%. Amazon ended 2025 with a $244 billion order backlog for computing capacity from its cloud customers, and designing its own chips in-house will help the company bring data centers online much faster than relying on third-party suppliers.

AWS generated $128.7 billion in total revenue in 2025, and its fourth-quarter growth rate of 24% was the fastest since the third quarter of 2022, which highlights the platform's incredible AI-driven momentum. AWS is also Amazon's most profitable business unit, accounting for more than half of the company's operating income in 2025.

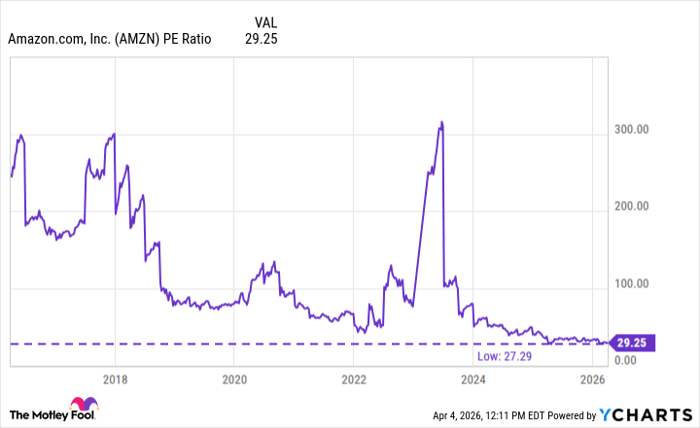

While Amazon stock is down 9% in 2026, it's also down 17% from last year's record high. It now trades at a price-to-earnings (P/E) ratio of just 29.2, which is close to the cheapest level since it went public almost 30 years ago. In my opinion, this presents long-term investors with a very attractive entry point.

Data by YCharts.

The case for Alphabet

Alphabet is the parent company of Google, YouTube, Waymo, DeepMind, and more. It's one of Amazon's biggest competitors in the cloud space through its Google Cloud platform, which offers many of the same services as AWS.

Google Cloud is one of Nvidia's biggest data center customers, but Alphabet also designed its own chips, called Tensor Processing Units (TPUs), which are even more specialized for AI workloads than traditional graphics processing units (GPUs). In fact, Alphabet used its latest Ironwood TPUs to train its Gemini 3 family of large language models (LLMs), which are among the most powerful in the AI industry.

More than 120,000 enterprises around the world tap into the Gemini models through Google Cloud, which they use as a foundation for their own custom AI software. This is important because the more AI applications companies build on Gemini, the more tokens they consume, and the more money Google Cloud makes.

The cloud platform generated a record $58.8 billion in revenue during 2025. Its revenue growth accelerated in each of the last three quarters, and came in at a whopping 48% in the final quarter of the year.

But Google Search, which remains Alphabet's largest source of revenue, also ended 2025 with accelerating growth. New features like AI Overviews and AI Mode have blended the traditional internet search experience with the convenience of AI, giving users much faster access to information. As a result, Alphabet says Google Search is experiencing higher usage than ever before, which is attracting more advertisers.

Alphabet stock is trading at a P/E ratio of 27.2 as I write this, so not only is it even cheaper than Amazon, but it's also cheaper than the Nasdaq-100 technology index, which has a P/E of 29.3. The recent stock market sell-off might be giving long-term investors a great entry point.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $472,291!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $49,299!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $536,003!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

See the 3 stocks »

*Stock Advisor returns as of April 9, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla and is short shares of Apple. The Motley Fool has a disclosure policy.

Recommended Articles